The People’s Republic of China, with its 1.4 billion population, is the most populous nation on earth, boasting the 2ndhighest economy in nominal terms. Being considered one of the largest economic miracles in recent history, – with sustained growth levels above 5% since 1990 up until 2020 – millions of Chinese people have been lifted out of poverty following the country’s embrace of international trade and investment. Nevertheless, ever since the beginning of the COVID outbreaks, China has struggled to maintain its historic impressive figures. While its zero Covid policy has certainly pressed the brakes on economic activity, through mandatory lockdowns and business shutdowns, a series of deeper and more serious problems – from a faulting real estate market to government overspending – have recently started to showcase the cracks on the country´s economy.

A brief recent history of China’s economy

For a large part of recent history, particularly between the 14th and 18th century, China is believed to have been responsible for one of the largest shares of economic activity worldwide. While it experienced a heavy economic decline in the subsequent period, it was during the 1970s that its share on global output began to rise once again. Following the end of the Chinese Cultural Revolution, the Four Modernizations were adopted to kick start the nation´s production sectors, with a special focus on agriculture, industry, defense, and science. This program heavily moved away from the “iron rice bowl”, or “work for life”, previously in place, and embraced a meritocratic system where workers and managers were rewarded if they hit or exceeded their targets.

In the 1980s, China implemented Special Economic Zones in its southeastern region, creating pockets free to trade internationally and receive direct foreign investment without Beijing’s direct control, in a bid to increase productivity and prosperity. Fast forward to 2001 and the World Trade Organization welcomed China as its newest member, allowing the nation to access the world’s markets and more favorable rates, marking it one of the most consequential events of the 21st century. The country has since become responsible for almost one third of manufacturing output, surpassing Japan in 2010 to become the 2nd largest economy, and is now home to 12 of the 100 largest firms by market capitalization, more than any country apart from the United States.

Economic Troubles: The Real Estate indebtedness

China, unlike the vast majority of the developed world, imposes restrictions on capital outflows. Coupled with a very volatile stock market, Chinese consumers tend to favor housing as the main form of investment, visible by its high ownership rates (around 90% compared to the US’s 65%) and the increasing purchase of 2nd and 3rd homes. Home ownership also seems to be a consequence of China’s demographic imbalance, with men vastly outnumbering women, as it seemingly becomes a pre-requisite for marriage. This leaves the country heavily vulnerable to this market, with some estimating that it is responsible for as much as 30% of the GDP when accounting to related activities. In addition, as China’s population begins to decline, the increase in prices that supports this investment can only go on for so long.

The year of 2008 marked one of the worst financial crises on record, shooting the world’s collective output growth into negative territory for the first time in at least 50 years. This tumble, however, did not seem to reach China as its output still recorded an impressive growth rate of 9%, due, in no small part, to the introduction of a massive stimulus package keeping interest rates low and borrowing cheap. This allowed companies like Evergrande – the largest (by sales) real estate developer in China as of 2016 – to use its lands as collateral to borrow money, to then be used to acquire more land (and so on), which, while allowing for massive growth, meant that debt levels also grew. With growing levels of non-financial debt by 2020, and with the goal of mitigating the risk, the Communist Party introduced the “three red lines” aimed at limiting the ease with which developers could accumulate debt. Going back to Evergrande´s case, while it announced plans to reduce its debt, issues resurfaced in 2021. With 1,5 million homes partially paid for, and an estimated 300 billion US dollars in liabilities, homebuyers began to protest in Guangzhou in a showing of the climbing proportion of these difficulties, and the company finally defaulted in December of 2021. With other major property developers having defaulted as well, namely HNA and Sunac, the sector is at risk of severely fragilizing one of the world’s largest economies.

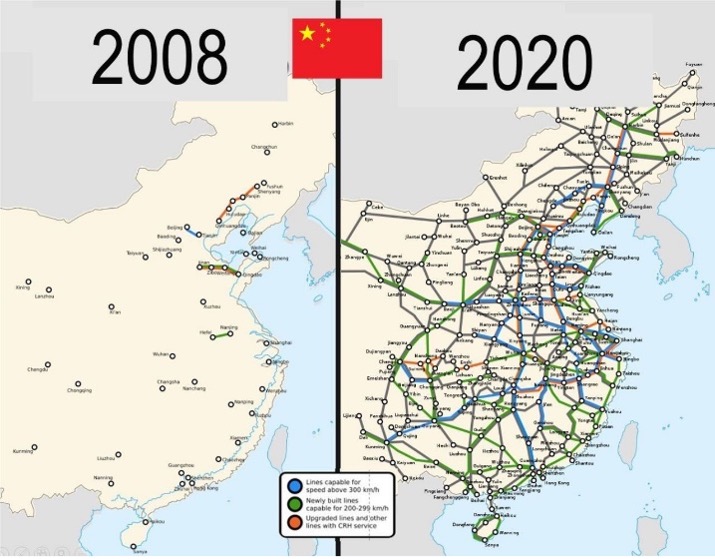

Economic Troubles: The Railway headache

The massive fiscal stimulus of 2008 was not restricted to the real estate sector. In fact, to keep the economy going, China embarked on heavy infrastructure spending, of which the railway was a big part. Infrastructure spending is one of the most efficient ways to boost an economy; not only does it employ a large number of people, but it produces something that continues to offer value long before the project is concluded. Notwithstanding, this railway investment soon began to give the nation headaches. Not only was it plagued with corruption accusations, but by not technically being managed by the government but by public companies that could more easily borrow capital, a construction spree gave way to a bigger problem. As the most profitable lines between the largest populational centers had been constructed, the growth of the system was based on connecting smaller cities further apart, meaning profit was harder to come by. The troubles began to intensify in 2015 when operating profits didn’t even cover interest payments and have since worsened. As tracks began to age, requiring more frequent maintenance, and with ticket prices rigidity blocking a revenue increase, the issues began to pile up. Ultimately, COVID dealt the final blow, plummeting ridership numbers and effectively making every line unprofitable, leaving a system with estimated levels of debt close to a trillion dollars.

Caveats and final thoughts

China has been recently facing a large number of economic headwinds, from a potential housing market collapse and overspending on infrastructure to more recent extensive lockdowns, trade wars, heat waves and floods. But to answer the question raised – “Is the country heading for a collapse?” – most probably not. Economies naturally go through booms and busts, and the latter, while painful, offer a way to remove the least efficient and productive elements in the market, and in the case of China, a chance to move away towards more sustainable sectors such as tourism or R&D. Furthermore, with a tight grip on the economy and the largest pile of foreign reserves of any country, China has a cushion against any possible bank runs and the ability to guarantee currency stability. The country has, for now, also dodged the climbing inflation levels seen in much of the rest of the world, and the central bank has even lowered interest rates. With the mentioned problems being addressed, and some more, including the lockdowns and environment irregularities set to dissipate in the short to medium run, China may no longer be able to support the huge growth levels it once did, but its economy is surely far from collapsing, with continuous stability and development guaranteeing its position as one of the largest and most robust on earth.

Sources: World Bank, Trading Economics, Business Insider, Oxford, Boden, Statista, Bloomber, Market Cap, Financial Times, Reuters, New York Times, CNBC, Eurasian Times, FRED

Manuel Rocha