In 1776, Adam Smith wrote, in An inquiry into the nature and causes of the wealth of nations, that “The acquisition of talents during education, study, or apprenticeship, costs a real expense, which is capital in a person. Those talents are part of his fortune and likewise that of society”. This idea might seem quite intuitive for an inhabitant of the world in the 21st century, and even the greenest economist would associate these words with the foundation of Human Capital.

However, until the last century, this concept was actually quite unpopular. As Theodore Shultz points out in Investment in Human Capital (1961), investment in human is not devoid of moral and philosophical issues. His words, “It seems to reduce man once again to a mere material component, to something akin to property”, are especially evocative, considering the 13th Amendment to U.S. constitution, which abolished slavery, had entered into force not even one century before.

With the advent of statistics and nation-level measurements in the period of WW2, researchers started to observe that increases in national output could not be fully explained by increases in physical capital. It became possible to link the accumulation of skills, capabilities and knowledge humans with these unexplained variations in growth.

Today, the World Bank defines Human Capital as “The knowledge, skills, and health that people invest in and accumulate throughout their lives, enabling them to realize their potential as productive members of society.”

But what aspects of the multifaceted human being are included in this definition? Reading further, the WB specifies: “Investing in people through nutrition, health care, quality education, jobs and skills helps develop human capital, and this is key to ending extreme poverty and creating more inclusive societies.”

Human Relationships as Capital

After accepting the “capitalization” of individual’s traits, a more recent step has been recognizing that humans are social animals, and therefore, their relationships are a fortune too. The concept of Social Capital generally refers to social relationships between people that have productive outcomes. In a nutshell, Portes (1998) explains it as “whereas economic capital is in people’s bank accounts and human capital is inside their heads, social capital inheres in the structure of their relationships”.

Social capital is for sure a peculiar form of capital: it does not reside in any individual entity, but it’s embedded in society, it lies in relationships, it’s rooted in networks. However, just like any other type of capital, it requires investment and maintenance to yield returns.

If defining the determinants of human capital is not an obvious task, defining those of social capital is even more challenging. The Institute for Social Capital indicates a range of dimensions including trust, togetherness, volunteerism, generalized norms, everyday sociability, and neighborhood connections.

In essence, applying this theory, helping an old lady cross the street, having a neighbor who looks after your child when you’re sick, or trusting the police—all of these actions contribute to a web of reciprocity that will eventually benefit either the individual or the broader society.

Just as human capital was initially controversial, social capital was—and perhaps still is—a contested concept. For sure, its reputation increased after the publication of Making Democracy Work: Civic Traditions in Modern Italy by the political scientist Robert Putnam. Focusing on Italian regional governments, he found how government performance was strictly linked to traditions of civic engagement.

Friendship as Social Capital

Within this broader framework, friendship emerges as a particularly powerful and personal expression of social capital — one that not only supports emotional well-being but also shapes long-term economic and social outcomes.

If friendship is part of human capital, then it somehow has impacts that extend beyond the individual to society at large. And it might be more powerful than one can think. In a 2022 study on networks and friendships, Raj Chetty’s and colleagues found that education, racial segregation, education, and family structure were not as important as cross-class connections in determining upward social-mobility. In fact, among all observed components of social capital, friendship across socioeconomic lines was the only one driving mobility. Social cohesion and civic engagement, by contrast, did not seem to play a role.

The relationship between friends also shapes the social tissue of communities. In Bowling Alone, Putnam describes how American society, one strong and civic engaged, is now degrading through the whimsical metaphor of bowling. The evocation of many lonely bowlers, with a nostalgic comparison to bowling leagues playing together, reflects the individualist derive of society. From this point of view, friendship and social interactions are a sort of public good, and not just a private comfort. The weaking of these relationships has consequences that go beyond individual loneliness, but undermine the health of society.

Relationships and Policy Makers

Friendships, connections, networks, and trust — they all contribute to both individual well-being and a healthier, more cohesive society. Yet we rarely hear politicians or policymakers address these topics directly. In an era where society is becoming increasingly individualistic, the case for investing in social capital becomes even more urgent. Urban planning, for instance, can be intentionally designed to promote cross-class connections and neighborhood friendships. The creation of public and recreational spaces that facilitate meeting and incentive people to socialize, promotion of sports and community strengthening activities can be impactful policies for boosting social capital. Reinvesting in friendships and ways of making them happen it’s not just about enhancing well-being, it’s a necessary step to rebuild a strong social fabric, that can sometimes be as important as and educated or healthy community.

Putnam, R. D., Leonardi, R., & Nonetti, R. Y. (1993). Making Democracy Work: Civic Traditions in Modern Italy. Princeton University Press. https://doi.org/10.2307/j.ctt7s8r7

Putnam, R. D., “Bowling Alone: America’s Declining Social Capital” Journal of Democracy, January 1995, pp. 65-78.

Tariffs have always been a contentious tool in global economic policy, and former President Donald Trump’s administration relied heavily on them to reshape America’s trade relationships. Trump’s approach to tariffs was characterized by the belief that they would protect American industries, reduce the trade deficit, and pressure foreign partners into negotiating more favorable deals for the United States. However, the actual effects of these tariffs have been complex and far-reaching, influencing everything from global supply chains to consumer prices. This article explores the potential and actual impacts of Trump’s tariffs on markets and international trade, offering examples, economic analysis, and perspectives from multiple sources.

What Are Tariffs and Why Did Donald Trump Use Them?

Tariffs are taxes imposed on imported goods. By making foreign goods more expensive, tariffs are intended to encourage consumers to buy domestic alternatives. Trump saw tariffs as a tool to reduce America’s trade deficit, particularly with China, and to protect domestic industries like steel, aluminum, and technology manufacturing.

Key Examples of Trump’s Tariffs:

In 2018, Trump imposed a 25% tariff on steel imports and a 10% tariff on aluminum.

In the same year, the administration slapped tariffs on $250 billion worth of Chinese goods, leading China to retaliate with tariffs on American products like soybeans, cars, and airplanes.

In 2020, Trump threatened additional tariffs on European Union exports such as wine, cheese, and aircraft parts in retaliation for EU subsidies to Airbus.

How Tariffs Affect Domestic Markets

1. Higher Costs for Consumers

While tariffs target foreign producers, the actual cost burden often falls on domestic consumers. Importers pass higher costs onto consumers, making everything from cars to electronics more expensive. A study by the Federal Reserve Bank of New York estimated that by the end of 2019, Trump’s tariffs cost the average American household about $831 per year due to higher prices.

Example: When tariffs were imposed on washing machines in 2018, prices jumped nearly 12% within months, according to research published by economists at the University of Chicago and the Federal Reserve.

2. Disruption of Supply Chains

Many U.S. industries depend on imported components and raw materials. Tariffs on Chinese technology parts, for instance, disrupted the electronics and automotive sectors, which rely heavily on Chinese factories for affordable parts. This forced companies to either raise prices or absorb losses, weakening profit margins and investment. In the long run, some firms moved production out of China, but this led to higher transition costs and inefficiencies.

Impact on International Trade

1. Retaliatory Tariffs and Trade Wars

When the U.S. imposed tariffs, trading partners retaliated with their own tariffs. China targeted American agricultural exports, including soybeans, corn, and pork, hurting U.S. farmers who relied on the Chinese market. By mid-2019, U.S. agricultural exports to China had fallen by 53% compared to 2017.

Example: The American soybean industry suffered particularly harsh consequences. Before tariffs, China imported about $12 billion worth of U.S. soybeans annually. By 2019, that number dropped to under $3 billion. The U.S. government ended up subsidizing farmers to offset their losses, costing taxpayers billions. (Source: Bloomberg, 2019)

2. Erosion of Trade Alliances

Trump’s unilateral use of tariffs alienated key allies, including the European Union, Canada, and Mexico. When Trump imposed steel and aluminum tariffs, both Canada and the EU retaliated with tariffs on iconic American products, from Harley-Davidson motorcycles to bourbon whiskey. This strained long-standing trade relationships, particularly within the World Trade Organization (WTO) framework, which is built on predictable, rules-based trade.

