The nationalization of TAP Air Portugal (hereby simply referred to as TAP) has been a hotly discussed topic recently. In this article, the major pros and cons of such a move by the Portuguese government are put into perspective, during a time in which taxpayers cannot afford to cover a bad decision from those in charge.

Founded back in 1945, under the Estado Novo dictatorship, TAP was initially a private company. During the first three decades of existence, its development occurred at a slow pace, mainly due to the fact that Portugal was a poorly internationalized country by the time. With the deposition of the regime, which led to the nationalization of the company (along with many other businesses), and a further global integration of the country, TAP could grow, expanding its routes and reaching more points on the globe. The fact that TAP took almost 20 years to reach the one million passengers milestone, compared to the 17 million attained in 2019, is a proof of the tremendous development registered not only by the company, but also by the sector as a whole.

What’s the company’s current situation?

Despite the pronounced long-term growth of the aviation industry, TAP exhibits long-lasting liquidity/solvency problems, presenting, year after year, worrying financial statements. As a matter of fact, the incapability of the firm to deliver sustainable results throughout decades led to its reprivatization (2015) in the aftermath of the financial crisis that hit Portugal.

Before diving into the numbers, let us proceed with a brief characterization of the firm’s organization nowadays. In fact, the aviation company itself, TAP SA, belongs to a holding, TAP SGPS, founded in 2003. Besides TAP SA, the group owns eight additional subsidiaries working on related businesses, such as catering, maintenance, cleaning services and computer engineering.

In 2015, under Pedro Passos Coelho’s government, the group was privatized and the Atlantic Gateway consortium, headed by David Neeleman and Humberto Pedrosa, acquired a participation of 61%. Later, in 2016, António Costa’s office partially reverted the process and secured a 50% share to the state, assuring an even split across private and public ownership. This ended up translated into an ambiguous shareholder structure, which has remained unchanged since then. But for how long?

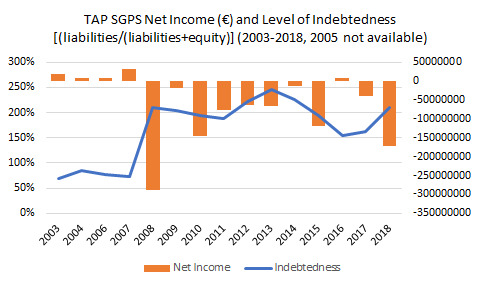

TAP SGPS is in severe financial distress. The graph below says it all. In 2008, owners’ equity became negative and net income simply disappeared, almost never to be seen again. To make things even worse, the level of indebtedness is currently at dangerous levels (above 200%) and, even though the expansion of the aircraft fleet has been contributing to increased assets, liabilities struggle to be reduced. In finance, such analysis should ideally be conducted via peer comparison, but the values presented (namely, those relative to income) are intrinsically poor and are a good portrait of the group’s frightening financial situation.

Data Source: Sabi Nova SBE

Should TAP become a state-owned company again?…

In this dramatic scenario, one may wonder what factors could be a justification for state ownership, as the financial situation does not seem to be one. Consequently, on the one hand, nationalization’s supporters argue that private management would only care about profit and this would potentially mean the elimination of important routes for the Portuguese community, such as the links with Guiné-Bissau or Cabo Verde. On the contrary, the state would defend the best interests of citizens, even if they led to inefficient outcomes. In this domain, the fact that most European countries have state-owned airlines is often used as an authority argument to back nationalization.

Another idea in favor of state control is the role of ambassador of the Portuguese culture that TAP is believed to play abroad. The defendants of this thesis argue that, by becoming private, the brand would lose connection to its Portuguese background and start to be seen as just another airline, which would harm Portugal’s international exposure. In fact, this is one of the main concerns of António Costa’s government, which considers TAP as a «strategic company». Taking into account that the aviation industry is among the most affected by the COVID-19 pandemic, he says that the government will avoid its bankruptcy at all costs. Also, TAP employs more than 10,000 people nowadays and many believe that privatization, a merger or an acquisition by a competitor would mean many jobs lost.

Could thousands of employees fill unemployment claims in case of privatization?

… Or should it be effectively privatized?

On the privatization side, people argue that the state has no right to arbitrarily inject taxpayers’ money into a company near bankruptcy and which can well be run by a private entity with no prejudice for national interests. If for a bank that is admissible due to systemic risk, an airline company is not believed to be worth of taxpayers’ effort, especially considering that there are loads of similar companies providing the same kind of services, many times at a lower cost for the client.

An interesting counterargument to that of national interests is precisely that, as opposed to the theorized, TAP does not defend the interests of Portuguese citizens, but rather those of Lisbon. The company is accused of regionalism, namely owing to the fact that it announced the re-establishment of more than 70 routes from Lisbon and just 3 from Oporto after the lifting of containment measures. So, if the company only serves one city, it is argued not to be fair that all taxpayers are equally liable for it.

To rebut the vision of job posts loss, the apologists of privatization argue that, if TAP goes bankrupt, other companies will come over and fill its place. This would mean that, despite scale advantages, most workers will not lose their jobs, but will rather be hired by other companies. In the context of Lisbon’s airport, given TAP’s large share, this could mean lower fees in case of bankruptcy, as competition would increase. The case of the United States of America seems to support this theory. After World War II, the country deregulated airlines market and, despite Pan American (their public company by the time) went bankrupt, the increase in competition led to lower fees and routes’ expansion.

What does the future hold?

At this moment, there is no certainty about the future of TAP and, even though state’s help (through convertible bonds, for instance) is a possibility, nationalization is unlikely to happen, as the burden it would imply on households during these times would be massive. Extraordinary times demand extraordinary policy action, but taxpayers could well not be able to deal with a questionable public rescue to TAP.

Sources: ECO, Jornal de Negócios, NiT, Notícias ao Minuto, Sabi Nova SBE, Showbiz Cheat Sheet, TAP, Wikipédia