Despite being the second biggest market in the world after the U.S. Treasury market, the truth is that you most likely haven’t ever heard of the Eurodollar system. This market, where some of the most sophisticated markets participants operate, is giving us warning signs of slowing economic growth. This might clash with some of the inflationary thesis defended nowadays.

But what is the Eurodollar system? And how does it work? What signal is this market giving us and why should we care about it?

What is the Eurodollar system?

In its simpler definition, as the name indicates, the term Eurodollar refers to US dollar deposits held at foreign banks or overseas branches of American banks, which originally operated mostly in Europe, hence the name. Indeed, while it is not entirely clear when this Eurodollar market was initiated, it is believed to date as far back as the post-World War II period, when Europe experienced a wide circulation of American dollars via the financial aid that the US provided to the war-torn continent in the form of the Marshall Plan. Thus, when the Eurodollar system began, it was mainly supported by the emergence of dollar money centers in Zurich, Munich and, of course, London.

However, what started as a fundamentally European-based independent and less regulated market of US dollar funds, rapidly spread across the globe in the next few decades, with many American branches opening operations in all continents. Therefore, as globalization grew and this “secondary” dollar market started expanding – going as far as replacing a lot of the traditional roles of global reserve currencies, such as gold – the Eurodollar system became a much more complex concept that now encompasses a much wider dimension of currencies and operations, representing one of the world´s biggest capital markets.

As Eurodollars are largely held and traded outside of US jurisdiction, they are not subject to the Federal Reserve´s regulation, particular in terms of reserve requirements, leading these deposits to be able to pay higher interests. Furthermore, by operating outside of the FED´s radar, this currency-like system of interbank liabilities allows for sophisticated financing and monetary transactions of US dollars to take place, making it so these international banks that deal with Eurodollars get to work with their own money multiplier, thus being in charge of creating and controlling their supply of US dollars.

Overall, the Eurodollar system became an alternative to traditional currency reserves, being able through its independence to provide the liquidity needed to satisfy demand in a way that, on many occasions, other systems (ex.: Bretton Woods) failed to do so, conferring the confidence that this “shadow” money would be the modern alternative to easily supply financing under the panorama of a globalizing world. This has consequently been reflected in high volume circulation of major international capital flows between countries under the Eurodollar system in the past decades, – with most transactions in this market being conducted overnight – which could potentially have significant geopolitical ramifications, seeing the power that this reserve-less, regulation-less system confers to the major international bankers that oversee it.

How does the Eurodollar work?

As mentioned previously, the offshore banks operating in the Eurodollar are not subject to regulations from Central Banks meaning that they don’t suffer from reserve requirements. This allows for a much higher flexibility to create dollars (being it a purely ledger transaction).

The deposits in the Eurodollar system have a minimum amount of $100.000 and are generally above $5 million and are priced in two different ways: either Overnight Deposits or, for longer maturities, tied to the London Interbank Offered Rate (LIBOR).

Overnight deposits are the most common transaction in this market, they mature on the next business day and usually start on the same date they are executed, with money paid between banks. The overnight bank funding rate is computed according to federal funds transactions, certain Eurodollar transactions and certain domestic deposit transactions.

Regarding longer maturities, Eurodollar is a LIBOR-based derivative. In this situation Eurodollar’s price reflects the market gauge of the 3—month U.S. dollar LIBOR, a benchmark for short-term interest rates at which banks can borrow funds in the London interbank market, interest rate anticipated on the settlement date of the contract.

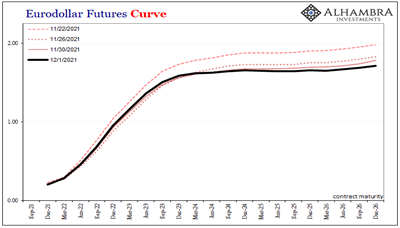

Inversion of the Yield Curve

Eurodollar futures are derivative contracts that allow buyers and sellers to hedge against interest rate risk in the future. It also allows speculators to bet on the future movements of the USD LIBOR rate. In the Eurodollar yield-curve, the short-term tenors are heavily affected by the Federal Reserve actions (namely by the defined interest on reserves – IOR), while the longer tenors correspond to market expectations on inflation and economic growth.

A Eurodollar futures curve can be built similarly to the treasury rates yield curve: the different future contract maturities are plotted on the x-axis and their associated interest rates are plotted on the y-axis. Under normal conditions, the curve should be upward sloping, reflecting the expectation of economic growth further down the line.

Inversion is not a normal shape for the curve, and it has, historically, preceded turmoil periods for global markets. For example, the last inversion happened on the 13th of June of 2018 where the inversion occurred in the Dec’20 to Sept’21 contracts. This doesn’t mean that the Eurodollar market predicted the Pandemic crisis but that it rather anticipated the deflationary forces existing in 2018 to play-out, namely the collateral scarcity on the Eurodollar system.

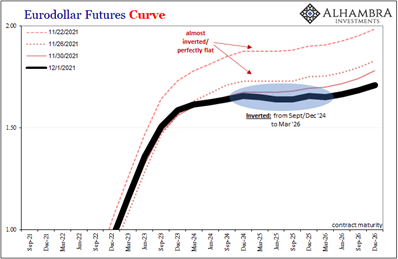

This same phenomenon was seen on the 1st of December of 2021, where the Eurodollar yield curve inverted between Sept/Dec’24 and Mar’26 contracts. This means, once again, that the sophisticated participants in this market expect the existing deflationary forces to impact economic growth.

The inversion of the yield curve in the maturities around 2024, 2025 and 2026, might suggest that the market doesn’t believe that the Federal Reserve will be able to maintain higher interest rates for a very long time. This could be the case because the market believes that the upcoming contractions in the supply of money in 2022 will cause a slowdown of economic activity, which would cause the Federal Reserve to cut interest rates once again.

Conclusion

The inversion of the Eurodollar yield curve, the flattening of treasury yields and the shortage of dollars in the system are some of the signs that indicate that deflationary forces are threatening economic growth. This might invalidate some of the inflationary thesis as the market participants reiterate their belief that there is no monetary inflation. This inversion might also be a response to a possible monetary policy error by Central Banks, as they plan to tighten into a seeming weak economy.

Sources: Investopedia, Alhambra Investments, Fxstreet

Diogo Almeida

João Baptista

Inês Lindoso

João Correia