Effects on Financial Markets

1. Market Volatility

Trump’s tariff announcements often led to immediate stock market swings. When tariffs on China were announced in March 2018, the Dow Jones Industrial Average plunged 724 points in a single day, reflecting investor fears of a full-blown trade war disrupting global economic growth.

2. Sectoral Winners and Losers

Some sectors benefited from protectionism, particularly domestic steel producers. However, industries reliant on steel (like automotive and construction) faced rising costs, eroding their competitiveness. Agricultural stocks, particularly in soybeans and pork, plummeted due to lost export markets.

Long-Term Economic Impacts

1. Reshoring vs. Offshoring Diversification

One goal of the tariffs was to bring manufacturing back to the U.S., a process called reshoring. Some companies did shift production, but many opted to diversify away from China to other low-cost countries like Vietnam, Mexico, and Thailand instead. This resulted in a fragmentation of global supply chains, increasing overall uncertainty.

2. Reduced Global Trade Growth

The uncertainty surrounding U.S. trade policy under Trump contributed to slower global trade growth. According to the World Bank, global trade growth fell from 5.4% in 2017 to just 1.1% in 2019, with tariffs playing a significant role.

Case Study: The U.S.-China Trade War

The most high-profile example of Trump’s tariff policy was the U.S.-China Trade War, which began in 2018. It involved escalating tariffs on hundreds of billions of dollars in goods on both sides. The conflict led to:

Higher costs for American businesses and consumers.

Reduced Chinese investment in the U.S..

A reshaping of Asian supply chains, with companies shifting production to Southeast Asia.

Ironically, despite Trump’s goals, the U.S. trade deficit with China actually increased in some sectors, as American companies stockpiled Chinese goods before tariffs took full effect.

Trump’s tariffs were a bold attempt to reset global trade dynamics, but the unintended consequences were significant. While they did pressure China into signing Phase One of a trade deal in 2020, they also:

Raised prices for American consumers

Hurt American exporters through retaliation

Increased market volatility

Weakened global trade growth

Undermined trust in the international trade system

As the world moves with the Trump era, policymakers face the challenge of rebuilding stable trade relationships while addressing the legitimate grievances about unfair trade practices, especially concerning China’s industrial subsidies and intellectual property violations. Whether tariffs were the right tool for this job remains hotly debated, but their lasting impact on markets and international trade is undeniable.

Sources

BBC, 2018; Peterson Institute for International Economics, 2020; Federal Reserve Bank of New York, 2019; Flaaen et al., 2019; Harvard Business Review, 2020; Congressional Research Service, 2020; CNBC, 2018; Reuters, 2018; Brookings Institution, 2020; Bloomberg, 2019; World Bank, 2020; Peterson Institute for International Economics, 2020.

On March 10th, the Trump Administration announced that 83 percent of the programs run by the U.S. Agency for International Development (USAID) would be canceled. This decision follows a series of actions targeting USAID, including placing its officials on paid leave, discussing the agency’s potential shutdown, and labeling it as being run by “radical left lunatics” and a corrupt institution that misuses taxpayer money. The first major move came with a freeze on approximately 90% of USAID grants and contracts worldwide—making the latest cuts less surprising.

Feb. 28, 2025, Washington. A senior advisor at USAID, is consoled by a co-worker after having 15 minutes to clear out her belongings from the USAID headquarters, Friday. (AP Photo/Jacquelyn Martin)

In a speech to Congress on March 4th, Trump outlined his reasoning behind these decisions. Reducing “the flagrant waste of taxpayer dollars” is part of his broader strategy to combat inflation, purpose for which the DOGE, the brand-new Department Of Government Efficiency headed by Elon Musk, was created. Trump listed several specific cuts, such as “$8 million to promote LGBTQI+ initiatives in Lesotho, which nobody has ever heard of,” and “$250,000 to increase vegan local climate action innovation in Zambia.” He also mentioned “$47 million for improving learning outcomes in Asia,” sarcastically noting that “Asia is doing very well with learning. You know what we’re doing—could use it ourselves.” Many other initiatives were dismissed as “scams.”

However, while some projects may be debated, the impact of these cuts extends to critical humanitarian aid programs. Initiatives preventing malnutrition and combating diseases such as malaria, polio, and AIDS have been shut down, leaving millions vulnerable around the world.

From a broader perspective, the decision aligns with a reshaped U.S. national interest—one that takes a narrower, more domestic-focused approach. While foreign aid cuts may contribute to reducing inflation, they also risk undermining stability in conflict-prone regions and weakening diplomatic relations. It remains to be seen what the long-term consequences of this decision will be for the US.

Impact on Developing Countries

But what can poor countries’ economies expect from such an abrupt dismantling of USAID?

It is inevitable that many African countries will face a profound distress, especially in the healthcare sector. For instance, in South Africa, 17% of funding for AIDS treatment comes from PEPFAR (the President’s Emergency Plan for AIDS Relief), which also supports the salaries of more than 15,000 healthcare workers. The situation could be even more critical in Ethiopia, USAID’s largest beneficiary, which receives over $200 million annually to support its healthcare system.

However, some argue that heavy reliance on foreign aid is not beneficial for recipient countries. There is no consensus on its overall impact on economic development. Some scholars argue that aid fosters growth through infrastructure improvements, pioneering investments, and attracting foreign capital. Others counter that it distorts labor markets and fosters dependency. Some have also compared foreign aid effects on local economies to the ones of natural resources revenues: these inflows can lead to currency appreciation, making locally produced locally produced tradable goods relatively more expensive and less competitive internationally, triggering the so-called “Dutch Disease” and weaking local manufacturing.

Foreign Aid Received in 2023, in US Dollars and adjusted for inflation. Source: OECD, 2025.

The Debate on Foreign Aid

Criticisms against aid arrive also from other Global South Activists, who claim that aid is just charity covering social injustice and perpetuating the colonialist “civilizing mission”.

One of the most prominent critics is Dambisa Moyo, a global economist born in Zambia and naturalized as an American. In her 2009 book, Dead Aid – Why Aid Is Not Working and How There Is a Better Way for Africa, she challenges the “greatest myths of our time: that billions of dollars in aid sent from wealthy countries to developing African nations has helped to reduce poverty and increase growth”. Moyo argues that foreign aid fuels corruption, distorts local markets, and creates a vicious cycle of dependency—ultimately increasing poverty rather than alleviating it. Moyo proposes the stop of aid funding, throughout the over a period of five years, as a solution to reduce poverty and improve economic growth and development in African countries.

Although Moyo’s plan differs significantly from Trump’s approach and underlying motivations, her perspective raises the question: Could these cuts ultimately push aid-receiving countries toward self-reliance?

Regardless of the answer to this question, Trump’s decision carries profound economic and humanitarian consequences for developing nations reliant on these funds, and challenges the West’s long-standing role in Global South development. If these cuts lead to reduced dependence on Western aid, they could open the door for alternative models and standards—ones that might ultimately foster more sustainable growth for recipient countries and prompt a reevaluation of an international cooperation system that has long been in need of reform.

Arellano, C., Bulíř, A., Lane, T., &Lipschitz, L. (2009). The dynamic implications of foreign aid and its variability. Journal of Development Economics, 88(1), 87-102.

On November 6th, German Chancellor Olaf Scholz announced in a speech to the media having dismissed Finance Minister Christian Lindner. This was followed by a wave of demissions in one of the three parties forming the ruling coalition, essentially making the government collapse. To understand this crisis, it is important to go back in time.

