Did you know that Millennials make up about 27% of the world’s population? Maybe you didn’t but this information comes from a science that we all know and yet often don’t give its due value: Demography.

Demography is, by definition, the study of statistics such as births, deaths, income, or the incidence of disease, which illustrate the structure of populations. The individuals that study these factors are called demographers.

In fact, this science led to curious conclusions, like the one at the beginning, but this science is much more and more complex than that. As we will show to you later in this article, demography has a very close link to the economy, as it is with the data collected and treated that, for example, financial, banking, or even insurance institutions establish their rates and conditions.

There are many factors that demography considers, but the most important ones are population size, population density, age structure, fecundity, mortality and sex ratio. All these factors affect the economy: for instance if population size decreases the working-age population will also decrease, which reduces labor input and leads to a slowdown in economic growth, resulting in the end in a decreasing growth rate of GDP per capita.

Different Countries, different demographics

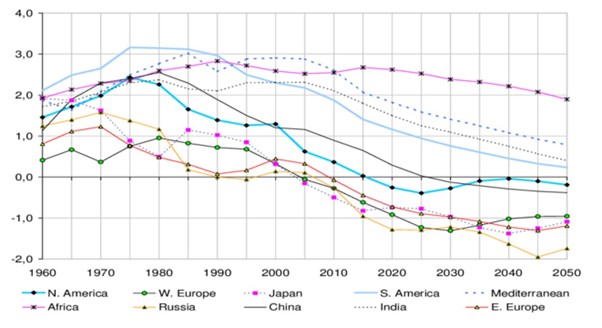

During the last 20 years, the global demographic landscape has suffered several changes in terms of population, age structure and wealth. Nevertheless, these changes are not linear across the globe, so there are various countries with very different demographic trends due to other variables such as culture and climate.

Demographics in developed countries

Developed countries, such as the United States, Japan, and European Union member countries are generally characterized by their high level of industrialization and high income per capita. Their population structure is estimated to have already peaked and so, the total population is expected to gradually begin to decline due to low birth rates and rising average age. In fact, it is estimated that in the most developed countries the population over 65 years old will reach 25% of the total population by 2040. In relation to Europe, the projected average age is 47 years, although it is estimated that the people in Greece, Italy and Spain will age faster. Japan and South Korea will reach average ages of 48 and 44, respectively. In these circumstances, a slowdown in productivity is expected, as well as an increase in the GDP share earmarked for pensions and medical care for the elderly.

During the next 20 years, a strong trend of immigration to developed countries is estimated due to their stability, quality of life and economic incentives despite not being able to change the overall structural direction.

Demographics in emerging countries (China, India)

In emerging countries, some Asian countries follow the same trend as European ones, although slower. That is, while European countries have already passed their populational peak, Asia will see its population increase exponentially until 2040 and then gradually decrease. Besides, it is expected that by 2027 India will be the country with the most population, surpassing China.

In terms of their human development evolution from demographic scenario, it is expected drastically improve given the increase in the proportion of working-age adults, greater female participation in the workforce and higher social stability in the most advanced age groups. However, the increase in development is thought to be faster than the increase in income, particularly in China, posing some challenges for governments.

Demographics in Underdeveloped Countries

The reality of developing countries is completely dichotomous from that of developed countries, not only at the economic level, as the former have a very limited level of industrialization and low per capita income, but mainly at the demographically. For example, countries like Sub-Saharan Africa have an infant mortality rate 18 times higher than the average of developed countries, whose infant mortality, on average, is less than 1%. Moreover, other differences strongly affect both birth and death rates, which are quite high, due to weak and limited health services, lack of access to information and contraceptive methods and few professional prospects, resulting in a short average life expectancy.

Developing countries are expected to increase their level of urbanization in the coming years, as their key development factor. In fact, according to the UN Report, the number of urban workers will increase from 1 billion to 2.5 billion in 2040, which suggests a huge boost in the development of these countries. However, the speed of urban growth is not enough to keep up with population growth – like in the case of Sub-Saharan Africa, whose population is expected to double by 2050, so these countries will probably overload their capacity to provide infrastructure and educational systems, necessary to enhance economic growth and human development.

Impact of demography on interest rates, savings and investment

Demography, particularly in aspects such as population ageing, will have a determinant impact on interest rates, bringing attached serious consequences for household savings and investment. Therefore, it is fundamental to take into account how current demographic trends like increasing life expectancy and the decline in fertility rates (with the baby boom generation moving higher up in the demographic pyramid) will impact the savings and investment market.

First, it is crucial to understand how net savers and net borrowers are usually distributed in an economy across different age groups. In accordance with the life cycle model developed by Franco Modigliani, savings are expected to vary across a person´s lifetime in a U-shaped form, suggesting that younger people and the elderly are usually those that actively save the least, whereas the middle-aged are responsible for the biggest share of savings. This is related to the notion of consumption smoothing over a person´s life, making it intuitive that people are more prone to save when they have higher incomes to then use these resources for times in which their incomes are relatively lower (during retirement or in the early years of their careers when their wages are usually lower).

Related to the notion of population dynamics, we can start by exploring how life expectancy will influence the savings market. Considering the case of increasing life expectancy that has been more or less experienced all across the globe in recent years, keeping the retirement age constant, it would imply that people would have to spread out their accumulated resources over the course of their lives over a longer retirement period. This, in turn, will trigger two different scenarios: one in which people anticipate this and increase their savings rate to offset the impact – resulting in a lower interest rate – and another in which they do not adjust their savings accordingly, leading to lower resources in the long-run and a higher interest rate.

On another note, we can also look at the effect of birth rates on savings and investment. Taking into account a reduction in birth rates, we can distinguish two effects. On one hand, it results in lower population growth, consequently contributing towards a lower GDP growth and thus a decrease in demand for investment – pressure for a lower interest rate. On the other hand, it contributes towards a higher number of the elderly/middle aged relative to the young; with the elderly usually being associated with lower savings rate but higher accumulation of capital, this will make it so two contrasting forces will clash, with the lower savings rate contributing towards a higher interest rate but a higher volume of accumulated savings/capital having the opposite effect. As for the fact that the middle aged are also to occupy a much more preponderant role in the population composition, as the savers of the economy, they will contribute to a higher demand for financial securities, hence pushing interest rates downwards.

With so many forces at play, the overall impact of demographics on the investment/savings market is rather unclear, even though all seems to point out that the current downward pressure on interest rates that has been felt in the past decades/years in developed (and ageing…) economies is likely here to stay, probably being itself already a manifestation of the impact of demographic trends on this facet of the economy.

Can productivity save the weak demographics in developed countries?

Increases in productivity can lessen the impact of such population shifts, and technological advances are the ideal source of productivity boosts. This, however, is a double-edged sword. On one hand, technological progress increases productivity, but at the same time, it can eliminate jobs, increasing unemployment.

Since the 2008 financial crisis, year-on-year productivity growth has slowed. Still, even though the rate of productivity growth has slowed, the absolute output per worker is now the highest it has ever been in real economic terms. This highlights the offset of productivity on demographics as there are fewer and fewer people in the workforce but a higher productivity per worker.

Conclusion

Demographics do not determine the fate of economic growth, but they are certainly a key determinant for an economy’s growth potential. An ageing population coupled with a declining birth rate in the developed world points to a decline in future economic growth.

Sources: Office of the Director of National Intelligence – Global Trends, Harvard Business Review, Caixa Bank Research, Warwick, Fraser Institute.

Diogo Almeida

João Baptista

Sara Robalo

Inês Lindoso

João Correia