For years, London has been the primary financial centre in Europe, but Brexit may allow Amsterdam and others to have a go at that title.

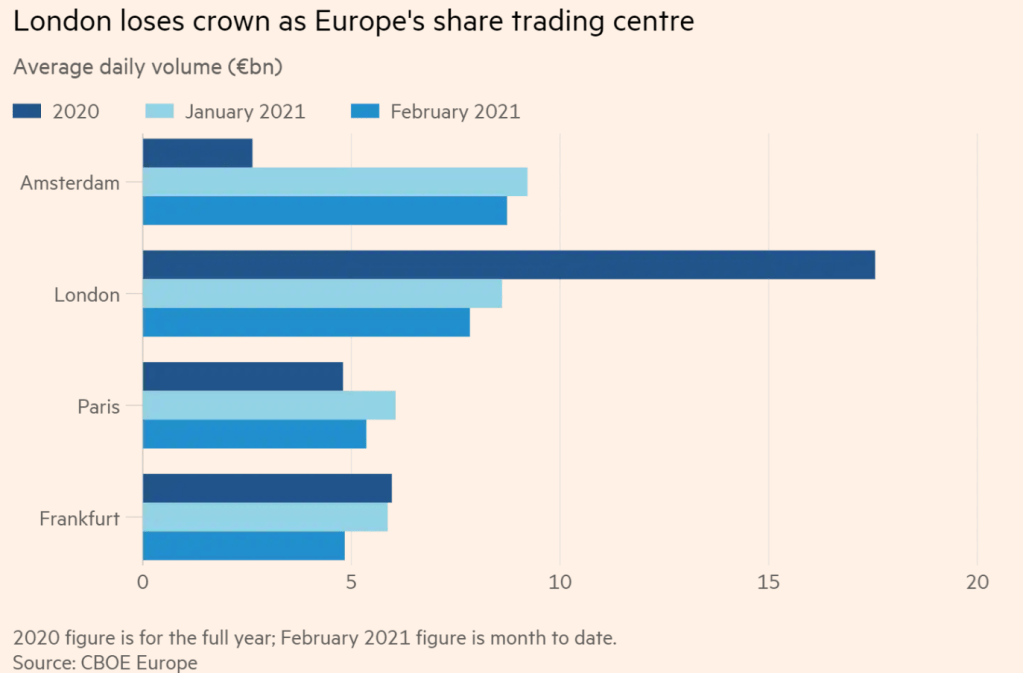

On the 1st of January of 2021, the United Kingdom (UK) finally left the EU. Immediate consequences could already be seen in the first days of UK’s exit. However, only now are we starting to have enough data to assess the true consequences of Brexit. One of the most interesting is the fact that London is no longer the largest share trading centre in Europe, having been surpassed by Amsterdam in January, which begs the question: “Is London’s status as the continent’s main financial hub under threat?”.

Before delving into the question, it is important to understand why London has been the dominant financial centre in Europe in the first place.

How did it happen?

First, it is worth disclosing that the city has always been an important trading hub, ever since the Roman founding, and, in the 19th, century, it was the political centre of the largest empire in History. But this is where most people get something wrong, as London is the composition of two cities that have their own two, distinct political entities. There is London, the one everyone thinks of as London, and then there is the less well-known City of London which is entirely surrounded by the former. The latter was founded by the Romans, and it has acquired a myriad of special privileges throughout its existence, due to its importance to the various kingdoms and nations that followed the collapse of the Roman Empire, privileges that it maintains to this day. In fact, the City had so much influence that, in the Middle Ages, Edward, the Confessor, built a new seat of royal power around an abbey he had founded in Westminster, in order to draw away power and wealth from the City. For centuries, the two cities were geographically quite distinct, only becoming indistinguishable in the 16th century.

However, the old city of London still maintains some privileges, some of them being that certain laws passed in Parliament do not apply to it. This special status is one of the reasons why so many financial services concentrate in this small area, as it has much more friendly business regulations than the rest of Europe.