Indeed, Germany’s current political instability is deeply rooted in the nation’s economic challenges over the past decade, shaped by both internal policy decisions and global economic forces. To understand the collapse of the coalition government (a government formed jointly by more than one political party) and the broader political crisis, it is essential to explore the economic context that led to this pivotal moment.

Wirtschaftswunder – “Economic Miracle”

After World War II much of the country was in ruins. Allied Forces had attacked or bombed large parts of its infrastructure. The city of Dresden was completely destroyed, the population of Cologne had dropped from 750,000 to 32,00 inhabitants, Germany was a ruined state facing an incredibly bleak future. Nevertheless, by 1989, when the Berlin Wall fell and Germany was once again reunited, it was the envy and surprise of most of the world.

Germany had the third-biggest economy in the world, trailing only Japan and the United States in terms of GDP. Its post-World War II “economic miracle” was built on industrial excellence, a strong export sector, and a model of social capitalism that balanced growth with social welfare.

By the early 2000s, Germany had established itself as the world’s fourth-largest economy, heavily reliant on the automotive, mechanical engineering, chemical and electronic industries alongside having the most open economy of the G7 states.

Economic Challenges and Impact of Global Events

Even though the country’s growth was exponential and undeniable, flaws in the economic model began to arise. One of them lies with demographic pressures, given the fact that this country´s ageing population has strained its workforce and social welfare systems, particularly pensions and healthcare aligned with an increase inimmigration that reduced innovative minds, falling behind in sectors like digital technology and artificial intelligence, sparkling political debates and polarisation.

Additionally, the overreliance on exports, particularly to China and the United States, left the economy vulnerable to external shocks, such as trade wars and global demand slowdowns. Proof and enhancement of this was the disruption of global supply chains due to Covid-19 Pandemic, that reduced demand for German exports, and forced the government to implement costly stimulus packages, increasing public debt.

Also, because this is a country moved and known for its industrial production, heavily relying on Russian energy, became a direct liability of when the 2022 invasion of Ukraine and subsequent sanctions. This energy crisis had severe industrial impacts on this country’s competitiveness. This conflict exacerbated Germany’s energy crisis, as Russia cut off gas supplies in retaliation for European sanctions, leading to skyrocketing energy costs, prompting a turn towards renewable energy (turn that has faced criticism for its slow implementation and high costs, intensifying debates over the viability of the transaction amid soaring energy prices and industrial pushback), and alternative suppliers but also driving inflation and recession fears.

The Economic Fallout: A Path to Political Crisis

Germany officially entered a period of recession in 2023, marking two quarters of negative GDP growth (-0.1% in Q2 2023 and -0.4% in Q4 2023). Along with high inflation (ranging from 8.7% to 3.7% in 2023), eroding consumer purchasing power, shrank the economy.

German industry leaders expressed frustration over rising taxes and regulatory hurdles, particularly regarding environmental policies, fuelling demands for more pro-business reforms.

This inability of the government to reconcile competing economic philosophies (fiscal austerity, backed by the FDP) with an increased public spending (supported by the SPD and the greens) has been a persistent source of pressure on Germany’s coalition government, reaching a breaking point in November of 2024.

Current crisis

Germany, which had already been facing a strenuous economic downturn as mentioned above, saw its government collapse on November 7th, after Chancellor Olaf Scholz dismissed Finance Minister Christian Lindner over budget disagreements, causing the breakup of the country’s ruling coalition. Since 2021, Germany had been governed by a three-party coalition, commonly referred to as the “traffic light” after the parties’ traditional colours, consisting of the Social Democratic Party of Germany (SPD), The Free Democratic Party of Germany (FDP), and The Greens. When Chancelor Scholz, leader of the SPD, fired Minister Lindner, leader of the FDP, a wave of resignations from the FDP and the party’s withdrawal from the coalition ensued, leaving the government without a majority and prompting a snap election to be scheduled for February of next year. Indeed, Scholz initially announced he would continue working with The Greens in a minority government and call a confidence vote for January 15th which, if lost, could allow elections to be held in March of 2025 instead of September when they would have happened without the turmoil. However, under pressure from the opposition party, the Christian Democratic Union of Germany (CDU), the vote of confidence was pushed to December 11th and, since the government is expected to lose the backing of the parliament, elections have been set for February 23rd according to statements lawmakers and officials from three major parties gave POLITICO. Scholz’s decision to fire Lindner came after months of tensions, mainly regarding the country’s budget policy, since Scholz and the SPD’s left-wing tendencies for government spending on social and environmental policies clash with Lindner and the FDP’s neoliberal advocacy for a free market and a conservative fiscal approach. The governance was therefore certainly not smooth. Last year, for instance, the country found itself in a fiscal scandal when it was discovered that the government had been unlawfully using “special funds” to spend outside the main budget and circumvent the constitutional “debt brake” put in place, which restricts the federal deficit at 35% of GDP, preventing the government from borrowing excessively and amassing debt. After this scandal, the relationships within the coalition kept worsening, as well as public opinion of the government. This year, a week before the events, in the midst of debate on ways to prevent a 10-billion-dollar gap in next year’s budget, a paper written by Lindner listing financial and economic proposals that had not been agreed upon with other parties, including cutting welfare payments, reducing climate protection measures and implementing tax cuts for companies, was madepublic. Lindner then rejected Scholz proposals for the 2025 budget, which included taking out additional debt to bring down energy prices, offer tax benefits to increase investment and increase support for Ukraine. When he addressed the media on the 6th of November, Scholz stated having dismissed Lindner for blocking his economic policies, telling reporters he “showed no willingness to implement any of our proposals” and highlighting the lack of “trust basis for any future cooperation” as he argued that Lindner’s “egoism is totally incomprehensible”. On his side, Lindner reproached Scholz for having demanded a pause on the debt brake.

This political crisis was kickstarted just hours after Donald Trump’s victory in the US elections was announced, an event which not only largely overshadowed the German crisis in the media but could also have even further implications for Germany and the rest of Europe.

Consequences on a national and international scale

Scholz’s government has grown increasingly unpopular in Germany, with Scholz being one of the least popular chancellors ever, according to a CNN opinion poll. In fact, in the European Parliament elections back in June, the traffic light coalition took a blow with Scholz SPD’s recording their worst result in a national vote in over a century, with less than 14% of votes for a party that has been central in the German political landscape for so long. The Greens and the FDP also saw bleak results with 12% and 5% of votes respectively, while the center-right Christian Democrats (CDU), former Chancellor Angela Merkel’s party, were clearly in the lead with more than 30% of the votes. The far-right Alternative for Germany (AfD) also emerged with strong results, finishing second with 16%, a gain of 5 percentage points compared to the 2019 EU election, even though the party’s top two candidates for the election were involved in a series of allegations of misconduct involving suspected espionage and potential Russian influence, and the party’s lead candidate, Maximilian Krah, was forced to stop campaigning after he defended members of Hitler’s Waffen-SS as not “automatically” criminals. Far-right AfD, as well as the recently formed and controversial populist far-left BSW, have increasingly captivated voters disappointed with the main parties.

Friedrich Merz, the leader of the opposition right-wing conservative CDU, was the one to pressure Scholz into holding his vote of confidence sooner. Merz is expected to win in the snap election, according to polls where CDU is leading with 32% of support. In contrast with his predecessor Angela Merkel, Merz has highlighted the need to close the country’s borders to asylum seekers and has used his X account to show his dislike for criminal immigrants as well as gender-inclusive vocabulary. The latter clearly benefits from an earlier election considering his party’s current popularity, while the SPD would need more time to improve its standing. In polls, the SPD stands at just 16 percent, behind the far-right AfD. However, because the CDU has vowed not to form a coalition with the AfD, it could be forced to turn to the SPD despite their different ideologies and views on issues like the financial support for the unemployed put in place by the center-left party or their spending on environmental protection, frowned upon by the CDU. Moreover, based on current fragmentation and polls, they will probably need a third party with which to rule with two main contestants being The Greens, who are not at all politically aligned with the CDU, and the FDP, who are a better fit for the latter with their free-market stance, but seemingly not for the SPD. Furthermore, the FDP is at risk as it stands below the threshold they need to make it into the parliament.

