Russia’s relationship with its debt has not been easy throughout history. In 1918, the embryonic Soviet Union repudiated the debt carried from the previous regime; in 1998, and after an attempt from the Russian Federation to gain credibility and integrate in international capital markets, Russia ended up defaulting in its domestic debt and in the Soviet-era external debt; in 2022, a Russian default seems to be looming once again.

With the Russian invasion of Ukraine, international markets price in the potential for a Russian sovereign debt default in external debt. Yields on Russian 10Y bonds, for example, have climbed vertiginously to nearly 20% since the beginning of the war.

An history of missed payments

Following the Bolshevik revolution and the overthrowing of the Tsarist regime, the embryonic Soviet Union, in 1918, repudiated all the debts of the previous regime. Despite this, throughout the Soviet experiment, the Soviet Union accumulated large levels of debt up until its dissolution in 1991.

After the breakup, the newly independent, former Soviet states, had an arduous road of restructuring their systems with more market-oriented economies in their sights. At that time, the Russian Federation assumed all foreign assets and debts of the former Soviet Union, an action that it viewed to be necessary to begin to integrate international capital markets and to build a good international reputation.

However, the restructuring of the economy proved to be more challenging than expected. Russian GDP suffered large contractions, decreasing nearly by half in the following years. At the same time, fiscal policy was quite loose with the government running large deficits and real interest rates were kept high as the new Central Bank tried to rein in inflation and create credibility. Together, these factors meant that Russian debt was not on a sustainable path throughout the 1990’s. In 1998, and although Russian debt was still not very high (60% of GDP), with the Asian financial crisis echoing throughout the markets, and the exchange suffering sharp devaluations, Russia ended up defaulting on its domestic debt, as it found itself unable to rollover existing short-term debt. And although Russia did also default on foreign Soviet-era obligations it honored all the external debt it had issued after the 1991, attempting to maintain good credibility.

With this same goal in mind, following this default, Russia sought assistance from the IMF, and was able to restructure the defaulted debt and implement structural reforms that placed it on the path towards sustainable debt management.

These changes can be seen in the evolution of sovereign debt ratings, which had deteriorated significantly during this crisis (S&P – SD), but that steadily rose in the early 2000’s. S&P rated Russian debt with a B in 2001 a grade of BBB in 2008. This grade was kept quite constant until recent months. Even now, although Russia finds itself in danger of defaulting, similarly to the 1998 crisis, its debt to GDP ratio is not very high (18% of GDP in 2020).

The importance of international capital markets and the credit rating system

Countries issue bonds in external debt markets as a way to collect the necessary funds to finance their sovereign debts; the associated price and respective interest rate at which they will trade will reflect a number of conditions that determine their risk level, which usually comes attached with a given credit rating.

Credit ratings will reflect the creditworthiness of the country in question, posing as an indicative tool for investors of the possible risks that are being undertaken when investing in said debt – which in turn will be translated into the interest rate at which the loan will be repaid. This risk represents the likelihood of the government failing to make the future payments associated with its debt obligations, either because it is unwilling or unable to do so, with risky investments being linked with low credit ratings and high interest rates. The level of risk assigned to each country will be determined taking into consideration the country’s economic and political environment, assessing several important indicators such as the country’s debt service ratio, variance of its export revenue, domestic money supply growth, among others. Overall, a good or bad credit rating could make or break a country’s economy, being a key factor in attracting foreign direct investment.

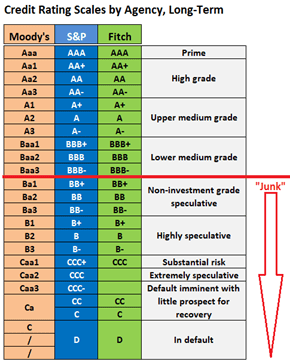

These credit ratings are assigned by independent credit rating agencies, with the three most widely known being Moody’s, S&P Global and Fitch Ratings. Each of these credit agencies will attribute a credit rating to the investment in question expressed in letter grade format, in accordance with their personal measurement scale: in alphabetical order, usually from A to D (best to worse), with specific intermediate categories for each agency. For example, S&P attributes a BBB- (or higher) rating to countries it considers to be within investment grade and Moody’s does so for Baa3 (or higher) rated bonds. Any rating of BB+ (or lower) for S&P and Ba1 (and below) for Moody’s falls to speculative grade, commonly referred to as the “junk” bonds territory.

Credit ratings are most definitely not static and may change all the time based on the newest data available on a multitude of political and economic factors, as the recent case of Russia government bonds´ credit rating steep downfall showcases. In fact, in just a few weeks, given the recent turn of events – with Russia´s economic panorama suffering a major hit facing the tight trade restrictions from the West and being essentially cut-off from Western financing – all major rating agencies have downgraded the country´s status by considerable significant notches from its secure position in the “stable” B territory, fearing Russia´s inability (and even to a certain extent its willingness) to service its debt. The situation further escalated upon President Putin´s announcement of the possibility of a “redenomination of foreign-currency sovereign debt payments into local currency for creditors in specified countries”, prompting the rating agencies to believe “that a sovereign default is imminent”, as illustrated by Fitch´s C rating and Moody´s equivalent Ca score, both only one level above default.

The impact of the Russian Invasion

The invasion of Ukraine has seriously influenced Russia’s economic and monetary landscape, mainly due to the package of sanctions applied by several European Union countries and the United States. Indeed, Putin admitted that such sanctions “effectively declare Russia default”, as they imply an increasing probability of default on its public debt (20% of its GDP). Nevertheless, what frightens Putin is not this amount, but the current lack of payment capacity.

Firstly, the sanctions applied to Russia, which include its exclusion from the SWIFT banking system and the blocked access to western financial markets, place this country in a possible economic drowning situation. In fact, according to the public finance sustainability theory, debt is only sustainable if the GDP growth rate is higher than the interest rate. Therefore, given all the economic and commercial exclusion to which Russia is currently exposed, it is possible that its GDP growth will not be satisfactory enough, consequently increasing its financial susceptibility and its risk of default. Besides the economic point of view, other sanctions applied imply the freezing of Russian assets located in institutions outside Russia, such as foreign exchange reserves and Russian bonds, which strongly limits the Russian capacity to pay its obligations.

Furthermore, apart from all the economic implications that trigger the default, another reason is closely linked with the monetary problems faced by Russia. For now, since the invasion of Ukraine, the ruble has devalued by around 40% against the dollar, once again compromising Russia’s monetary capacity to pay its debt. Then, the problem starts when its $480 billion foreign debt is denominated in US currency, so it must be paid in dollars. In fact, according to international declarations by financial institutions, the inability to pay debts in the original currency is formally considered as default. Moreover, nominally paying in rubles will get much more expensive for Russia given its huge drop in recent weeks.

Conclusion

Against the general feeling that Russia wouldn’t be able to make its next bond payment due on March 16 (with a 30-day grace period), it was able to do so. Still, it seems to just be delaying the inevitable given the weak economic outlook and the impact of sanctions.

What this will represent for the world economy is still murky but seeing as only a relatively small sum of the nation´s debt is held by foreigners; all points out to the country´s potential default not posing a major systemic risk to the global financial system.

Sources: Reuters, Fortune, IMF Elibrary, Carnegie Endowment For International Peace.

Diogo Almeida

João Baptista

Sara Robalo

Inês Lindoso

João Correia