On top of that, business regulations in the UK are more like the US’s than those in continental Europe, allowing for different practices in the Private Equity market, for example, and more easily attracting the financial juggernauts across the Atlantic. Combined with the language bridge, it is almost as if they are doing business in America, whilst being in Europe. Furthermore, its location allows for investors and traders to catch the end of the Asian trading day and the beginning of Wall Street’s, a privileged position in terms of currency exchange trade. Moreover, the fact that so many financial institutions decide to operate in London only attracts more institutions, as they can better harness economies of scale, by having almost all necessary complementary services and skilled human resources concentrated in the city.

The Impact of Brexit

Now, Brexit is threatening London’s envied position, as it is putting more constraints in the flows of capital and financial assets to and from the European bloc. In fact, the EU expects banks to move their euro denominated trades into the bloc by 2022, and some have already complied.

Furthermore, the UK’s financial services sector was able to provide these services to their many clients in the EU, thanks to the system of passporting for members of the European Economic Area (EEA), until Brexit was concluded.

This system consists of several different passports for various service categories that financial institutions can apply for and that allow them to provide these services to any member of the EEA. These passports also allow institutions to setup branches in the territory of other member states with much greater ease and simplicity than would otherwise be possible. Many financial institutions rely on several different passports at once to provide the range of different services that their clients depend on.

After Brexit, with the UK’s exit from the single market, the passporting system is no longer available to the UK’s financial institutions. Instead, they will need to depend on individual licensing in each EEA country they wish to operate in. These licenses, often, are not as comprehensive or as easy to obtain as the previous passporting system. Furthermore, it forces institutions to setup branches in other countries that they might not otherwise need, creating needless costs and inefficiencies.

Nevertheless, there is a potential agreement that would solve some of the problems the loss of passporting brings, which is an “equivalence” agreement in which Brussels and London would both agree to recognize some aspects of the other party’s financial supervision rules as equivalent to their own, and that would alleviate some of the frictions that have been registered since the start of the year. However, so far, there has been no agreement on equivalence.

Due to this, London’s trading markets of shares were hurt in January, as EU-based financial institutions were unable to trade, due to the lack of equivalence. Subsequently, trading of shares and other instruments has been flowing out of London into other European and American markets, with Amsterdam emerging as a clear winner and surpassing the City in share trading volume. “The city’s sudden dominance in European equity transactions goes back to Brexit contingency plans drawn up months ago. Both Cboe and the London Stock Exchange Group Plc’s Turquoise platform chose the Netherlands as their alternative site for EU share trading”, Bloomberg states, which is likely due to its business-friendly environment. Notwithstanding this, the more probable outcome in the long run is that many of the European operations that were previously done in London will be spread out through many cities besides Amsterdam, such as Frankfurt, Milan, Paris, Madrid. There probably won´t one single winner.

A potential agreement on equivalence would not return to the City the ease of access to EU markets it had with the passporting system, as it covers fewer areas and services and is a unilateral agreement that could be withdrawn by the EU at any time. But even the prospect of full equivalence that many UK-based financial firms are hoping for is unlikely, since the EU wants to assert its financial independence and fears the UK may try to deviate its financial rules from those of the EU.

Still, even though it may seem that the EU can only gain with this outcome, one cannot forget that the EU’s financial activities were mainly conducted in London for a reason, and, with Brexit, firms’ access to capital markets and liquidity will not be as straightforward as it was prior to it. These added inefficiencies could hurt the EU, but the extent of the harm is still uncertain.

Final remarks

Despite Brexit, London will most likely remain a very important financial centre, perhaps even maintaining the status as Europe’s main financial hub, but the gap between it and its rivals will be smaller. Moreover, an agreement on equivalence in certain specific sectors is a likely option, but, given the more protectionist attitude of the EU, it is not probable this will be an agreement that ensures full equivalence.

All in all, the fears of London’s financial centre disappearing altogether are a bit exaggerated, but the city will also not come out unscathed, as many would hope. London is not just an important financial hub for Europe. It is important for the whole world, forming a crucial part of the current daily financial cycle of the globe, that encompasses other squares, like Tokyo and New York. But its importance for Europe will most likely decrease in the long run. As usual, reality is neither black nor white, but greyish.

Sources: Bloomberg, Financial Times, Investopedia, Marketplace.org, The New York Times, Wikipedia.

Rodolfo Carrasquinho

João Baptista