On February 28, 2026, U.S. and Israeli forces launched strikes on Iran, triggering a conflict that sent shockwaves far beyond the Middle East. Within days, one of the world’s most critical energy arteries, the Strait of Hormuz, was declared closed by Iranianforces, causing what the International Energy Agency (IEA) has defined as the “largest supply disruption in the history of the global oil market.”

Oil prices have reached levels not seen in years and inflationary pressures are mounting globally. To understand how bad this crisis actually is, one must first understand the centrality of the Strait of Hormuz to the global energy system.

The Strait of Hormuz: The World’s Most Critical Chokepoint

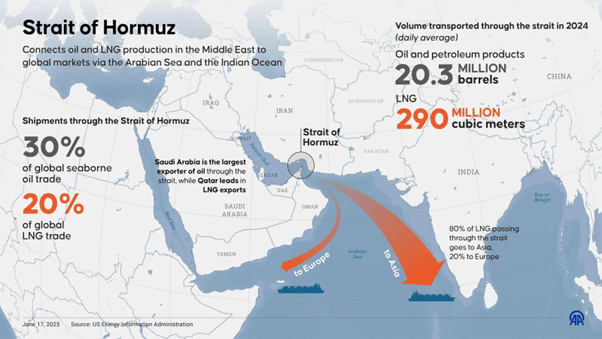

The Strait of Hormuz is a narrow waterway, barely 33 kilometres wide at its narrowest point, separating Iran from Oman. Yet through this sliver of ocean flows roughly 27-30% of the world’s maritime crude oil and petroleum trade, along with significant volumes of liquefied natural gas (LNG). Any disruption here is felt almost immediately in markets from Tokyo to London.

Starting on March 4, 2026, Iranian forces declared the Strait “closed,” threatening and attacking on vessels attempting transit. Oil-producing nations of the Gulf (Kuwait, Iraq, Saudi Arabia, and the UAE) saw their collective output drop by at least 10 million barrels per day by mid-March. QatarEnergy, the world’s largest LNG exporter, declared force majeure on all its contracts as tankers could not leave the Gulf.

To notice is that Asian economies together receive around 84% of crude oil and 83% of LNG transiting the Strait, hence being the ones most exposed.

Figure 1: The Strait of Hormuz, through which roughly 30% of the world’s seaborne oil trade passes. Source: Forbes.

A Shock Without Precedent: Price Surges and Market Volatility

Oil markets have not been a stranger to geopolitical shocks.

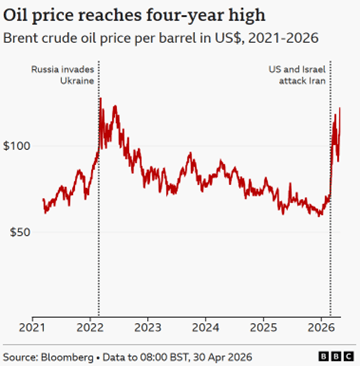

When Russia invaded Ukraine in February 2022, Brent crude surged past $100 per barrel as markets priced in the risk of supply disruptions from one of the world’s largest energy producers. That spike, dramatic as it was, didn’t last long.

The 2026 Iran war, instead, has produced a shock of an entirely different magnitude. As the chart below illustrates, the current price surge has already eclipsed the Russia-Ukraine spike in both speed and scale.

As the Strait closed and Gulf output collapsed, prices climbed relentlessly. March 2026 saw one of the largest single-month oil price jumps ever recorded: Brent gained 51% in a single month, peaking at nearly $120 per barrel. By late April, with peace negotiations stalled and the Strait still functionally closed, Brent briefly touched $126, a four-year high not seen since the most acute phase of the Russia-Ukraine energy crisis.

Figure 2: Brent crude oil price per barrel (US$), 2021–2026. The chart highlights two defining shocks: the 2022 Russia-Ukraine spike and the steeper, faster surge following the US and Israel attack on Iran in February 2026. Source: Bloomberg / BBC News, data to 30 Apr 2026.

