Some of us may have been aware of the big fuss that started a few weeks ago in the “repo market” and that required the intervention of the Federal Reserve through the injection of money. But how many understand what is traded in this market and why is it important for the US economy?

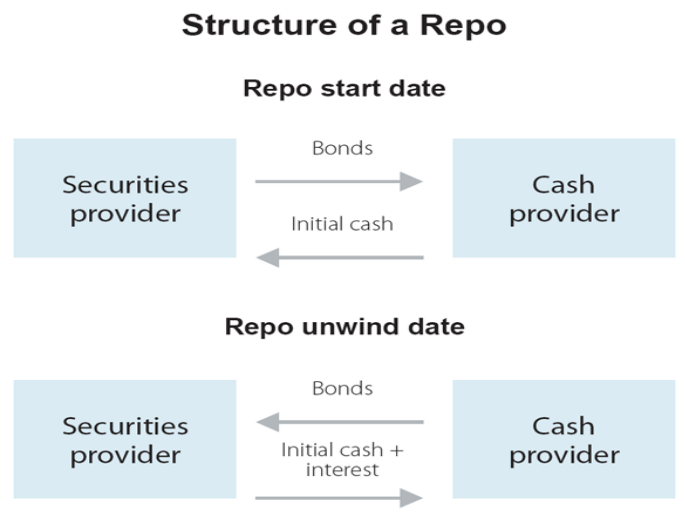

What is a repo?

First, we must grasp this concept of Repurchase Agreements. A repo operation occurs when one party lends money to another using US Treasury notes (or other types of securities, although less usual) as collateral. The party that exchanges the securities for cash agrees to buy them back for a higher price at a later date, usually the following day. The difference between these prices is the repo rate

Repurchase agreements allow lenders to earn a low but secure return while holding safe securities as collateral and borrowers without liquid assets to meet their short-term obligations. Borrowers regularly consist of Wall Street brokers or hedge funds that must manage large portfolios through day operations. Lenders can be anyone with a money-market savings account looking for a short-term risk-free investment.

Federal Funds Market

Besides covering short-term needs in terms of liquidity and providing a safe investment for the agents previously mentioned, repurchase agreements are also an important money-market tool in the federal funds market. As we are aware, banks work with financial assets, loans and deposits but they require cash to manage their day-to-day operations and short-term obligations (mostly payments and other transactions). Therefore, banks (and some other parties) trade their reserves at the Federal Reserve with one another overnight through repurchase agreements. The banks with excess reserves lend them to less liquid banks in exchange for US Treasury notes that will be returned next morning for a higher price. The repo rate in this market has the name federal funds rate and is the Fed’s goal to keep it between defined lower and upper bounds.

The importance of repurchase agreements

The repo market is a vital cog in the US economy by accomplishing different functions:

-

Arrange efficient short-term funding: by offering short-term deposits supported by safe securities and enabling lenders other than commercial banks, it makes funding easier, cheaper and more efficient;

-

Allow the management of day-to-day operations of low-cash portfolios: investors and especially large funds don’t keep many cash assets since they are considered unproductive, so repos allow for short-term payments without the sale of long-term positions;

-

Provide an accessible risk-free short-term investment: the fact that repos are collateralized by US Treasury notes makes them the perfect short-term choice for riskaverse investors such as money market funds or non-financial corporations; repos are also more available than other short-term options such as risk-free deposits at the Central Bank (only available to institutional agents) or Treasury bills (crowded primary market and tight secondary market);

-

Facilitate Fed operations: due to their low-risk, collateralized nature, and efficiency repurchase agreements are a widely used instrument by open market operations to increase or decrease money supply;

-

Foster price discovery: repos ease the primary market and most importantly inject liquidity in the secondary market, therefore fostering trade and arbitrage and aiding in discovering the relative prices of the securities used as collateral.

What is happening in the repo market?

Middle of September, interest rates on the obscure part of U.S lending spiked, prompting fears on broader problems. A few weeks ago, there was a big cash shortage where banks and hedge funds excessively demanded more funding that the market couldn’t supply. Monday 16th was a tax payment deadline for big companies and a holiday in Japan – which meant a large portion of funds’ sources were shut off – and after a recent Treasury auction for government bonds, there was a liquidity crunch.