To sum all this up, Germany’s political turmoil seems to be set to last even past the election, which may lead to another bumpy coalition.

All the while this has been happening, Ukraine’s situation has worsened with the beginning of the winter months. Its main allies in the EU, France and Germany, are both dealing with political instability. Furthermore, Trump’s win in the US elections has also left Ukraine in a delicate position as the future president threatened to cut US aid to Ukraine and encouraged Russia to “do whatever the hell they want” to any NATO member that fails to pay its defence bills as part of the Western military alliance. Given these circumstances, Germany, who is the second biggest contributor of military aid to Ukraine after the US, is expected to increase its support as well as strengthen its own defence and influence other European nations to do the same. This seems a rather difficult task with the country’s recent political crisis and unpassed budget for 2025 despite both the CDU and the SPD sharing the same stance on increasing support for Ukraine, with the CDU being even more decisive on the matter.

Trump’s victory also has further implications for Germany as the politician has promised to increase tariffs on imported goods, including German cars, which would certainly worsen the already precarious economic situation.

Conclusion

Reflecting on Germany’s journey, makes evident that the nation has skilfully navigated a path from devastation to resilience, emerging as a powerhouse within Europe. However, its current political and economic state reflects the complexities of trying to maintain this status amidst evolving challenges. From shifts in global markets and energy policies to addressing societal issues like integration and climate change, this country finds itself in a difficult situation to get out of. The choices it makes now, grounded in its historical lessons and forward-thinking policies, will not only shape its domestic stability but also influence the broader European and global order.

Sources: “The Economy in Germany.” 2024.; “The German Economic Miracle Post WWII.” Thomasbeard; “Germany’s Economic Growth Challenges – Economist Intelligence Unit.” Economist Intelligence Unit; VisualEconomik; TRADING ECONOMICS; Fair Observer; “Germany Engulfed; The Guardian; IPS; ZDFheute Nachrichten; Dw.Com; POLITICO

It is well known countries diverge in levels of development which lead us to a world full of inequalities, but did you ever wonder how we ended up in this situation?

Oded Galor argues that, even though there are factors that perpetuate inequalities, the deep-rooted factors that triggered (or not) development were related to population diversity and the geographical profile of each region. Let’s dive into his theory.

Geographical traits

Evidence of geographical differences in the world dates as far back as to when civilizations chose places like the Fertile Crescent, Mesoamerica, and the Yangtze River Valley to settle. These offered rich soils and favorable climates for the domestication of plants and animals, leading to stable food supplies and population growth. The unequal availability of domesticable species across regions meant some societies could develop agriculture more rapidly than others, creating early disparities in wealth and social organization.

Eurasia’s east-west orientation was another key factor, as it facilitated the spread of crops, technologies, and ideas across similar latitudes and climates, resulting in a more rapid and widespread agricultural advancements compared to the north-south axis of Africa and the Americas, where climate varied significantly. Furthermore, areas prone to diseases like malaria (especially in sub-Saharan Africa) which increased infant mortality rates and the sleeping disease which killed or weakened livestock and population, negatively impacted their economic trajectories compared to healthier regions. Later on, large civilizations would also choose not to settle in these regions due to the high mortality rates.

It was due to a lot of geographical traits that the European Miracle happened around the 18-19th century. Europe had proximity to the sea and navigable rivers which was advantageous for trade and many states with different languages which promoted competition and fostered economic growth while China was unified and had a uniform writing system, single language and central control. According to the hydraulic hypothesis by Karl Wittfogel, the fact that Europe depended largely on rainfall compared to China having a network of dams and canals with political centralization also fostered innovation and competition inside Europe. Other advantages of Europe were the Pyrenees, alps and Carpathian Mountains – hurdles that were natural buffers to invasion and the fractal shoreline which made it easy to defend from invaders and encouraged maritime trade. Comparably, China had mountain ranges that offered little protection from centralized imperial rule and no peninsulas apart from Korea which was independent.

Geographical roots of cultural traits

There are some cultural traits with geographical roots responsible for differences in development. For example, regions with higher return on crop cultivation would tend to be more long-term oriented and therefore invest in innovative agriculture or alternative methods even if that meant sacrificing present consumption. Also, in regions where the plough (which required massive upper body strength) was the main tool of agriculture, there was a division of labor (men would work on the fields and women would take care of the house) and a less egalitarian view on women would be passed along generations. Last but not least, areas with uniform climates would generally be more loss-averse and prepare their crops for possible harsh weather while areas with volatile climates between different regions and throughout the year would be more loss-neutral and risk a bit more while cultivating as they could just escape harsh weather by moving to a different region (they did not need to prepare their crops for hypothetical losses).

Population Diversity

Population size and composition were considered wheels of change. Larger populations were more likely to generate greater demand for new goods, tools and practices, as well as exceptional individuals capable of inventing them, and benefited from more extensive specialization, expertise and exchange of ideas through trade. Moreover, as stated in Darwin’s natural selection, any intergenerationally transmitted trait which makes an organism better adapted to their environment, generating more resources, would survive longer, setting human capital formation as a pertinent element of growth.

Social diversity can also explain some of today’s divergences. According to the Serial Founder Effect, the further a region is from Africa the less diverse it is. This happens because populations started settling in Africa 300k years ago and, as they migrated farther away, the less they would mingle with diverse species reducing variety in civilizations. Since social diversity has a contradictory effect, as it spurs cultural cross-pollination of ideas and enhances creativity, fostering tech progress but also provokes conflict and erodes the kind of social coherence necessary for investment in public goods, an intermediate level of diversity is the sweet spot conducive for economic development. That is why Latin America with lower level of diversity and Africa with higher levels of diversity are less developed than Europe which has intermediate levels of diversity.

Institutions

Institutions and cultural traits were not what triggered development, but rather what determined the speed of it. North and South Korea are a perfect example. They were both dictatorships, but while NK had massive nationalization of private property and centralized decision-making, SK had private property protections and decentralized political and economic power, making inclusive institutions promotive of development and extractive institutions a hindrance to it.

Other example is former British colonies which had common law systems compared to Portuguese and Spanish colonies with civil law systems. Or even South Italy with a feudal order and mafia, characterized by lower prosperity, strong family ties and less trust outside family environments which issued reduced cooperation, opposite to North Italy which was a democracy with higher social mobility.

How are the inequalities Deepened?

We have stated the possible deep-rooted foundations for the inequalities we face nowadays, but what about the causes that emphasise those already existing disparities in qualities of life?

We can adopt a different outlook on this topic, by saying that inequality deepens because of a rapidly changing world. By interacting with a range of factors, including economic systems, political factors, cultural influences, rapid technological change, but also the climate crisis, urbanization and migration, as well as gender, age, origin, ethnicity, disability, sexual orientation, class and religion. Addressing these facts requires a comprehensive understanding of both historical and contemporary factors.

By delving a little bit deeper on some of these topics, we gain a better understanding of how they are undeniably associated with an inevitable distinction between people and their lifestyles.

Technological progress came about as a revolution that became shocking because of its quickness to spread and develop. The unequal access to it can lead to disparities in access to information, skills and economic opportunities. Because of the previously stated deep-rooted causes, some nations are wealthier, disproportionally benefiting new technologies, while poorer communities may lack the resources to adopt them. This may lead to a whole new range of problems, as automatic and digital technologies can displace low-skilled workers, exacerbating unemployment and wage inequality, affecting those vulnerable populations who may, once again, not have the means to transition to these new jobs. Thus, a much larger bridge to connect these nations is imperative.

