The world is on red alert and has “Coronavirus” as its watchword. But what is exactly this virus that has caught everyone’s attention in the past weeks? This so-called coronavirus disease 2019 (COVID-19) is identified as a new type of coronavirus that belongs to a family of viruses that cause illness such as common cold, severe acute respiratory syndrome (SARS) and Middle East respiratory syndrome (MERS). Despite its scientific definition, not much is known about it yet. Nevertheless, its contagiousness is undeniable and, despite having started in China, according to the World Health Organization, “the number of infections outside China has outpaced those inside the country”, raising the world’s concern about the rise of a pandemic that has made, until now, 3555 victims. Yet, another question arises: is this mysterious virus only a well-being subject? As a matter of fact, this highly contagious virus is spreading beyond healthcare fields, shaking economies and tumbling global markets.

Hit-hard industries by COVID-19

Closed stores, travel bans, or cancelled conferences are some of the measures imposed in order to combat the spread of the virus of 2020. Plenty of businesses are struggling to get back on their feet and consumers’ worries keep rising after new cases emerge. China is one of the main concerns among industries, as the virus concentration is much greater in this country and the number of stores closing and shoppers sheltering at home are increasing. However, the initially-Wuhan epidemic has now expanded far beyond the Chinese city.

The travel industry is one of the largest industries in the world, with revenues around $5.7 trillion. But now, it’s being hit by travel restrictions and cancelled trips prompting a crisis towards this industry and dragging down the global economy. The international Air Transport Association, IATA, warned that global demand for air travel could fall in as much as $30 billion in revenues, the first time in 10 years. These would correspond to a 4.7% hit in global demand levels, corresponding to a 0.6% global contraction given the 4.1% expected growth for 2020.

Many big shows have been cancelled already, in an attempt to control the outbreak of the virus. Among them are Geneva Motor Show, Facebook’s F8 conference or ironically enough the leading trade show for the travel industry itself, ITB Berlin. Many companies’ business trips are also on hold, concerned about the employee’s exposure. British Airways, Ryanair, Lufthansa and EasyJet have already been forced to cancel hundreds of flights, as the airlines industry body has already warned of a falling number of passengers. Some of them are resorting to price cuts on short-haul flights, in order to dodge demand breaks.

In the tech industry, companies are already sensing the damages being caused by COVID-19 as well. The first ones being those with direct exposure to China, the supply chain of which is so dependent on this country, causing several companies to have issued a financial warning regarding the consequences of the pandemic.

Moreover, shortages in supply are expected in various products ranging from smartphones, headsets or even cars. The manufacturer Foxconn, known to be the main assembler of Apple, has stopped almost all of its production in China, who’s accountable for 75% of the production capacity of the firm. Foxconn’s revenues are down 10% compared to last year’s period. The disruption in the company’s operations has prompted questions regarding the dependence on this geographic location.

Why can this affect the global economy?

The reason is simple: China. Bear in mind that we are talking about the second biggest economy in the world and the world’s largest manufacturing and exporter of goods. Besides losses in China due to decreases in consumer spending and stores closing, the impact will extend beyond the Wuhan province.

Since the outbreak of the COVID-19 virus, there has been a tremendous amount of stoppages and even lockdowns in China’s factories, as only about 50% of them haven’t yet been harmed by the spread of the virus. This not only affects production, but also sales, since people are forced to stay at home, hence, not spending money on a wide variety of products. Furthermore, sales in China are not the only ones doomed to failure this first trimester, as sales in a lot of different sectors outside China are now compromised due to the disruption of supply chains created by all the lockdowns that have been occurring. So, basically, any company directly working with China, as for raw materials or any work in progress goods, is most likely being impacted since, a lot of companies in Europe and the United States are receiving their orders with weeks of delay and some of these can’t even sail through the Ocean due to requirements of a minimum amount of goods to fill the ships, which are simply not coming through.

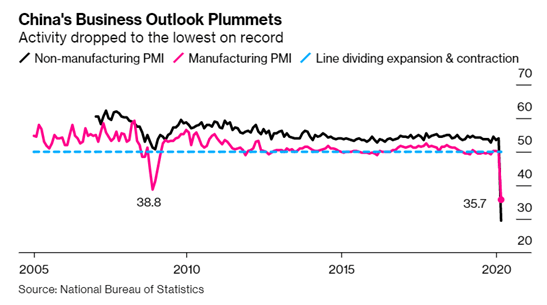

By looking at the Purchasing Managers’ Index (PMI), we can understand how severe the coronavirus has been to China’s economy given the fact that in 2008’s global recession this index had hit a low of a 38.8 score (to provide some insight, any score below 50 shows that there are more purchasing managers, in the manufacturing sector, indicating a contraction in this sector). Besides this concerning value, the IMF stated that the global spread of COVID-19 will damage economic growth for 2020. After the easement of the US-China trade relations, growth for this year was expected to surpass 2019 , whereas now “Global growth in 2020 will dip below last year’s levels, but how far it will fall and how long the impact will be is still difficult to predict” as the Managing Director of the IMF Kristalina Giorgieva said last week. This means a revision of 0.4% or higher compared to the values expected in January.

Although it is to be known at what extent, we can definitely agree that COVID-19 is taking a toll on the economy and may even have lasting effects in our lives. What remains to know is how Governments and Central Banks will react and how are investors limiting losses and even making gains during this period.

Sources: Bloomberg Intelligence, Market Watch, The Washington Post, CNBC, Financial Times

João Ribeiro

João Ribeiro  Matilde Mota

Matilde Mota

Martim Leong

Martim Leong  Francisco Nunes

Francisco Nunes