Throughout history, disparities about the definition of social justice, across regions, led countries to adopt different income-tax systems (1). Despite being the most accepted, the progressive way of taxes has been increasingly questioned by academics and political leaders, arguing that a flat-tax system would be a better fit for countries regarding fairness and economic dynamics.

What distinguishes a flat rate from a progressive rate?

Simply put, a flat income-tax system applies the same income-tax rate to all taxpayers, regardless of their income level. Contrarily, a progressive system increases the rate as the income level increases, where the income range can vary greatly, depending on the country.

On the one hand, those who defend the first method argue that it is unfair to charge higher-income individuals a greater tax rate. The rationale behind this position is that they should not be penalized for adding more value to the economy. On the other hand, supporters of the progressive system believe that income distribution before taxes is not fair, i.e., earnings do not necessarily match economic contribution. Furthermore, wealthier households are considered to have the moral duty to aid those struggling. In their view, adjustments are needed and desirable.

Historically, the progressive system has been prevailing in most developed Western countries. In the USA, for instance, only 9 states (Colorado, Illinois, Indiana, Kentucky, Massachusetts, Michigan, North Carolina, Pennsylvania and Utah) out of 50 have a flat income-tax. In turn, only 8 of the 36 OECD member countries currently have a somewhat flat system (Czech Republic, Denmark, Estonia, Hungary, Iceland, Ireland, Poland and Sweden) (2).

In order to accurately address the origins and the main effects of a flat-tax system, some of the referred countries will be used as case-studies in this article.

What caused some countries to adopt a flat-tax system?

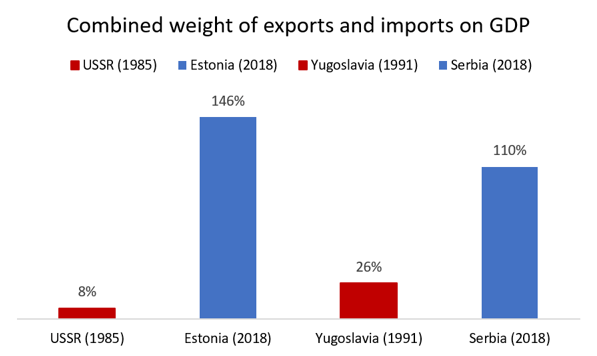

It is not a coincidence that most European countries which adopted a flat-tax system were once part of a bigger state. Estonia, for instance, which is perhaps the successful case in the adoption of a flat-tax (1994), was part of the USSR until its breakup in 1991, as well as Latvia (1994), Lithuania (1995) and Georgia (2005). In turn, Serbia and Montenegro, which adopted a flat tax in 2003 and 2007, respectively, are former members of Yugoslavia.

What these countries have in common is the lack of openness of their economies prior to their independence, as seen in the graph. Nowadays, approximately thirty years after the breakup of their previous federations, countries like Estonia and Serbia have shown an intensive internationalization process. Indeed, economic history tells us that global trade increases the welfare of nations. Therefore, it seems logical that former USSR and Yugoslavia members would aim at opening their economies so that they could thrive and catch up with Central and Western European more developed states.

Data source: The Global Economy

In a report for The Heritage Foundation, Mart Laar, former liberal-conservative Prime Minister of Estonia (1992-1994; 1999-2002), explained that, when the USSR broke up and the country conquered its independence, the Russian ruble no longer had any value, Estonian industrial production declined by more than 30%, real wages fell by 45%, while inflation was running at more than 1000%. GDP per capita in the country was at $2,000, compared to the $14,370 attained by the Finnish neighbours. This Baltic country was totally devastated, after being pushed to the limit by Moscow, hence lacking urgent and impactful policies to invert its economic path.

Among a set of important measures to stabilize and boost the economy such as the introduction of an own currency (the kroon) which was pegged to the German mark, and balanced Government budgets, openness to global markets also played a significant role by fostering competition and attracting direct foreign investment. Nonetheless, the decisive move «to achieve a lasting breakthrough in Estonia’s development» would be the flat tax.