When we focus on Globalization, we can easily conclude that it has facilitated the flow of goods, services, and capital across borders, undisputably benefiting some economies. That does not exempt the fact that it ultimately marginalized developing countries who may struggle to compete on equal footing with those established markets, leading to uneven economic growth. Also, global supply chain often exploits labour in developing countries, where workers may face low wages accompanied with poor working conditions, which is the case of India, Bangladesh or Kenya, where there is an increasing population of “working poor”. Both poverty and a global workforce at risk of exploitation are socially created circumstances that drive the demand for inexpensive labour, which in turn sustains the profitability of labour-intensive industries. This will perpetuate cycles of poverty and inequality within those regions, as well as wealth concentration in the hands of multinational corporations and affluent individuals, often at the expense of local economies and communities.

Many developing countries rely heavily on the export of a few commodities, leaving them volatile and dependent of commodity price cycles. Price fluctuations can lead to economic instability. When the prices are risen, the benefits often accrue to a small elite or foreign investors rather than being distributed to the broader population. This can exacerbate existing inequalities and impose limits on economic mobility for local communities. Also, some countries that are considered resource-rich experience a so called “resource curse”, that believes that these countries rely exuberantly on those resources, neglecting the other sectors, hindering sustainable and equitable growth.

Figure 1- “resource curse”

Conclusion

In alignment with all that it was tackled, understanding global inequalities requires a comprehensive view that considers both historical contexts and current dynamics, revealing how deep-rooted factors continue to influence disparities in quality of life across the world, and what other factors carry on deepening it.

Sources: “ECCHR: Forced Labor in Global Supply Chains.”; “Causes of Inequality – Equality Trust.”; “Psychological Characteristics and Colonialism: Where the Deep Roots of International Inequalities Were Shaped – the Sustainable Development Watch.”; “The Resource Curse: The Political and Economic Challenges of Natural Resource Wealth”.

A look into the integration and competition concerns of the Draghi Report

“Europe faces a choice between exit, paralysis, or integration” – Mario Draghi

Unlike many of us perceive, European integration is far from figured out.

In practical terms, integration is all-around. From the euro to the European Court of Justice, touching on more simplistic aspects such as the citizen’s identification as Europeans. On the other hand, macro shocks like the Sovereign Debt Crisis might be able unveil more sensitive aspects of this fragile social, economic and political commitment, for example, by leading us to question whether European countries should pay for each other’s debt.

So, how much integration is too much integration? Mario Draghi, former Italian prime minister and president of the European Central Bank (ECB) brings this issue back to the fore with the release of his 400-page report on European competitiveness. There, Draghi identifies a rather plain and apparently sensible solution for its stagnation: cooperation and coordination. The former president of the ECB calls for an additional annual €800bn in investment, paired with a profound policy redesign to foster the European’s assertiveness in global competition. For many, a courageous punch full of truth, while for others, a political disaster.

This article will further delve into the specific intricacies of the mediatic Draghi’s Report, while dissecting the competition dilemma that Europe faces and intertwining them with the pervasive message of integration throughout report. Thus, alluding to the question of whether it exists a trade-off between resilience in global position and the core of current European values.

Nicolas Tucat, AFP

Background

The idea that the European Union is falling behind the United States, China and other advanced economies, when it comes to competitive edge, has been abiding for a while now.

The report dedicates a fair number of pages exploring the evolution of these dynamics. For instance, the gap in GDP level at constant prices is said to be widening, from 15% in 2002 to 30% in 2023. When measured in Purchasing Power Parity (PPP), it amounts to 12%. The gap growth is more sluggish when translated into per capita terms, but the authors claim is still significant, rising from 31% in 2002 to 34% today. The catalyzers for these disparities are precisely differentials in productivity: About 70% of the gap in per capita GDP with US at PPP is explained by lower productivity levels in the EU.

2024, The future of European competitiveness – Part A

On the other hand, the European Union is the proud face of some of the lowest levels of inequality, reportedly disclosing rates of income inequality around 10 percentage points below the ones evidenced in the United States (US) and China. It also surpasses these countries when it comes to life expectancy at birth, low levels of infant mortality, and education. In fact, its education systems allow a third of adults to have completed higher education. The EU is also the world leader in sustainability, environmental standards and progress towards the circular economy. (2024, The future of European competitiveness – Part A).

Plans had already been forged to deal with this issue of modest competition efforts across the European landscape. In November 2023, Ursula von der Leyen delivered her annual State of the Union speech, where she presented the main lines of action for the European Commission for the next year. Von der Leyen dedicated around a third of her speech to reshaping the EU’s economy, but the headline announcement was, precisely, Draghi’s Report. (2023 Foy)

Proposals

The report identified three main areas of action: The first is closing the innovation gap with America. According to the report, emerging technologies are still underdeveloped in the EU, not by lack of ideas or competence, but because of structural blocks, in the form of said inconsistent and restrictive regulations. Europe must focus on easier access for researchers when it comes to the commercialization of ideas, joint public investment in breakthrough technology or even investment in infrastructure to lower the cost of developing AI. Furthermore, training and adult learning should be at the core of the agenda.

The second area for action is combining decarbonization with competitiveness, by reforming Europe’s energy market, so that end-users can benefit from a competitive clean energy price, supporting industries that allow for decarbonization (e.g. clean tech and electric vehicles), while jointly promoting green industries.

The third area is increasing security and reducing dependencies. This vector of action is a result of the political turmoil instituted by the geopolitical instability. The EU is called to build a true “foreign economic policy”, by establishing coordination mechanisms in trade agreements and direct investment, ensuring stock of specific critical goods and devising industrial partnerships to establish robust supply chains.

To add on to this, the article takes a more thorough look at some more specific recommendations that have been particularly featured within the mediatic space, as the ones where it may be more difficult to achieve political consensus towards.

Competition Policy

“There is a question about whether vigorous competition policy conflicts with European companies’ need for sufficient scale to compete with Chinese and American superstar companies” – Draghi’s Report

A controversial point of discussion encompasses the question of competition policy enforcement, particularly mergers. EU antitrust policy has long been praised for protecting against abuses of dominant position. However, the report claims that this might be compromising the forging of European world-beaters, instead of only preserving competition within the EU (2024, Financial Times). In practical terms, this can be translated into the concern that European firms won’t be able to compete with significant global firms.

To achieve this, the report suggests an increased weight of the innovation factor in the assessment of mergers, by allowing higher market share concentration if this were to produce the development of new technologies by the merging firms. Of course, this might raise concerns regarding the misuse of this type of defense on a merger deal, allowing for a situation in which firms might commit to innovation only for the possibility of acquiring increased market power. So, Draghi suggests making companies showcase measurable levels of investment that can be tracked in the years following merger approval. The commission might, for instance, require companies to provide data on pricing or investment.

What is more, it is proposed a less stiff approach towards collaboration between rival corporate executives, with the argument that coordination might be necessary to maximize investment in research, or technological standardization (2024, Foy & Espinoza).

The report also recommends defining telecoms markets at the EU level – as opposed to the Member State level. To exemplify, a merged telecoms group could function in an almost monopolistic setting in individual countries, if their market share across the entire single market was less than 40 percent, which serves as a threshold for merger policy (2024, Foy and Espinoza).

These last measures have been subject to much mediatic scrutiny. On a paper published in Vox EU, the professors Tomaso Duso, Massimo Motta, Martin Peitz and Tommaso Valletti expressed their concerns regarding the telecom policy recommendations provided by the report. They claim that “They propose a broader, EU-wide market definition, which would artificially de-concentrate the relevant market, thereby making intra-national mergers appear no longer problematic on paper”, which ultimately creates the possibility to accept mergers that would be detrimental to European businesses and consumers.

