Do Revolut or N26 sound familiar? They are some of the most known fintechs in Europe. Both present themselves as alternatives to the traditional banking sector. The first is from the United Kingdom and the latter is based in Germany.

If you’re Portuguese, you are probably familiarized to MB Way and have heard about PPL Crowdfunding, a crowdfunding platform as its name suggests.

Fintech’s are revolutionizing modern banking, among other financial services.

Briefly, “fintech” stands for financial technology and represents the term used to name companies that exploit technological advantages to provide more efficient, lower cost and more user-friendly financial services.

Revolut is maybe the most known example of a fintech unicorn [term used to name tech companies valued above $1 billion].

Without a physical presence (it doesn’t have any bank infrastructure like Barclays or BBVA), this fintech is able to provide most of the financial services offered by the big banks at a lower cost and with a more user-friendly interface. You may transfer money between two different country-based banks without any intermediation fees for example. In this case, the United Kingdom’s based unicorn is clearly a Competitive Fintech Venture as it competes with the traditional banking sector.

Another type of fintech is what may be called a Collaborative Fintech Venture: this kind of company aims instead at complementing the traditional financial services. An example of these ventures is the MB Way service, provided in Portugal by SIBS, a company mainly held by the national big banks. It initially enabled consumers to easily transfer money between different bank accounts, using only the client’s phone number. This way, consumers have an additional feature linked to their bank account and are therefore more pleased with their banking services.

So, should the big banks feel threatened by fintechs?

Fintech is creating opportunities for customers and businesses alike, Bank of England Governor Mark Carney said.

“In the process, however, it could also have profound consequences for the business models of incumbent banks,” said Carney. So, should the big banks feel threatened by fintechs?

The BoE, in its 2017 stress test, said the tested major banks (HSBC, Barclays, Lloyds, RBS, Santander UK, Standard Chartered and Nationwide) concluded that they could withstand continued low growth and fintech competition without making big changes to their business models or taking on more risk.

[Reuters] However, the BoE stated that the fintechs’ competition could cause “greater and faster disruption” to these banks’ business models than even these institutions project.

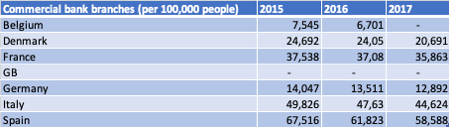

Number of commercial bank branches in Europe (per 100,000 people)

Number of commercial bank branches in Europe (per 100,000 people)Also, as digital payments gain terrain over the use of bank notes and coins, the ATM network in these same countries has dropped on average 2.5% since 2015, which leaves room for fintechs in the payments’ sector, like Stripe, based in San Francisco. Stripe started as a service to help small online sellers process payments and now serves tech giants like Amazon and Microsoft. It now presents other products, like a credit card issuing technology and its latest valuation, dated from Jan. 2019 was $22.5 billion.

As shown by Revolut, fintechs may weaken the relationship between customers and the banks. “For instance, in the future, it may be possible for a customer to manage their finances with only minimal direct engagement with their banks.” This will certainly make it harder for banks to maintain their high margins and profits.

Moreover, as digital banking wins over the traditional one, bankers as we know them are also at risk. According to the World Bank, the number of commercial bank’s branches per 100,000 people in developed countries like Belgium, France, Denmark, Germany, Italy or Spain have dropped an astonishing average of 5.9% since 2015 (to the last recorded year-worthy of data), which coincides with the foundation year of Revolut.

To cope with this already existing and growing competition, the big banks have to take one of two alternatives: to design on their own innovative alternatives and technologies that bring more value to customers as fintechs do; or to integrate these upcoming firms in their ecosystem, as it may be easier for these start-ups to be more agile and disruptive than for the “too big to fail” banking institutions. Otherwise, if these financial organizations also show themselves as “too big to innovate”, they are condemned to fail, to be replaced and outperformed by the upcoming fintech companies or even by big technological conglomerates like Apple, who are rapidly taking over some financial services (e.g. Apple Pay).

One thing is for sure: this competition will certainly benefit consumers and possibly even the whole economy, in which the new blockchain technology may have a relevant role to play.