The acute awareness of a new world being knitted together has helped prompt plans for the future that will capitalise on and accelerate the changing patterns of economic and political power. Chief among these is the Belt and Road Initiative (BRI), President Xi’s signature economic and foreign policy, which uses the ancient Silk Roads and their success as a matrix for Chinese long-term plans for the future.

Since the project was announced in 2013, nearly $8 trillion have been promised to infrastructure investments, mainly in the form of loans to around 1,000 projects in 65 countries.

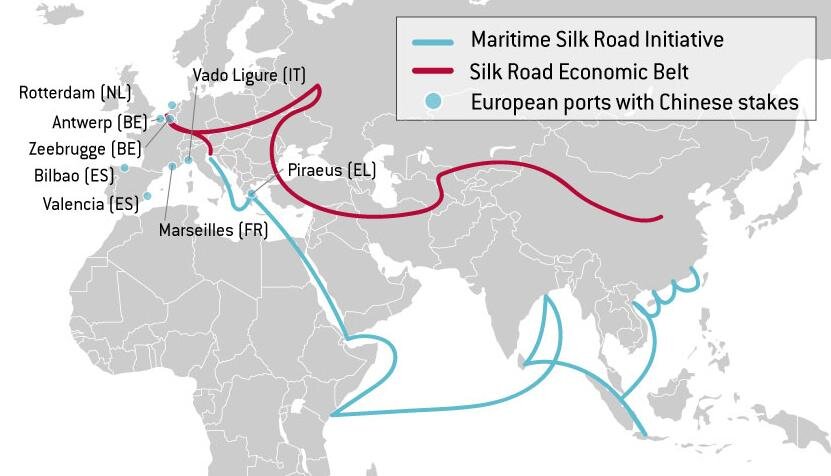

Some believe that the amount of money that will be ploughed into China’s neighbours and countries that are part of the BRI over sea – Maritime Silk Road – and land – Silk Road Economic Belt – will eventually multiply several times over to create an interlinked world of train lines, highways, deep water ports and airports that will enable trade links to grow even faster and stronger. In the meantime, the IMF issued a warning, in 2017, regarding the credit bubble, stating that the debt levels were not so much of a concern but rather a real danger.

China’s BRI was decided when the new leadership faced the combined pressure of the economic slowdown, US pivot to Asia and the deterioration of the relations with neighbouring countries after the 2008 Global Financial Crisis.

The continental economic belt focuses on the connectivity between China and Europe through Central Asia, and also between China, the Persian Gulf and the Mediterranean through Central and Western Asia. In addition, the maritime road aims to link China’s seaports to the South China Sea, the Indian Ocean and Europe.

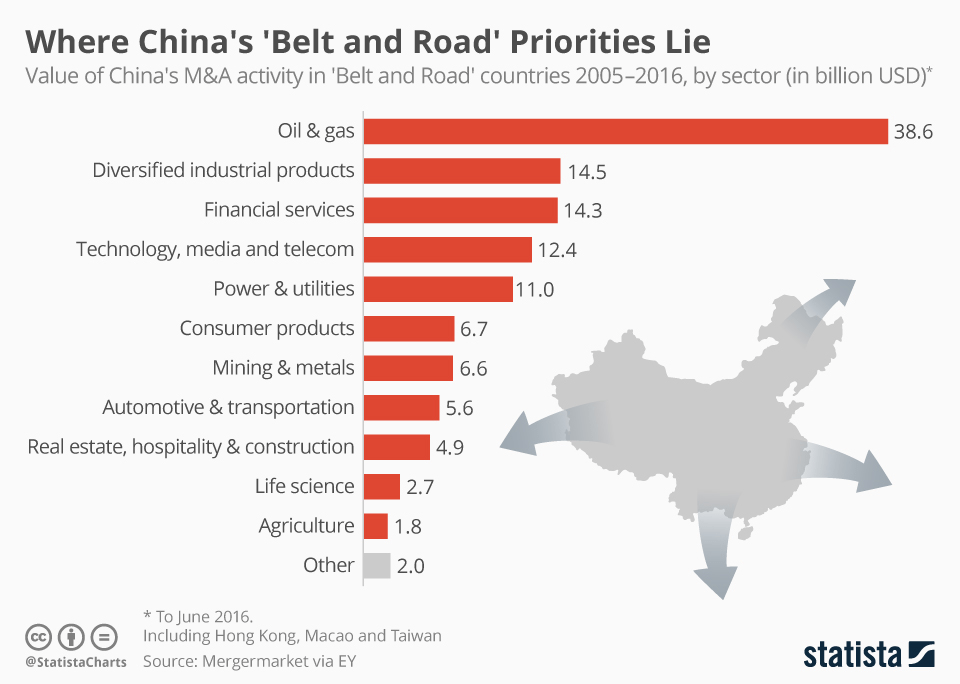

The BRI’s five major goals are claimed to be: promoting policy coordination, facilitating connectivity, unlimited trade, financial integration and people-to-people bonds. The sectors in which the BRI has focused more time and effort are oil and gas, diversified industrial products and financial services, as shown in the chart below.