Integration

Draghi claimed that the new “industrial strategy for Europe” would cost approximately €750- €800bn, which corresponds to 4.4-4.7 percent of EU GDP. Large amounts of money should be placed on joint funding key projects, such as innovation, as well as other European “public goods” —such as defense procurement, cross-border grids or common energy infrastructure.

Another concern expressed in the report points to the levels of financial fragmentation of the capital markets of the EU. Its integration is seen as an essential procedure towards the introduction of economic momentum that would allow for the development of the investments needs.

With the case of banking fragmentation, the report reminds us of the incomplete implementation of the Banking Union. While the unified supervision aspect is solidified, Europe has failed to implement a common debt insurance scheme, and the single resolution authority lacks a financial backstop. One of the proposed actions to facilitate this process is the creation of a common safe asset, particularly, the report appeals to “issue common debt instruments to finance joint investment projects that will increase the EU’s competitiveness and security.” However, it also established that a necessary condition for this to happen would be that “the political and institutional conditions are in place”, which can signify an impediment.

Moreover, the report asks for the extension of qualified majority voting (QMV) in the Council of The European Union, such that voting subject to QMV would be elongated to more areas, or even generalized, implying the end, or at least, reduction of the veto power under unanimity voting.

The difficulty here lies exactly in gaining political momentum to implement such reforms. In fact, the German finance minister Christian Lindner has already spoken on the matter, dismissing the Draghi’s suggestion to raise additional common debt to fund breakthrough innovation: “Each individual EU member state must continue to bear responsibility for its own public finances”. (2024 Hall). Eelco Heinen, finance minister of the Netherlands, said that “Europe has to grow, and I totally agree with that. An economy will grow if you reform (…) more money is not always the solution.”.

Conclusion

To conclude, the Draghi Report could represent either a turning point for Europe or just another document to be archived and forgotten about in the years to come. And although it may not be translated into policy action, at least for the time being, it has the power to ignite the public discussion back to “After all, what is the Europe that we want?”

It would be possible to end poverty in the United States, at least in theory. Using a pure means-tested transfer system, the authorities could compensate each individual in the amount remounting the difference between the poverty line value and their income. This would cost only 131 billion dollars, about one-sixth of the value cost of the Social Security program (Using the U.S. Bureau of the Census 2019). The problem is that such computation doesn’t account for the Moral Hazard implications that come with benefit guarantees, as Jonathan Gruber points out in his book Public Finance and Public Policy (2019, Chapter 17).

What happens is that this program may have a way of disincentivizing work to some extent, as it can motivate people slightly above the poverty line to stop working to receive the full benefit without substantially having to lower their consumption. Thus, increasing the number of people receiving the benefits, along with the policy’s costs.

This phenomenon, named Moral Hazard, largely studied by economists, constitutes a change in people’s behavior provoked by the acquisition of insurance, either literally or figuratively speaking. In economics, this event usually leads to inefficient allocations of resources since it induces individuals to have a consumption different from the optimal level. The most common examples of Moral Hazard situations are observed in public policy, such as in the scenario described above, with insurance-related issues, such as health insurance or car insurance, and even during the Great Recession, the topics for the discussion in this article.

Illustration by Christoph Niemann, The New Yorker

Moral Hazard in Public Policy

There are multiple applications of this concept within the realm of insurance in public policy. Unemployment, disability, injury, retirement, and poverty, appear as somewhat unpredictable situations against which agents want to be insured. If one is to think about it, much of the population seeks to smoothen their consumption throughout life. This can be translated into preferring to pay a fixed amount in insurance premiums so as to benefit from compensation in the face of an adverse event, like job loss, in such a way that consumption does not brutally fall.

Here, Moral Hazard usually conveys disincentives to work: Take the example of Unemployment Insurance (UI), that functions as a means of compensating individuals if they lose their jobs. If the payment amounted to 100% of workers’ salaries, people would not have the incentive to seek employment throughout the duration of the benefit, which would ultimately lead to a lower-than-optimal provision of labor in the economy. Additionally, much of the workforce would have an incentive to stop working, adding up to the costs of the program. This is why not only UI but also schemes that cover these and other types of adverse events often do not contemplate full insurance. Instead, they try to weigh out the consumption smoothing ability that the program carries with its Moral Hazard costs.

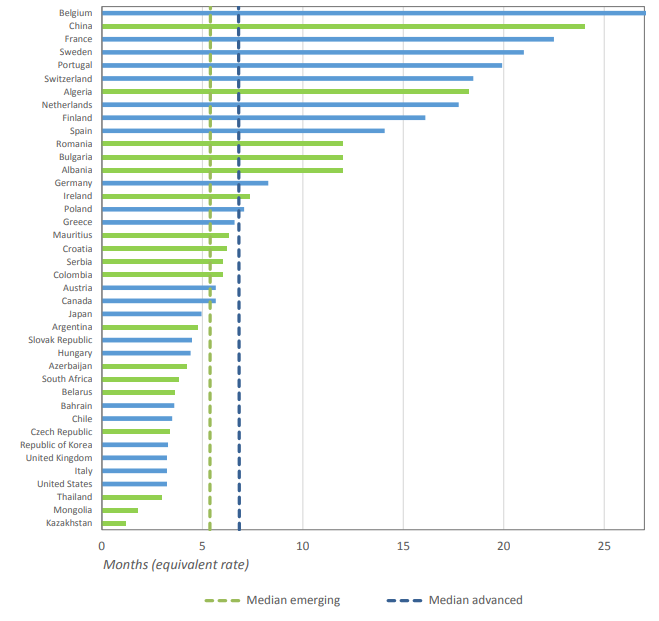

Countries may choose different schemes of Unemployment Benefits, depending on their internal policies. According to the Figure, it can be pointed out that the United States provides one of the lowest financial disincentives to return to work and constitutes one of the countries with a lower maximum amount for the duration of the benefits program (Figure 2). On the other hand, in most European countries the disincentive is more substantial and the threshold for the benefits is higher.

Fig.1 – Financial disincentive to return to work (2023, OECD Data)

Fig. 2 – Maximum duration of unemployment benefits at an equivalent rate (2019, ILO)

Moral Hazard in Health Insurance

Once again, insurance (in the health case) promotes consumption smoothing when faced with an adverse event (sickness). Its importance relates to the fact that it facilitates necessary treatments without the injured having to carry out major payments.

Yet, another common means for Moral Hazard to manifest itself is through health insurance, which can comprise two types: Ex ante and ex post Moral Hazard. The first one illustrates cases where individuals have less incentive to indulge in activities that reduce the risk of sickness or illness (e.g. smoking), when insured, whereas the last comprises a circumstance in which insurance beneficiaries are less likely to limit the use of healthcare when sick (e.g. going to consultation because of a cold).

When provided with health coverage, individuals may be more prone to seek medical care for minor conditions or undergo unnecessary procedures. This overutilization can strain healthcare resources, and lead to inefficiencies in the delivery of care. Additionally, it can drive up costs for insurers, leading to greater insurance premiums.

However, would it be unreasonable to assume this increase in healthcare utilization can come from the actual need for medical care?

“Too Big to Fail”: Moral Hazard in the Great Recession

Moral Hazard is not only present in the daily life of the average person but also in the most pressing global financial crises. The most prominent example being the 2008 Financial Crisis. In the years leading up to this crisis, the United States had evidenced an exponential increase in housing prices, stemming from factors such as the accessibility of credit, lower interest rates, and permissive lending standards. This allowed a significant number of subprime borrowers to obtain mortgages, bundled by Financial Institutions to form Mortgage-Backed Securities (MBS) and Collateralized Debt Obligations (CDO) which were posteriorly sold to international investors with higher credit ratings.

