Growing concerns on the stability of the financial sector 2023 has seen a wave of bank failures, from Credit Suisse in Switzerland to Signature and Silicon Valley Bank (SVB) in the United States (US). These recent collapses of prominent banks have sparked concerns about the stability of the financial sector, leading to a surge in Google searches for “financial crisis” not seen since 2008. Given the already-present fears of a recession, the collapses only added to the public’s anxiety, shaking consumer confidence in the economy. While the situation is unsettlingly familiar, the uncertainty and fear of contagion remain daunting. This latest banking crisis highlights the potential side effects of financial disarray and underscores the need for swift and effective intervention to restore stability. To exemplify the bank failures and bankruptcy, this article will focus on the case of SVB.

A perfect combination of events leads the “bank of start-ups” to collapse

Known as the “bank of start-ups”, especially for those in the tech sector, California-based SVB was established in 1983, with the mission of helping “individuals, investors and the world’s most innovative companies achieve their ambitious goals”, counting as their clients start-ups and tech companies of the likes of Shopify or Insight Partners. In 1988, they went public through an IPO on Nasdaq and, in 2008, they went international. But how did a bank that was the 16th largest bank in the United States, reporting, in Q4 for 2022, $212B in assets, $342B in total client funds and $74B in total loans, collapse on the 10th of March?

The short answer to this question revolves around the typical suspect when referring to the failure of banks: bank runs, which are a self-fulfilling prophecy. However, in the case of SVB, it can be seen as a perfect combination of events which led to this disastrous outcome. The first motive can be linked to the Federal Reserve’s decision to increase interest rates to fight the increasing inflation rates, which are corroding American consumers’ purchasing power. This macroeconomic environment would lead SVB’s long-term investments in government bonds to be eroded as SVB had $21 billion invested with an average yield of 1.79%, as they had been purchased when interest rates were near the zero-lower bond. In comparison, currently, a 10-year Treasury bond has a yield of around 3.9%. Simultaneously, startups were raising fewer rounds of venture capital investment, due to the current economic environment, which decreased the amount of deposit inflows and increased the outflows. So, SBV’s cash decreased, such that the bank had a lower amount of resources to finance its operations. Consequently, in order to raise funds, SVB resorted to the sale of their government bonds. However, as they were yielding a lower interest than those that investors had access to if they bought directly from the government, this led SVB to sell a portion of said bonds at a discount to compete with the competitive market, resulting in a loss of $2 billion. The ultimate blow to SVB’s credibility would be the capital raise announcement, resulting in a generalised panic amongst SVB’s depositors, as more than 90 percent of them exceeded $250,000 in guaranteed Federal Deposit Insurance Corporation (FDIC). At the end of last year, according to the Wall Street Journal, SVB had over $150 billion in uninsured deposits. Fear led to large withdrawals, with depositors pulling out $42 million, in just one day alone. Consequently, SVB’s stock plummeted.

To avoid a widespread panic and broader contention, despite appearing that SVB’s problems spilt over to Signature Bank, the government intervened in the form of California regulators shutting the bank down and placing it in receivership under the FDIC with SVB’s senior managers, including its CEO, Greg Becker, being removed. SVB’s collapse has been deemed as the 2nd largest in American history, only losing to Washington Mutual which collapsed in the 2008 Financial Crisis. Furthermore, in an unusual decision, the FDIC agreed to guarantee all SVB deposits, even those above the $250,000 per account threshold.

What else is being done?

Deputy Treasury Secretary, Wally Adeyemo, sought to reassure the public about the health of the banking system after the sudden collapse of SVB, in an exclusive interview to CNN, stating: “Federal regulators are paying attention to this particular financial institution and when we think about the broader financial system, we’re very confident in the ability and the resilience of the system”. In reality, the 2008 financial crisis prompted stricter regulations in the United States and around the world. In response, regulators imposed more rigorous capital requirements on American banks, with the aim of preventing the collapse of individual banks from having a ripple effect on the wider economy and financial system.

Following the collapse of SVB, federal regulators acted promptly to mitigate depositors’ losses and restore trust in both the banking system and the broader economy. To achieve this, they put into effect a series of measures aimed at reassuring the public and bolstering confidence in the financial sector. The government introduced a program called the Bank Term Funding Program (BTFP) – a lender of last resort facility- which serves as a safety net for financial institutions. This program, which is backed by the Federal Reserve, provides loans to banks, credit unions, and other deposit-taking institutions in times of need. The loans can last for up to one year and enable these institutions to meet the needs of their depositors without having to resort to selling their high-quality securities at short notice.

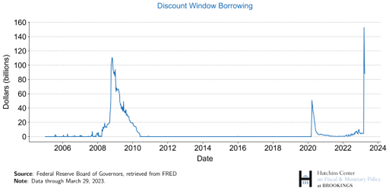

Another way the government relied on to regulate the financial industry differently was through a discount window, a facility that offers banks the option to borrow cash on a permanent basis, typically for short periods, such as a few days or weeks. From March 9 to March 15, borrowing at the discount window escalated from $4.6 billion to $152.9 billion, before declining to $88.2 billion by March 29. However, the decrease was mostly offset by augmented borrowing through the BTFP.

Numerous banks overseas borrow and lend in U.S. dollars. Although foreign central banks possess the capability to print their own currencies, like Euros, Yens, and British pounds, to lend to their struggling banks, they do not have the authority to print U.S. dollars. In response to the Global Financial Crisis, the Federal Reserve initiated a sequence of agreements with foreign central banks, whereby it would exchange U.S. dollars for foreign currencies with other central banks. On March 19, 2023, the Federal Reserve announced that it would conduct daily swaps at least until the end of April to enhance the efficacy of the swap lines.

In the end, the FDIC’s race to find another bank willing to merge with SVB to safeguard unsecured deposits was successful as First Citizens Bank purchased SVB’s remaining assets, deposits, and loans.

Conclusion

Bank failures like this have happened before—there were more than 550 banks shut down between 2001 and the start of 2023. But this one was particularly newsworthy due to its dimension, being the second-largest bank failure in US history.

There is now less anxiety about the stability of the banking sector due to the significant regulatory reforms put in place after the crisis in 2008 and the steps taken by the Federal Reserve following the collapse of SVB to improve confidence in the banking system and prevent future banking failures. The risks of broader contagion are thought to be limited for now but, even if a recession occurs, analysts don’t think it would be as long lasting as the Great Recession.

According to Mike Mayo, a senior bank analyst at Wells Fargo, back in the prior crisis “Banks were taking excessive risks, and people thought everything was fine. Now everyone’s concerned, but underneath the surface the banks are more resilient than they’ve been in a generation.”

Sources: The Economist, TIME, Silicon Valley Bank, Wall Street Journal, CNN, The American Prospect, CNN Business, Investopedia, Brookings, Expresso

Hannah Ribeiro

Pedro Teixeira