These series of events shot interest rates up to 10 percent on overnight lending, more than four times the Fed’s target rate, as commercial banks saw their reserves shrinking unexpectedly. The federal funds rate hit 2.3 percent a day after, which is above the central’s bank target. This reflected in unexpected strains. (image 2.)

These increases in the interest rates of repurchase agreements were also influenced by the fact that there is less cash in the system compared to previous periods. Over the past years, the excess reserves have been declining since the Federal Reserve started shrinking its balance sheet, limiting the amount of money available in the markets. Since 2017, the Fed has been shortening their treasury and mortgage-backed securities (MBS) portfolio, now being at $3.9 trillion of assets, a significant reduction when compared to the $4.25 trillion worth of securities back in the period of 2008-2014 when there was a quantitative easing programme.

The Federal Reserve had to immediately intervene with a temporary injection of $75billion, open market operations to prevent borrowing costs from spiralling even higher. By fuelling the money market, the Fed was able to stabilize interest rates and slowly bring them to a suitable window within their parameters. It also announced the lowering of interest rates by a quarter percentage points as part of its effort to encourage economic growth, leaving interest rates between 1.75% and 2%.

The Fed chairman Jerome Powell said they had been expecting an extra demand because of Treasury settlements and the need for cash by tax-paying corporations. However, they were not expecting this amount of volatility in the market.

“The effective federal funds rate is the interest rate banks charge each other for overnight loans to meet their reserve requirements. Also known as the federal funds rate, the effective federal funds rate is set by the Federal Open Market Committee, or FOMC. The effective federal funds rate is the most influential interest rate in the nation’s economy. It affects employment, growth and inflation.”

— Bankrate Sourced

Why is or should Wall Street be concerned?

Well, any unwanted and unexpected volatility in the financial market tends to distress investors, especially in what some people think is a pre-recession phase of the US economy. However, the Fed came out to say that as they were shortening their balance sheet and reducing the excess reserves in the system it was inevitable for a moment like this to happen. This could have been seen by investors as a distraction by the Central Bank or as foreseen and expected event. Unfortunately, as in the 2008 recession, people are starting to feel like someone’s not telling them something, and adding this unanticipated rise of the overnight lending rates to the $17 trillion dollars’ worth of bonds with negative interest rates and to the inverted yield curve, they feel like something’s missing them. Maybe the real problem is not only on the shortage of reserve but on the essence of the transaction: the collateral

US Treasury bonds have been perceived for a long-time now, as risk-free securities, while still giving an average annual return of 2%. However, is it that unlikely that the US defaults on its debt obligations? If so, how can some financial institution let these considered risk-free bonds be a collateral in a repurchasing agreement that goes up to 10% in interest rates and how can the Fed lose such control over these interest rates? It may only be a normal Supply-Demand situation where lenders have that power to determine the interest rates due to the borrower’s despair, but questions about its intrinsic value are starting to appear raising concerns across the markets

As mentioned previously, the repo market, though rather unknown, played an important role in the crashing of the economy in 2008, where both the lenders and borrowers were destined to lose and lost money, since mortgages bonds were being used as collaterals with triple A ratings. When the economy suffered its great contraction and some big corporations and banks that made repos went bankrupt, the other parties were then trapped with securities that were in fact worthless. On the other side, some companies tried to save themselves in the short-term by making repurchasing agreements with the same collaterals that were now considered risky, even when lenders lost faith in these securities and withdrew their funding, leaving them with no chance of negotiating and trapped as well with them.

So, what if the US economy is heading in the same direction as a decade ago and no one is noticing it like they did then? Economists are still arguing, but still, the 16th September event may have been a sign of the times to come.

João Ribeiro

João Ribeiro  Martim Leong

Martim Leong  Francisco Nunes

Francisco Nunes

Thanks for one’s marvelous posting! I truly enjoyed reading it, you’re a great author.I will always bookmark your blog and will eventually come back from now on. I want to encourage you to ultimately continue your great job, have a nice evening!

LikeLike