Why did Financial Institutions engage in such risky lending practices?

Credit rating agencies played an instrumental role in the crisis by assigning high ratings to MBS and CDO, prompting a false sense of security about the degree of risk of these securities. This is where Moral Hazard comes in, as the financial institutions involved operated in accordance with the misbelief that they were “too big to fail” (Stewart McKinney, 1984). This entailed the expectation that, because of financial institutions’ vitality to the economy, regulating authorities would not allow them to fail due to the systemic risk that could influence the course of the global environment. Thus, these continued to operate with disregard for possible unfavorable outcomes so, when housing prices peaked and proceeded to decline in 2006, borrowers defaulted on their mortgages, leading to a collapse in the value of MBS.

The losses caused a domino effect in the financial sector and major financial institutions faced bankruptcy, with long-lasting effects on the global economy prompting a significant need for regulatory reforms. One measure was the Dodd-Frank Wall Street Reform which implicates more strenuous capital and liquidity requirements for banks with at least $50 billion in assets, and the Consumer Protection Act in the US to further protect financial activity in the country. Its provisions included the Volcker Rule, which argues that banks that take on hazardous risks should not be government-subsidized and aims at constraining banks from using their own money to trade securities, rather than depositor money. The latter faced opposition as many of the institutions that integrated this failure did not take on deposits and would not have been subject to such rules.

So, are authorities able to contain Moral Hazards?

Silicon Valley Bank (SVB), a bank with assets totaling $209 billion in late 2022, according to the Federal Deposit Insurance Corporation, collapsed one week after being listed on Forbes’ America’s Best Banks List, making the sour transition from one of the best American banks, into the second-largest bank failure in US history.

This unfortunate occurrence sprang from the large amount of deposits with scarce cash held by the bank, with which SVB would buy treasury bonds and other long-term debts that have low returns and risk. However, as the Federal Reserve increased interest rates to combat inflation, SVB’s bonds became riskier and, thus, saw a stark decline in value which prompted mass customers to withdraw funds, leading to its collapse.

It is also argued that this failure started before the Federal Reserve’s regulations, with the overturn of the Dodd-Frank Act whose requirements were relived in 2018 by former President Donald Trump. This was done through the Economic Growth Regulatory Relief, and Consumer Protection Act, according to which the law increased the threshold to $250 billion. Thus, another instance of moral hazard lies with the bailout provided to SVB, raising concerns regarding other banks’ propensity to take risks. It is, therefore, of great importance to acknowledge the dichotomy faced by the Federal Reserve when weighing price stability and financial stability, since interest rates, despite being conventionally perceived as a powerful strategy to stabilize inflation, can rapidly escalate to become a trigger for Moral Hazards within the financial sector, rooting global financial instability.

Policy implications

Evidently, public policy applications of Moral Hazard come with implications. Many economists focus their work on the design of these. With the UI, policymakers try to balance the consumption smoothing benefits of the insurance with its Moral Hazard costs, which depend on the magnitude and predictability of adverse events. For example, retirement is a rather predictable event, so people may prepare in advance. On the other hand, unemployment is considered of low magnitude, meaning that some may be able to self-insure. The functioning of both Disability Insurance (DI) and Workers’ Compensation (WC) goes along those lines, which ultimately impedes these programs from offering full coverage.

Poverty alleviation programs, as mentioned in the introduction, also carry Moral Hazard concerns. In such a case, there are policies designed to try to make sure that everyone who needs the benefit gets it and those who do not don’t, although this might be difficult. There are some instruments impregnated in society to try to regulate this, such as ordeal mechanisms, that make welfare programs somewhat unattractive to guarantee that only the population that necessitates benefits from them. For example, the long lines in soup kitchens.

In 2010, President Barack Obama signed the Patient Protection and Affordable Care Act, often referred to as the Affordable Care Act (ACA) or Obamacare. This legislation aimed to extend health coverage to millions of uninsured Americans by expanding Medicaid, establishing health insurance exchanges, and introducing various health-related provisions. The ACA sought to make health insurance more accessible and affordable. It offered premium tax credits and cost-sharing reductions to individuals with lower incomes. However, the Act may also have exacerbated existing moral hazards within the health insurance industry, as Sean Ross discusses in his article (2023). Some of the provisions included the mandatory coverage of some essential benefits, the obligation to buy insurance, provided with an exemption for low-income citizens, and restricting prices. However, in such a scenario, one should also consider the fairness argument for the existence of programs that lower the efficiency of an economy. At the end of the day, it is a trade-off.

Illustration by Andrew Grossman, IAS

Conclusion

From work disincentives to devastating financial crises, moral hazards’ ever presence within a country’s economy underscores the intricacy in policy making towards a balance between social welfare and economic efficiency. While initiatives such as healthcare or social benefits aim to mitigate disparities, moral hazard reminds governments of the complexity implicit in policymaking and surfaces the question introduced in this article: To moral hazard or not to moral hazard?

References

Aklin, Michaël, and Andreas Kern. 2019. “Moral Hazard and Financial Crises: Evidence From American Troop Deployments.” International Studies Quarterly (Print) 63 (1): 15-29. https://academic.oup.com/isq/article/63/1/15/5290056

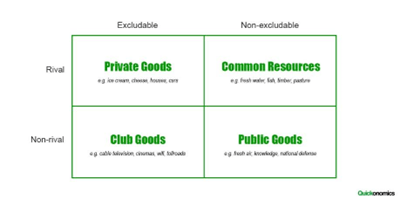

The four categories of goods, given their degree of excludability and rivalry

Definition “rivalrous and non-excludable goods”. Big words. And what do they mean, exactly? Well, let’s break it down. First, excludability: an excludable good is a good/resource that someone can bar (or limit the access to) other people from using. Second, rivalry. Despite the name, rivalrous goods are not the ones that lose their temper when their football team is losing. Rivalry simply means that if one person uses the good, someone else will either have less of the good to use or be unable to use it at all. Think of the shirt you are (presumably) wearing now: while you wear it, no one else can. Music, for example, is just the opposite – if someone is listening to a song, there won’t be any less of the same song for others to hear (unfortunately, in some cases). With these 2 characteristics, we divide goods into 4 categories: private goods, the excludable and rivalrous ones; club goods, excludable but non-rivalrous; public goods, neither excludable nor rivalrous; and the ones we will be focusing on, the non-excludable and rivalrous goods, the commons.

So, common goods are the ones that everyone has access to (or at least it would be hard to block anyone from using them), while also being diminished with every utilization, that is, there is progressively less quantity available the more they are used. Now, you may recognize this description as the one of most natural resources: fish in the sea, mineral deposits, the shells at the beach…Consequently, it is easy to see the problem that arises from these characteristics: their sustainability.

THE TRAGEDY

The Tragedy of the Commons. Despite the rather theatrical name, it is neither a Shakespearean play nor a Mexican soap opera (we’ve checked).

This Tragedy is an economic term coined in 1968 by Garrett Hardin to describe the phenomenon of over-exploitation of common-pool resources: users of the common good behave opportunistically, seeing the resource as “free”, since they cannot be excluded from it, so they reap all the benefits without taking in the costs, which ultimately leads to depletion.

The extinct dodo

We do seem to have a tendency to explore every resource we can until thorough extinction (I mean, when was the last time you saw a dodo around?), with no regard for their long-term (or even short-term) sustainability. The rationale is rather simple: if it belongs to everyone, it belongs to no one, so you should be quick to grab as much as you can before it’s over.

The problem with this is, as we’ve seen, the risk of depletion. And this is not merely childish or selfish behavior. This is, in fact, very standard rational economic behavior. Every user can be immediately better-off by taking more than what is sustainable to take, so they do it, until inevitably the resource is gone. Individuals have no direct incentive to behave sustainably. Sustainability is often in the best interest of a community, but not necessarily of a single person. See the problem?

