Imposto Mortágua (Portuguese for Mortágua Tax) is a type of property tax that was implemented in Portugal in 2017. Its formal denomination is AIMI, Adicional ao Imposto Municipal sobre Imóveis (Portuguese for Additional Property Tax). It gained popularity as Imposto Mortágua, due to the Portuguese congresswoman and economist who created this tax, named Mariana Mortágua. As such, what is this tax about?

In short, this is an additional tax to the common Portuguese property tax IMI (Imposto Municipal sobre Imóveis) in Portugal. It is only imposed on individuals and corporations with luxury properties – which can vary from urban housing buildings to construction fields. However, regarding corporations, this tax only considers property that is not being used for production, while households’ property used directly for housing is not accounted nor taxed too. Furthermore, all revenue collected from this tax is directly allocated to the Portuguese Social Security.

More specifically, AIMI is only imposed on citizens that own property whose tax equity value is above a certain threshold, this being 600,000 € in 2019 for non-married individuals and 1,200,000 € for married individuals benefiting from joint taxation. Moreover, this tax is progressive and, therefore, divided in three brackets, with tax rates ranging from 0,7% to 1,5%, coming from the less valuable properties to the more expensive ones, respectively. This information regards the year of 2019, and a more visual and detailed representation of this tax methodology can be seen in the figures below.

Figure 1 – Tax brackets and absolute amounts imposed on singular, non-married individuals, owning properties valued at that respective amount. The values on the left column show the possible Valor Patrimonial Tributário (Portuguese for Tax Equity Value) of a property (as one can see, properties valued at bellow than 600 000 € are not taxed), the values on the middle column show the marginal tax rate for each property value and the values on the right column show the absolute amount an individual has to pay, marginally.

Source: Banco Montepio

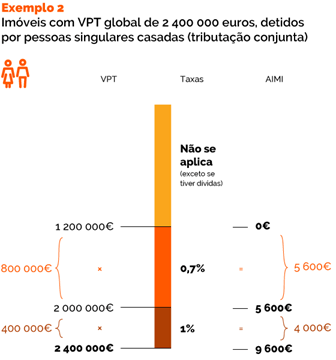

Figure 2 – Tax brackets and absolute amounts imposed on properties owned by married individuals with joint taxation.

The interpretation for this is equivalent to the one in Figure 1, except that the tax only applies to properties valued at more than 1 200 000 € owned by married individuals with joint taxation.

Source: Banco Montepio

It is also important to state that these tax rates, since they are marginal, are therefore imposed on the difference between the next threshold value and the extra income above the previous threshold/bracket. For example, on a singular household with a property valued at 1,100,000 €, the following taxation will be imposed: for the first 600,000 €0.7% will be deducted from 400 000 (i.e. 1,000,000 € – 600,000 €), and then on the extra 500 000 €, a marginal tax rate of 1% will be imposed on the 100 000 € (i.e. 1,200,000 – 1,100,000 €),. As such, the absolute amount paid by this household on a 1,100,000 € property will be:

(400,000 € * 0.7%) + (100,000 € * 1%) = 2,800 € + 1,000 € = 3,800 €.

This tax created an interesting phenomenon – it is highly disliked by the Portuguese population, despite the fact that the vast majority of the people not supporting it are not affected at all by the tax itself (indeed, less than 1% of all Portuguese taxpayers are obligated to pay AIMI).

As such, one might ask: but why? Is it a problem of just misinformation of the population about the tax methodology or are there more complex political economy behaviours underlying such phenomenon?

Evidence shows that taxes on wealth (such as AIMI) are known to combat inequality in a very effective way. Indeed, wealth inequality shows a much larger gap compared to income inequality. Therefore, if an economist/politician has as main priority the reduction of inequality, a wealth tax might be the way to go since it tackles the main problem of wealth inequality directly.

AIMI is a great example of this, since taxing property is one of the most effective ways to tax wealth – not only it taxes directly the rich, who might have large inheritances and wealth stocks that are generating no flow to the economy, nor contributing to economic growth in any way, but it is also very difficult (if even impossible) to deviate from this tax, since property cannot be moved. This means that the likelihood that this tax generates a reflexive outcome is very narrow.

As such, it is also important to clarify that wealth taxes are levied on the wealth stock (therefore, the total amount of net wealth a taxpayer owns), while an income tax is imposed on the flow from the wealth stock. The income earned from returns to wealth becomes part of the wealth tax base for the next year, as the wealth stock grows.

This might very well be the reason why people dislike Imposto Mortágua – they feel as though they are being double-taxed. Indeed, wealth is a stock generated by the accumulation of income flows throughout one’s life (and also possible inheritances generated from income flows of past generations) and such income flows have been, for the most part, heavily taxed by income taxes. Accordingly, many people disagree with the policy of taxing wealth, since they view it as though such wealth has been taxed already through the taxation of income flows that ultimately generated such wealth. Considering AIMI specifically, this reasoning may widely apply too. People might view their properties as an accumulation of the income they generated throughout life, that was taxed accordingly and, therefore, they believe that owning such properties should not be upon the obligation of paying an added tax.

Thus, coming back to the initial question of why AIMI was so disliked when created, one might believe the answer to be a combination of the following reasons – not only because of a general dislike for wealth taxes, as many people view it as being unfair, but also due to misinformation about the respective tax methodology, thus believing AIMI would apply to any individual owning any kind of property or land (which is not the case).

As such, one might question what are the motivations to apply such tax as Imposto Mortágua in Portugal. The answer relates to the trade-off the government makes between efficiency and equity considerations, being this a purely normative discussion and, therefore, harder to reach fair conclusions.

For every public policy the government makes, a trade-off must be done between the effect on market efficiency and the effect on income and wealth inequality that such policy would make. How to compute the optimal trade-off is a hard task to ask and one can even say it depends more on politics rather than economic reasoning. The creation of AIMI is, therefore, a policy that prioritizes the latter – its ultimate goal is to reduce wealth inequality in Portugal – but, as one can see, it comes with some consequential hurdles. Nevertheless, in 2019, this tax generated revenues of 151,560,000 €, which were around 8,52% of the state’s tax revenue. This might benefit the activity of Social Security, which could ultimately help lower classes by giving them the needed resources and, therefore, reduce inequality.

Concluding, morally speaking, it is very ambiguous to objectively state whether this public policy is good or bad for the country, since it mainly depends on one’s motivations. When creating Imposto Mortágua, the government considered the economic impacts and may have disregarded eventual discontents among the population. Nevertheless, the government believes its economic outcomes show a clear positive social impact for many citizens. But, as seen above, people’s expectations, motivations, and consequent behaviours are highly heterogeneous.

Sources: Banco Montepio, Economia ao Minuto, Esquerda.net, Idealista, Portal das Finanças, Tax Foundation, ZAP Notícias