In the words of Laar, it was all about providing the right incentives to people:

“when people who had started companies realized that the tax system punished success, their enthusiasm to persevere and determine their own future declined considerably”

Similarly, in Lithuania and Latvia, nations that share many characteristics with Estonia (these three would become known as Baltic Tigers), the flat tax was introduced to improve the economic outlook after Soviet ruling. Besides, they had to compete with Estonia for foreign investment, for which fiscal policy was a powerful tool. On the other hand, in Russia and Ukraine, the flat-tax was introduced mainly to incentivize higher-income households not to evade their taxes.

How does flat taxation impact economies and societies?

Despite all the positive results political leaders aimed at achieving with a flat-tax system, do/did they really happen? Looking at tax revenue, GDP per capita, income reporting and tax compliance and Gini Index, we can take some conclusions.

Regarding tax revenue, the year immediately after Russia changed from progressive (12%, 20% and 30% rates) to flat taxation (13% in 2001), personal income-tax revenues increased 26% in real terms and 2% as a percentage of GDP, a working paper of the IMF from 2005 concluded. In the case of all Baltic Tigers, Deena Greenberg, despite finding out in the paper The Flat Tax: An Examination of the Baltic States that tax revenue increased after the adoption of a flat tax, could not conclude that both were linked, leaving space for ambiguity as for the effect of flat taxation on personal income-tax revenue. Nevertheless, the fact that these countries decreased their tax rate after some years raises doubts on the effectiveness of this method.

Data source: Taylor & Francis Online

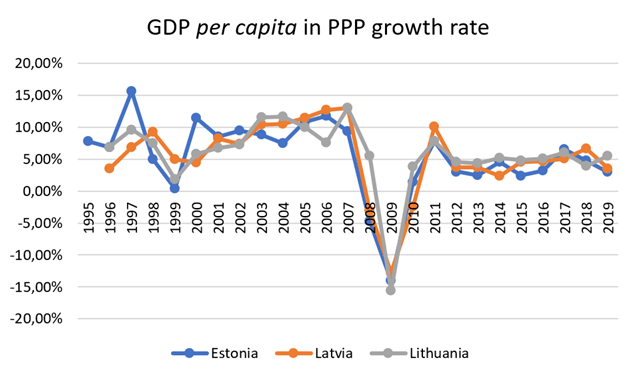

Analysing the evolution of real GDP per capita of some European countries with flat taxation, there is a clear trend: all of them grow significantly in the first years after its introduction, but then growth rates slow down. However, this has more to do with their historical precedents and consequent policies (macro stabilization, property reforms, openness to trade) than with the adoption of the flat tax itself. They happened simultaneously, which may induce misleading conclusions. So, it doesn’t seem to be enough evidence that GDP per capita improvements in these countries over time are due to flat taxation.

Data source: AMECO

In terms of income reporting and tax compliance, it is not clear that a flat tax improves the standards, as the study ‘Flattening’ tax evasion? (2019) concludes by analysing a set of transition European countries. The already referred working paper from the IMF (2005), though, points out that tax compliance in Russia increased after the introduction of a flat tax. Therefore, despite not being totally clear, we could admit some positive impact of a flat tax in tax compliance, especially in less developed countries, in which standards are low.

From an inequality point of view, the Gini Index gives us an accurate insight. The higher the index, the higher the inequality. In this regard, findings are that flat taxation is positively correlated with income inequality, as the following table shows.

Data source: World Bank

All in all, income inequality ends up being a determinant when it comes to deciding which taxation system to use. Despite being correlated with economic improvements, there is no clear evidence that flat taxation plays a role in them. The fact that Slovakia (2013) and Latvia (2018) have recently abandoned their flat systems in favour of the progressive method should be a matter of reflection. Even though the social justice argument is debatable, the economic side does not seem to support flat-tax admirers.

(1) For the sake of this article, only personal income was considered.

(2) Although only Estonia has a perfectly flat tax system, the remaining countries are included in the list either because they consider very few income ranges or because higher tax rates are charged only to abnormally wealthy individuals.

Sources:

AMECO, Deena Greenberg, European Central Bank, European Commission, Global Tax News, International Monetary Fund, LSE Blogs, ProPublica, Taylor and Francis Online, The Balance, The Global Economy, The Heritage Foundation, The Slovak Spectator, Verena Fritz, World Bank