Is the world entering a multipolarity era?

For roughly three decades following the collapse of the Soviet Union in 1991, the United States stood as the world’s unchallenged superpower. Political scientist Charles Krauthammer famously described this era as the “Unipolar Moment”, a period in which no other nation could rival American military, economic, or diplomatic reach. Today, that moment appears to be ending.

A convergence of forces (e.g., the economic ascent of China, the expansion of the BRICS bloc, shifting US foreign policy, and the growing assertiveness of the Global South) is reshaping the international order at a pace that few anticipated.

The Architecture of American Dominance

To understand what is changing, it is necessary to understand what it once was.

After the Cold War, the United States accounted for roughly 25% of global GDP, operated the world’s most powerful military by a significant margin, and anchored a network of international institutions (think of the United Nations, the World Trade Organization, and the International Monetary Fund) that largely reflected Western values and priorities. The US dollar became the world’s dominant reserve currency, giving Washington extraordinary leverage over the global financial system.

This period of unipolarity was not simply a matter of military might: it was a comprehensive structural dominance spanning economics, technology, culture, and governance.

The Rise of New Powers

That architecture is now under sustained pressure.

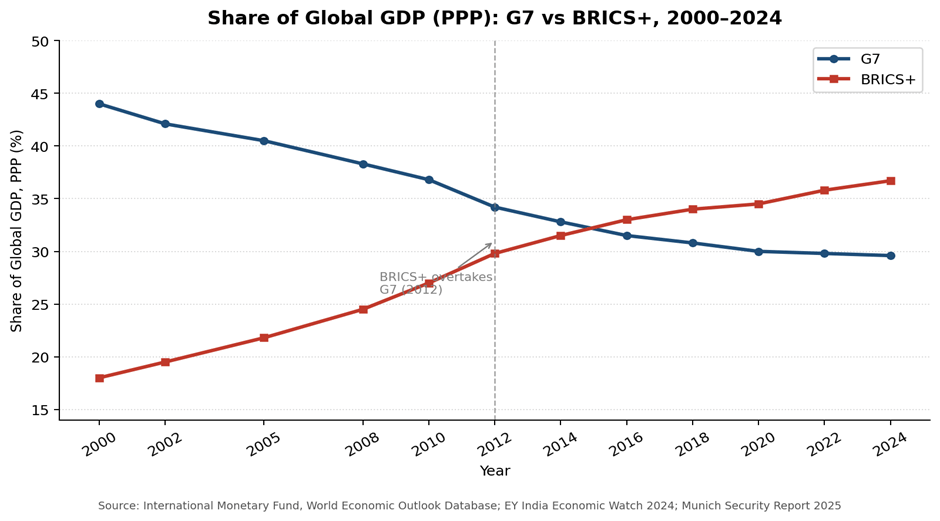

The most significant challenge comes from China, whose economy has grown from approximately $1.2 trillion in 2000 to over $18 trillion today, a rise from 4% to nearly 18% of global GDP. Simultaneously, the BRICS bloc (originally comprising Brazil, Russia, India, China, and South Africa) has expanded aggressively, and as of 2026 represents over 36% of global GDP measured in purchasing power parity (PPP), already surpassing the G7’s share of roughly 29.6%, according to IMF data.

This is not merely an economic story. The BRICS nations collectively account for approximately 40% of global trade, according to the Munich Security Report 2025, whose central theme was precisely “Multipolarization”. The report observed that an ongoing power shift toward a greater number of states vying for influence is clearly discernible, marking a decisive shift in the language of mainstream international security analysis. Beyond BRICS, middle powers including Turkey, Saudi Arabia, India, Indonesia, and Brazil are increasingly acting as independent actors rather than automatic supporters of the Western-led order. At the 2025 Munich Security Conference, 30% of speakers represented the Global South, a figure that would have been unthinkable a decade ago.

Fracturing Alliances and US Foreign Policy

The second major driver of change is the United States itself.

The return of Donald Trump to the White House in January 2025 accelerated tensions already present within the Western alliance system.