Dealing with the ‘new normal’

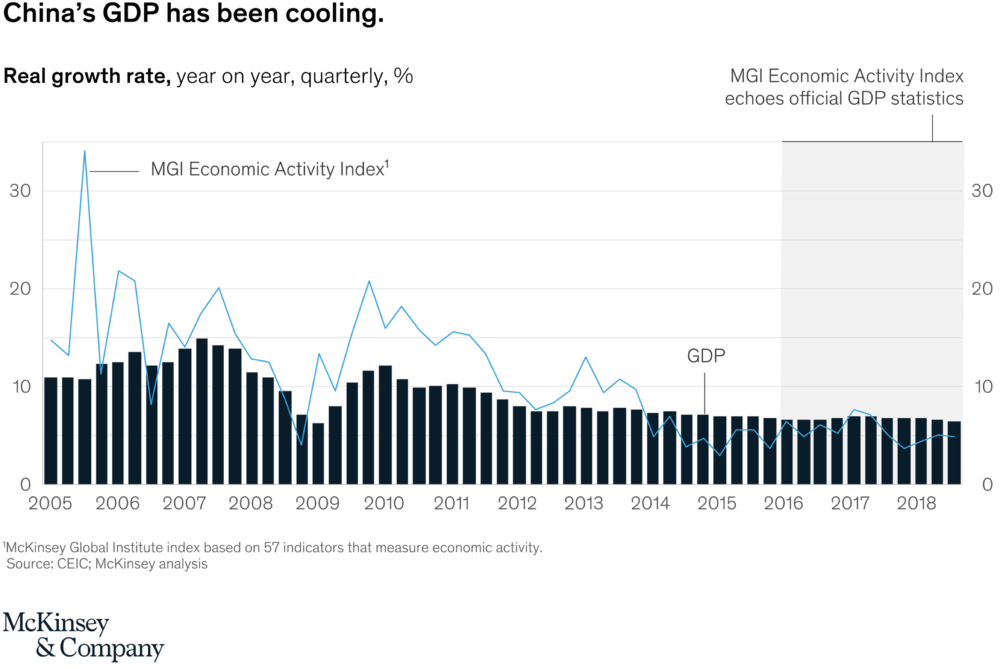

Serious challenges to the Chinese economy account for the most important drivers of the BRI. After the Global Financial Crisis and experiencing high-speed growth, the Chinese economy has slowed down since 2012 and entered the state of a ‘new normal’. China’s engine is cooling down, yet it continues to rack up one of the fastest rates of economic growth in the world. Given its enormous scale, this translates into substantial additions in absolute terms. In 2019, China added the equivalent of the entire Australian economy to its GDP. Nevertheless, the efficacy of China’s government stimulus has been waning.

Each renminbi of economic stimulus that the government pumped into the economy delivered less in actual GDP growth than in the past. The rise in ICOR (Incremental Capital-Output Ratio) – the amount of money the government needs to put in to yield a unit of growth – meant that economic stimulus was, in other words, getting more expensive.

Two major problems that the Chinese economy carries, which can be partially solved by the trade generated from the BRI, are overcapacity and excessive foreign exchange reserves.

The problem of overcapacity is not only in labour-intensive traditional industries, such as steel and cement sectors, but also in the so-called high value-added emerging industries, including new energy sectors. Overcapacity has kept the growth rate down, which makes it urgent to find alternative oversea markets.