NEED A SOLUTION? ELIMINATE THE PROBLEM

This is the standard economics’ layout of the issue – and standard economics presents a solution. Think of a small forest, of around 30 trees, and 3 lumberjacks. Every year, in the spring, the lumberjacks come and take down trees to sell the wood. Now, the forest is capable of regenerating: if they leave at least 3 trees standing, next year 30 will be there again (it’s a very mathematically exact forest). What would be optimal? Easy, right? Each lumberjack could take down 9 trees, and all could come back next spring to get more. But each one has an incentive to outperform the others, sell a lot of wood and get rich. So, each takes as many trees as they can, leaving none in the forest. How can we prevent this?

The forest and lumberjacks’ metaphor

Whatever we do, the good will not magically become non-rivalrous, but we can do our best to make it excludable. In other words, if the problem arises from collective ownership of the resource, then the solution is surely to change that ownership form. One way to do this is to effectively switch ownership to the government, who then regulates who has access and how much of the resource can be consumed. In our magic forest example, this would mean passing a law stating that each lumberjack could take no more than 9 trees every year.

It should be noted that this solution requires some form of enforcement – a surveillance authority to ensure regulations are upheld, as well as a penalty in case of breach of the system. These are usually provided, or at least legitimized, by the same governmental authority that controls the resource.

Such top-down, centralized solutions suffer from certain inherent problems, namely rent-seeking (one entity trying to gain some profit without further contributing to the productivity of the system – like governmental officials trying to collect bribes from the citizens to grant them access to the resource), principal-agent conflicts (when there is a conflict of interest between the citizens and the agent meant to act in their behalf, like the government representative) and knowledge issues (the government may not be fully accurately aware of the needs of the population).

If state control is not the ideal answer, then maybe we should go in the opposite direction: privatization. Maybe each person could be given a part of the resource to explore (say, each lumberjack is given a certain amount of trees), and trade between themselves, so that each gets the best deal they can potentially obtain.

If state ownership is not the solution, how about privatization?

Unfortunately, this is not a perfect solution either. Besides the physical impracticability of dividing up some of these goods, there is again the issue of enforceability. Besides, this solution comes with a problem at the very beginning: each person is given a part of the resource to exploit – but… given by whom? Often enough, such a project of privatization requires a government taking control of the resource and then assigning its exploration as it sees fit. So, at its very core, this solution is not so different from the first. Both rely on a higher authority defining and enforcing regulations to limit the use of the common good. They follow a very simple logic: if commons are so tragically doomed, then our efforts should focus on tackling their core characteristics, what makes them common goods in the first place.

So far, we have looked at the problem and formulated solutions assuming this is how individuals act when faced with a resource to share. But do we always have the behavioral standards of a preschooler? Thankfully, no. In fact (poor dodos aside), we are actually very capable of collectively managing common resources.

OSTROM’S THEORY

In 2008, economist Elinor Ostrom was awarded the Nobel Prize in Economic Sciences (becoming the first woman to receive it). The reason? Her breakthrough research on common-pool resource management.

Elinor Ostrom

Ostrom took a different approach to the problem. Hardin had looked at common goods and their rivalrous and non-excludable nature and tried to explain their over-exploitation based on standard economic theory’s behavior predictions: people behave selfishly and without considering others or the future; therefore, the Tragedy is only natural. Ostrom, on the other hand, decided to start from observation, not from assumptions. And what did she discover? Examples, many in fact, of sustainable management of a common-pool resource! This real-life examination allowed her to arrive at a new theory. In all these successful cases, the management was done by the local communities! Yes, the solution was right there in the name all along.

So, all we need to do is to leave common goods alone, trusting local communities to handle the matter? Great! Economics is so easy (…said any economics freshman right before their first midterm season…). The theory is, of course, slightly more elaborated.

Ostrom laid down a set of conditions under which local community management – what she called management through collective action – of common resources can be optimal:

Define clear boundaries of the common resource

Rules governing the use of common resources should fit local needs and conditions

As many users of the resource as possible should participate in making decisions regarding usage

Usage of common resources must be monitored

Sanctions for violators of the defined rules should be graduated

Conflicts should be resolved easily and informally

Higher-level authorities recognize the established rules and self-governance of resource users

Common resource management should consider regional resource management

Let’s think of what this looks like in the previous 30-trees-for-3-lumberjacks example:

First, the community should clearly set down who the resource is meant for. By community, we mean the people who live and work within the ecosystem the forest in inserted in – a village where the lumberjacks live, the market they trade on. The group allowed to explore the resource is the lumberjack professionals – they are the ones who make their livelihoods from the forest. It should also be clarified how much of the resource can be taken, and the lumberjacks should take part in the rule making. The people in the village know better than anyone how the forest works: they know at least 3 trees must be left for the forest to regenerate, and have an interest in its sustainability, and the lumberjacks want to reap the benefits of its exploration. Besides, people are more likely to comply with rules they helped write themselves. Of course, the forest must be monitored, and if someone takes more than their share they must be punished by the community. But this punishment should be gradual – not immediately banning, but warning, sanctioning and informal social condemnation (the offender should feel ashamed to break the rules). If there is any disagreement regarding the forest, it should be able to be resolved quickly, in an informal way. The community should also feel assured that their rules will not be overturned by a higher authority. Lastly, they should remember that the forest does not stand alone. It is part of a larger system that should be had in mind, so that resources are explored in a way that does not hurt the rest of the system.

CONCLUSION

Common-pool resources management is a puzzling subject. They can be invaluable tools for the subsistence and development of local communities, or they can be consumed to extinction in a heartbeat. Ostrom’s Co-operative Collective Action Management Theory is a clever and helpful way to think about sustainability, one of the greatest challenges of our century. Her work proves observation and context are important tools for economic research, perhaps the most important ones.

Sources:Investopedia, Wikipedia, Harvard Business School, American Enterprise Institute, Aeon, Corporate Finance Institute

The People’s Republic of China, with its 1.4 billion population, is the most populous nation on earth, boasting the 2ndhighest economy in nominal terms. Being considered one of the largest economic miracles in recent history, – with sustained growth levels above 5% since 1990 up until 2020 – millions of Chinese people have been lifted out of poverty following the country’s embrace of international trade and investment. Nevertheless, ever since the beginning of the COVID outbreaks, China has struggled to maintain its historic impressive figures. While its zero Covid policy has certainly pressed the brakes on economic activity, through mandatory lockdowns and business shutdowns, a series of deeper and more serious problems – from a faulting real estate market to government overspending – have recently started to showcase the cracks on the country´s economy.

A brief recent history of China’s economy

For a large part of recent history, particularly between the 14th and 18th century, China is believed to have been responsible for one of the largest shares of economic activity worldwide. While it experienced a heavy economic decline in the subsequent period, it was during the 1970s that its share on global output began to rise once again. Following the end of the Chinese Cultural Revolution, the Four Modernizations were adopted to kick start the nation´s production sectors, with a special focus on agriculture, industry, defense, and science. This program heavily moved away from the “iron rice bowl”, or “work for life”, previously in place, and embraced a meritocratic system where workers and managers were rewarded if they hit or exceeded their targets.

In the 1980s, China implemented Special Economic Zones in its southeastern region, creating pockets free to trade internationally and receive direct foreign investment without Beijing’s direct control, in a bid to increase productivity and prosperity. Fast forward to 2001 and the World Trade Organization welcomed China as its newest member, allowing the nation to access the world’s markets and more favorable rates, marking it one of the most consequential events of the 21st century. The country has since become responsible for almost one third of manufacturing output, surpassing Japan in 2010 to become the 2nd largest economy, and is now home to 12 of the 100 largest firms by market capitalization, more than any country apart from the United States.

Economic Troubles: The Real Estate indebtedness