In general, there are many pros and cons to the creation of a monetary union. The creation of a single currency among many countries allows for the lowering of cross-country transaction costs, increases certainty for investment while, because of this, stimulating trade and job creation. On the other hand, it means that the union’s monetary authority has the responsibility of implementing a “one size fits all” monetary policy, which may create problems if the members of the monetary union have very different economies or if the shocks which monetary policy is meant to address occur asymmetrically across countries.

The creation of the Euro

An Economic and Monetary Union has been an objective of the European Union from as early on as the late ’60s/early 70s, with the first steps towards the coordination of the member states´ monetary policies having been taken with the launch of the EMS (European Monetary System) in 1979. However, it wasn´t until a decade later that the idea of a single currency union really started to take shape, upon the presentation in the “Delors Report” of a three-stage plan to be applied in the ’90s to prepare the union for what would come to be known as the euro area, ultimately culminating in the creation of a single currency and the European Central Bank.

The idea of a common currency first and foremost appeared as an important symbol of political and social integration in Europe, tied with the notion that an increased integration of the European member states would reduce the risk of war and crisis on the continent. Then, on an economic viewpoint, a common monetary policy centered around price stability was viewed as an important propulsor of economic stability. Likewise, those who supported the creation of the euro believed it would allow for an increase in market integration, consequently reducing transportation costs and improving market efficiency and price transparency.

In 1991, the Maastricht Treaty effectively cemented the transformation of the European Community into a full Economic and Monetary Union, laying down the rules for qualification for membership of the Monetary Union. Indeed, a set of macroeconomic criteria that member states had to respect to be able to participate in the EMU and adopt what would be the new common currency (the euro) was defined. These became commonly known as the four convergence criteria, focusing on price stability, public finances, exchange-rate stability, and long-term interest rates. In terms of price stability, a member state´s inflation rate (measured by the HCPI) should not exceed more than 1.5% of the best three performing member states. As for public finances, to ensure that they are sustainable, government deficit should not surpass 3% of the GDP and public debt should be below 60% of the GDP (although some accommodation here was made at the time of the start of the Union, as many member states did not fulfil these specific public finance requirements). Moreover, regarding long-term interest rates, to guarantee the durability of the convergence, they must not be more than 2 percentage points above that of the three member states with the lowest interest rates. Finally, when it comes to ensuring exchange-rate stability, applicants to the common union should have been participating in the ERM II (Exchange Rate Mechanism) for at least two years prior to the adoption of the common currency without severely devaluing against the euro.

The need for this set of requirements to be put in place prior to the entrance into the monetary union came as a necessary part of subjecting such a wide range of countries – still very much asymmetrical in some regards – to a single monetary policy but allowing them to keep their national fiscal policies. Indeed, some countries with better performing public finances and benefiting from low interest rates (such as Germany) expressed their concerns of how being associated with other not as well performing countries could negatively impact their economy, hence their pressure for a system of rules to be establish so as to guarantee as much as possible convergence among the member states. This type of concern is also reflected in the way much of EU´s monetary policy is designed, particularly in their rigidity and zealous focus on price stability, as is greatly patented in the way the European Central Bank was created in 1998 very much influenced by the German model, mirroring their Bundesbank.

Ultimately, the euro was officially launched on January 1st, 1999, with the exchange rates of the participating currencies being irrevocably fixed, replacing its precursor (the “ecu”, a transitory currency composed of a basket of European currencies to serve as a basis for fixing the exchange rates of the member states) at 1:1 value. In this initial phase the euro only served in the form of cashless payments, having been put effectively in circulation in 2002.

The beginning of the Monetary Union and the Financial Crisis

The process of increasing openness of financial markets alongside the adoption of the Euro’s convergence criteria by countries wishing to join the monetary union meant that during the 1990s there was a convergence of interest rates across countries, with some countries like Portugal, Greece and Italy enjoying interest rates much lower than before.

During the early 2000’s, thanks in part to the abundant credit and to the advances in economic openness, some countries (such as Portugal, Greece, and Italy) began accumulating large current account deficits. These may simply be the sign of a healthy economy, if they are being used to finance future growth so that, later, the current account deficit can be matched by a current account surplus. However, if this is not the case, then current account deficits will accumulate, increasing a country’s external debt until, at some point, external credit stops being granted. While they were accumulating large stocks of external debt, some of these countries were also amassing very significant amounts of public debt.

In 2008, as the financial crisis began, and its contagion spread across financial markets there was a global flight to safety. Because of this, Portugal, Spain, Greece, Italy, and Ireland, which, to differing extents, fell into the trends described above, began facing international credit crunches and the yields on their sovereign bonds began increasing, with Portugal and Greece being the most affected. This sovereign debt crisis then led to troubles in the banking sectors of these countries which can then worsen the sovereign debt crisis, creating the “Doom Loop”.

The Greek banking and debt crisis was challenging and, in 2012, the possibility of a default was looming. Certain actions, like currency devaluation to decrease current account deficits or drastic increases in liquidity to Greek banks to avoid the banking system from grinding to a halt, were not available to Greece, since monetary policy was delegated to the ECB. Because of the deteriorating situation and due to the possibility of Greece exiting the Euro, the ECB decided to do “whatever it takes” to save the Euro and announced a program for purchasing debt of the distressed countries on the secondary markets, reassuring markets and bringing down the debt spreads, and, potentially, saving the Euro.

Who to favor?

The ECB mandate has one and clear focus, price stability. To ensure so, the central bank applies all the tools that it has available. However, the effects from such tools impact multiple variables which have important macro-economic consequences for Eurozone countries, such as FX rates or credit spreads. This, coupled with an asymmetric impact on the moves of these variables for different countries creates a huge dilemma for the policy makers behind ECB’s decisions: Who to favor?

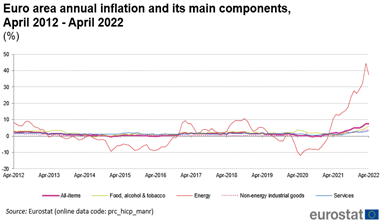

Does the question sound simple to you? Let’s think of today’s scenario for policy makers at the ECB. In Europe we are experiencing broad record inflation, way above the defined target for price stability, meanwhile credit spreads are already very high compared to historical values, mainly for peripherals countries, and the Euro FX is at some of its lowest levels, especially against the dollar. Should the central bank tighten financial conditions to fight inflation and strengthen the Euro but, at the same time, risking a default/crisis in peripherals countries? Or should it do the exact opposite?

What would you do, who do you favor?

Source: Borsa Italiana

Source: Eurostat

Conclusion

The introduction of the euro brought many benefits for the countries involved but it is still a long way from its counterparty in the United States of America. These problems arise mainly due to the structural differences between all the economies in the Eurozone. The “one size fits all” is still one of the biggest challenges going forward with some steps already made into solving it.

Sources: European Commission

Diogo Almeida

João Baptista

Sara Robalo

Inês Lindoso

João Correia