But it is not only price levels that make these two events different. The 2022 shock was driven by fears of reduced Russian supply, which the market eventually adapted to through rerouted trade flows. The 2026 crisis saw the physical closure of a chokepointthrough which there is no realistic alternative route for most Gulf producers.

“The market hasn’t seen the full impact of that yet. There’s more to come if the strait remains closed.”

Darren Woods (CEO of Exxon Mobil, May 1, 2026)

Ripple Effects: The Global Economy Under Pressure

The impact of this supply shock extends well beyond gasoline prices. Inflation and stagflation risk have moved to the top of the agenda for central banks. Analysts have forecast that if disruptions persist, global inflation could rise by up to 0.8 percentagepoints, with the risk of stagflation, a combination of slow growth and rising prices, for major economies. The United Nations Secretary-General warned that if the war continues throughout 2026, the world will “confront the specter of a global recession,” addingthat “the consequences are not cumulative – they are exponential.”

The Gulf Cooperation Council (GCC) states themselves have not been spared. Over 80% of the region’s caloric intake is imported via the Strait, and by mid-March roughly 70% of food imports were disrupted, creating a concurrent grocery supply emergency. This adds a wider humanitarian dimension to what began as an energy crisis.

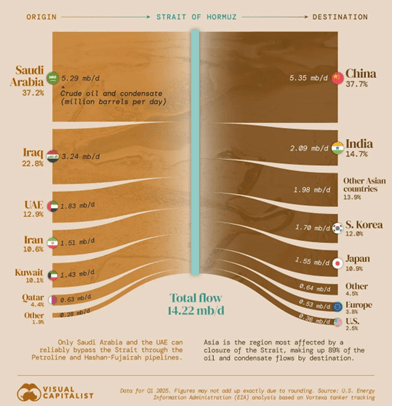

Figure 3: Crude oil and condensate exports through the Strait of Hormuz by destination country (Q1 2025). China alone accounts for 37.7% of total flows, followed by India (14.7%), South Korea (12.0%), and Japan (10.9%) Source: Visual Capitalist / U.S. Energy InformationAdministration (EIA).

The Philippines became the first country to declare a national energy emergency on March 24, 2026, importing 98% of its oil from the Middle East. Nepal restricted gas cylinder refills. Myanmar imposed alternate-day driving rules. Aviation has beenseverely disrupted across flight corridors linking Africa, Asia, and Europe.

Meanwhile, the crisis has created stark divides: the United States, as the world’s largest oil producer, saw crude and petroleum exports surge to nearly 12.9 million barrels per day in April 2026, while oil-importing nations in Asia and Africa bore the heaviest burden.

Looking Ahead: What Comes Next?

As of early May 2026, the situation remains deeply uncertain. Brent crude is trading around $108–$112 per barrel, lurching with every twist in diplomatic negotiations conducted through Pakistani mediators. Commodity Context founder Rory Johnston has cautioned that even a sustained reopening of the Strait would trigger only a temporary price relief, as supply chain bottlenecks, infrastructure damage, and production outages would likely anchor Brent in the $80–$90 range, well above pre-crisis levels, for the foreseeable future.

The damage to LNG infrastructure compounds the problem. Qatar’s Ras Laffan complex, struck by Iranian missiles on March 18, faces an estimated 3 to 5 years of repair work, sending LNG spot prices in Asia up by over 140%. With strategic petroleumreserves being drawn down and commercial inventories depleted, Exxon’s Woods has warned that prices may need to rise further to curb demand once those buffers run out.

The crisis has also injected new urgency into the debate around energy security and the green transition.

As the chart above makes clear, oil markets remain acutely vulnerable to geopolitical disruption. Whether the lesson is finally taken seriously may prove to be one of the most consequential legacies of the 2026 Iran war.

Sources

CNBC; Bloomberg; Forbes; CBS News; Congressional Research Service; BBC News; Reuters; Visual Capitalist; U.S. Energy Information Administration (EIA)

Rebecca Fratello

Writer