In November 2020, LVMH announced it reached an agreement to acquire the US Jeweler Tiffany & Co for a record breaking $16,2 B. Almost a year has passed and the deal has not been completed, the two companies have been back and forth on the negotiations, involving lawsuits in courts and the French government.

The companies behind the drama

LVMH Moët Hennessy Louis Vuitton SA, commonly known as LVMH, is a French multinational firm, based in Paris, France. The firm was created through a $4 billion merger, in 1987, of fashion house Louis Vuitton with Moët Hennessy. LVMH is the world’s leading luxury goods seller, controlling around 60 subsidiaries that each handle a small number of prestigious brands, 75 in total. The subsidiaries are often managed independently, under the umbrellas of six branches: Fashion Group, Wines and Spirits, Perfumes and Cosmetics, Watches and Jewelry, Selective Distribution, and Other Activities. The oldest of the LVMH brands is wine producer Château d’Yquem, which dates its origins back to 1593. The company also owns luxury retailers, including a majority stake in DFS Group Ltd., a group of duty-free stores, and Sephora. The company sought to expand and diversify in the late 1990s through several acquisitions.

Tiffany & Co., commonly known as Tiffany’s, is an American luxury jewelry and specialty retailer, based in New York City. Tiffany’s is known for its luxury goods, particularly its diamond and sterling silver jewelry, but their offering also includes china, crystal, stationery, fragrances, water bottles, watches, personal accessories, and leather goods. It markets itself as an intermediary of taste and style. Tiffany & Co. was founded in 1837 by the jeweler Charles Lewis Tiffany and became famous in the early 20th century under the artistic direction of his son Louis Comfort Tiffany. The company operates retail outlets in the Americas, Asia-Pacific, Japan, Europe and the United Arab Emirates. Tiffany’s operates 326 stores globally in countries such as the United States, Japan, and Canada, as well as Europe, the Latin America, and Pacific Asia regions.

Why Tiffany & Co.?

LVMH, the largest player in the luxury goods market, had been looking to grow its “hard luxury” segment for some time, seeing a perfect contender in Tiffany & Co., a leading brand in jewelry manufacturing, in a period of significant M&A activity. Despite the drama around the acquisition, the operation is still the largest ever luxury deal, giving the French group led by billionaire Bernard Arnault a greater presence in its smaller segment.

LVMH is already the market leader in the “soft luxury” market, composed of clothing, leather goods, bags, and accessories, with this segment representing almost 40% of total revenue. However, the group has a smaller presence in the jewelry market, the so-called “hard luxury”, the deal would double LVMH’s size in this segment from $4,72 B to over $9 B.

The deepening of the presence in the jewelry market will increase the group’s capacity to compete with other leading players such as Richemont, Chow Tai Fook Jewellery Group, Signet Jewellers, and Pandora, in one of the fastest-growing categories in the personal luxury goods sector.

Tiffany’s network of over 300 stores across the globe would complement LVMH’s Watches & Jewelry division of 75 stores. Furthermore, the American company has greater presence in the United States, a market LVMH looks to consolidate, and among Asian consumers. In fact, Mr. Arnault believes Tiffany & Co. “would fit perfectly within LVMH’s portfolio of brands”.

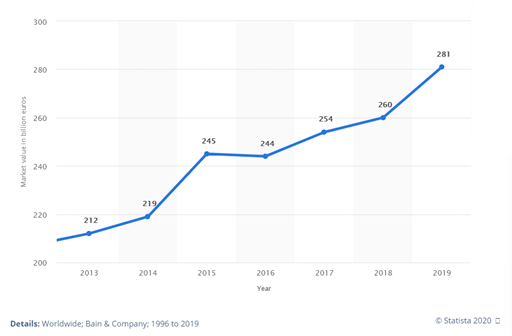

The luxury market has been growing consistently, having greatly accelerated in 2019 driven by a stronger growth of the US and Chinese markets, with the Chinese market representing the most rapidly growing proportion of the global luxury goods market, due to the expansion of an aspirational middle class. Nevertheless, the industry has seen difficulties in expanding in recent years because of changing consumer patterns, particularly among younger generations who tend to prefer experiences and services, such as travelling and dining, in comparison to luxury goods.

Also, because of the pandemic, global demand has shrunk, the luxury market is no exception as demand is expected to drop by 30% in 2020, with a recovery that could take years. Horizontal integration can be seen as a way to strengthen the brand ahead of the storm.

Despite LVMH’s growing collection of brands, regulators have not seen the deal as harmful for consumers, the European Competition Authority says there is no danger of monopolization or restriction of consumer choice. In fact, the acquisition will not alter the competitive structure of the market, because of the low market concentration. LVMH will still face competition from several other manufacturers of luxury goods, including Cartier, Van Cleef & Arpels, Richemont, among others.

Turbulent negotiations:

LVMH acquiring the American luxury jeweler for a colossal $16.2bn seemed like a “too good to be true” offer coming from the French billionaire, dubbed “the wolf in cashmere” – and it was so. The offer based on an EBITDA ratio of 17, over 50% greater than Tiffany’s 10-year average at the time, was not going to stand as the COVID-19 pandemic promised a possible 35% contraction in 2020 in the luxury market, predicted by Bain consultants, with Tiffany’s earnings closely trailing that downturn, according to the S&P Global.

When the deal was first struck, the $135 per share (37% premium at the time) supported the added value brought by Tiffany & Co, notwithstanding the closure of major markets, namely China. However, when the lockdown reached Europe, investors began to jitter, dropping Tiffany’s share price to around $114. With 35 years of experience in the luxury industry, Arnault knew that this was his opportunity to alter the deal’s terms, despite the air-tight prenup signed by both parties and the costs of backing out ($575M).

Negotiation turbulence climaxed in early September, when LVMH threatened to pull out of the deal, following a request from the French foreign minister, Jean-Yves Le Drian, to delay the deal. Tension between Paris and Washington arose, after US President, Donald Trump, imposed customs duties on certain French luxury goods, following the French’s adoption of digital services taxes. LVMH’s CFO, Jean-Jacques Guiony, stated they were prohibited from closing the deal, and uninterested in lengthening the lock-stop date, resulting in Tiffany’s share price dropping by 8.4%, to $111.67.

Nevertheless, Tiffany & Co was determined to follow through. It filed a lawsuit against LVMH claiming the conglomerate was merely attempting to strong-arm the jeweler into dropping the agreed merger price, consequently breaching the transaction agreement. LVMH hit back with a suit claiming Tiffany’s “catastrophic” performance following the pandemic indicated dismal prospects for the future. Ad interim, predictions on the deal resulted in stock price fluctuations for Tiffany & Co.

Final offer

Conflict between the giants ended with the French luxury group agreeing to pay a total of $15.8bn, at $131.5 per share – a haircut of $425M, less than 3%, of the original price. Moreover, Tiffany’s would have to pay shareholders a dividend of $0.58 per share. All lawsuits were settled. Though LMVH’s course of action seems extreme for such a modest price cut, ultimately it was able to bulk up on watches and jewelry, boosting its portfolio in the “hard luxury goods”.

Whether Bernard Arnault suffered from buyer’s remorse or went from the “wolf in cashmere” to the “lamb in lycra”, and despite the hiccups brought about by governmental intervention, legal conflict and pandemic-induced economic slowdown, this marks the largest deal ever in the luxury industry.

Sources: Financial Times, Marketline, Statista.

Tiago Rebelo

Tiago Rebelo  Nuno Sampayo

Nuno Sampayo Diogo Almeida

Diogo Almeida