Trump’s approach, characterized by tariff escalation, skepticism toward NATO burden-sharing, and unilateral diplomatic maneuvering, strained relations with traditional partners in Europe and Asia. Europe, long dependent on US security guarantees, responded by dramatically increasing defense spending, though analysts note it will remain reliant on American military infrastructure for years to come.

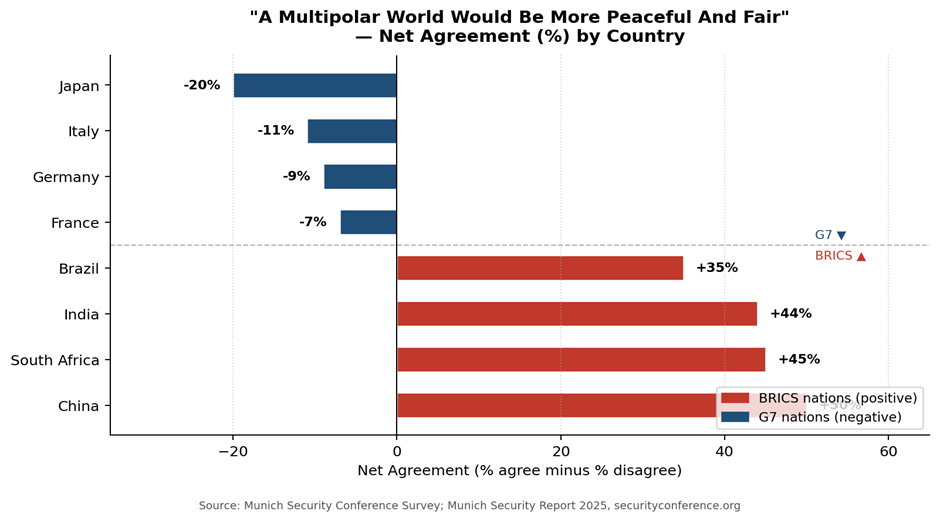

At the same time, a growing divergence is visible in how different parts of the world perceive the emerging order. Surveys conducted for the Munich Security Report 2025 found that majorities in G7 nations view the shift toward multipolarity with concern, fearing increased disorder and conflict. By contrast, large majorities in China (+50% net agreement), South Africa (+45%), India (+44%), and Brazil (+35%) believe a multipolar world would better address the needs of developing nations. The North-South divide has rarely been so sharply quantified.

The Dollar, The Military, And the Limits of Decline

The narrative of American decline is, however, contested by several analysts. Writing in Foreign Affairs in February 2026, analyst C. Raja Mohan argued that “the first year of Trump’s second term has punctured the narrative of American decline and the rise of multipolarity,” pointing to the US ability to intervene militarily, reshape trade rules, and push resolutions through the UN Security Council with limited effective resistance.

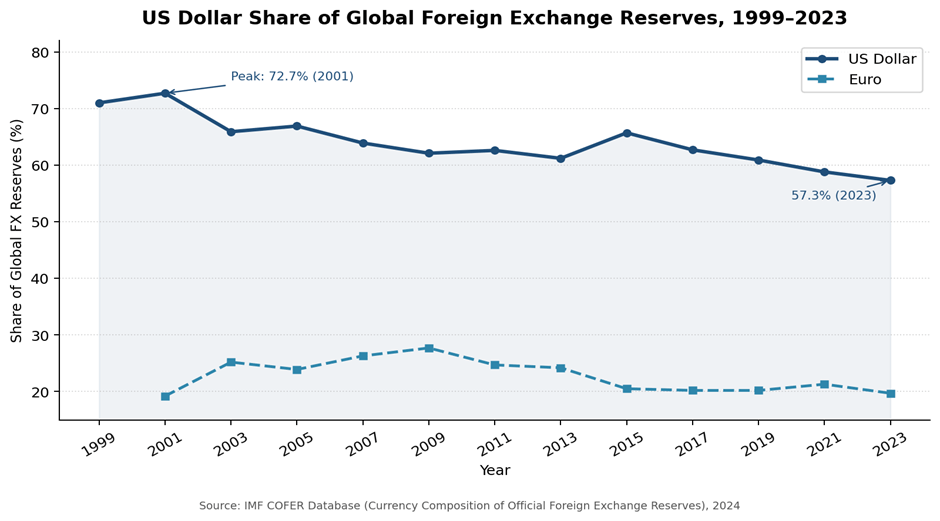

A key pillar of this argument is financial. The US dollar still accounts for approximately 57% of global foreign exchange reserves, according to IMF COFER data, down from a peak of nearly 73% in 2001, but still far ahead of any rival currency. The euro, its closest competitor, holds under 20%. Efforts by BRICS nations to launch an alternative reserve currency or payment system have so far failed to gain traction, with even the BRICS Development Bank continuing to operate primarily in US dollars. Beyond finance, the US continues to dominate the sectors most critical to 21st-century power: artificial intelligence, semiconductor technology, and advanced military systems. Russia, often cited as a pillar of a new multipolar order, has a GDP smaller than that of Italy and a narrow economic base heavily dependent on natural resource exports.

As the Munich Security Report 2025 concluded with notable precision: “Today’s international system shows elements of unipolarity, bipolarity, multipolarity, and nonpolarity. What you see depends on where you look.”

What Multipolarity Would Mean in Practice

Regardless of how the academic debate is resolved, the practical consequences of the current transition are already visible. Multilateral institutions are under strain: the WTO’s dispute resolution mechanism remains largely paralyzed, the UN Security Council is increasingly deadlocked, and global supply chains are fragmenting along geopolitical lines, a process known as “friend-shoring”, as nations prioritize strategic alignment over economic efficiency.

Some analysts see opportunity in this transition. Chatham House researcher Amitav Acharya has argued that a “multiplex” world order could emerge, one characterized by greater ideological diversity, more inclusive global institutions, and stronger regional governance. The inclusion of the African Union in the G20 in 2023 was cited as a potential sign of this more representative direction. The Munich Security Report 2025 cautioned, however, that without shared rules, multipolarization risks producing not a fairer world but a more conflictual one:

“Before our eyes, we are seeing the negative scenario of a more multipolar world materialize — a more conflictual world without shared rules and effective multilateral cooperation.”

Conclusion

The world of 2026 is no longer the world of 1995. While the United States retains unmatched military capability and continues to anchor the global financial system, its ability to set the terms of international order unilaterally has measurably diminished.

The rise of China and the BRICS bloc, combined with a more assertive Global South and an increasingly transactional US foreign policy, are producing a structural transition whose ultimate destination remains unclear. What is certain is that the rules, institutions, and alliances that defined the post-Cold War era are under revision and the outcome of that revision will shape the next several decades of global politics.

Sources

Munich Security Conference, Munich Security Report 2025 C. Raja Mohan, “The Multipolar Delusion,” Foreign Affairs, February 2026 ; Brandon J. Weichert, “The Unipolar Moment Is Over,” The National Interest, December 2025 (nationalinterest.org); Amitav Acharya, “The Decline of the West and the Rise of the Rest,” The World Today, Chatham House, December 2025 (chathamhouse.org); Centre for International Governance Innovation, “America’s Unipolar Moment Is Over” (cigionline.org); MD. Abir Mahmud Jakaria, “Global Power Shift: Is the United States Losing Dominance in the Emerging Multipolar World Order?” ResearchGate, February 2026 (researchgate.net); Indian Journal of Law and Legal Research, “The Rise of Multipolarity: Is the Unipolar World Order Officially Over?” February 2026 (ijllr.com); IMF, World Economic Outlook Database (imf.org); IMF, COFER Database — Currency Composition of Official Foreign Exchange Reserves (imf.org); EY India Economic Watch, “Can BRICS Play a Key Role in Shaping Future Global Economic Policy?” 2024 (ey.com); BRICS Brazil Presidency, “BRICS GDP Outperforms Global Average”

Rebecca Fratello

Writer