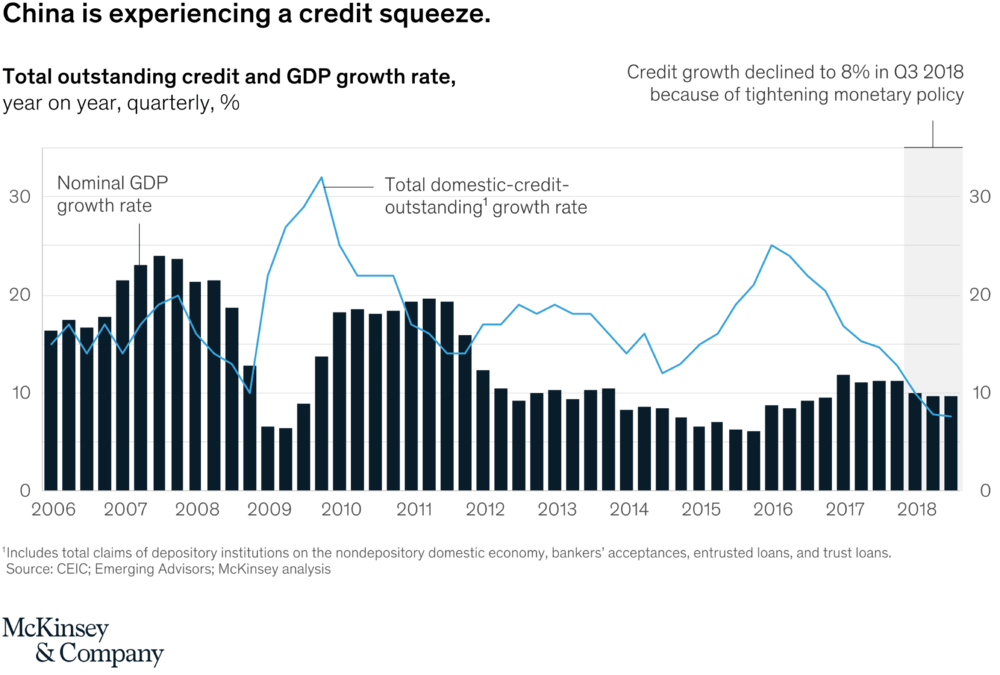

Excessive foreign exchange reserves were mostly caused by the large-scale stimulus package, as high as $586 billion, and further imbalance of the economy. The accumulation of excessive foreign reserves reflects worsening external imbalance, though it is also an upside factor to an emerging economy facing the risks of global adjustment. China’s foreign exchange reserve has rapidly increased to $4 trillion in recent years and about $1.4 trillion was invested in the purchase of US treasury bonds. Undoubtedly, this development is not sustainable and China’s economic leaders face severe political and economic pressure in tackling this issue.

In order to increase efficiency, China needs to find more exits for such large amounts of resources.

Studies made by Think Tanks such as the Asian Development Bank have shown that there is huge demand for infrastructure in Asian developing economies which is not largely met with existing multilateral and regional development financing institutions. It is believed that there is huge space for mutual cooperation between China and Asian economies on infrastructure investment, which is the reason why so many Asian developing countries have signed up for the two Chinese initiatives.

Debt vulnerability in BRI countries

As anticipated, BRI spans at least 65 countries with an announced investment as high as $8 trillion for a vast network of transportation, energy and telecommunications infrastructure connecting Europe, Africa and Asia. It is an infrastructure financing initiative for a large part of the global economy that will also serve key economic, foreign policy, and security objectives for the Chinese government.

Yet, important questions arise on sustainably financing the initiative within BRI countries and how the Chinese government will position itself on debt sustainability. Infrastructure financing, which often entails lending to sovereigns or the use of a sovereign guarantee, can create challenges for sovereign debt sustainability. When the creditor itself is a sovereign, or has official ties to a sovereign as China’s policy banks do, these challenges often affect the bilateral relationships between the two governments.

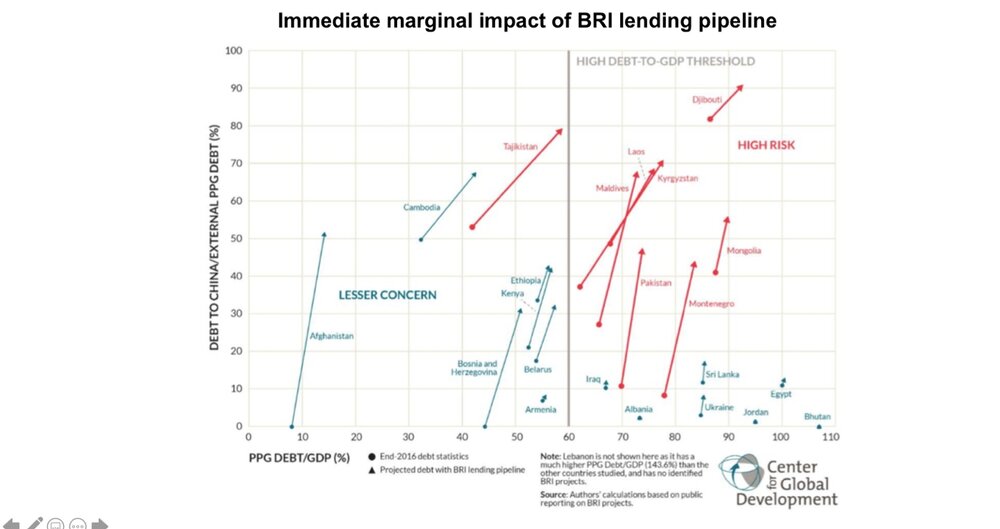

Even though China’s plan sounds like a brilliant idea to fix its own problems, it is not all sunshine and rainbows. There is a concern that debt problems will create an unfavourable degree of dependency on China as a creditor. Increasing debt, and China’s role in managing bilateral debt problems has already exacerbated internal and bilateral tensions in some BRI countries, such as Sri Lanka and Pakistan. Washington-based Center for Global Development raised serious concerns about 8 nations receiving BRI financing, namely Pakistan, Tajikistan, Maldives, Laos, Mongolia, Montenegro, Djibouti and Kyrgyzstan. These nations’ mounting debt to China puts their economies at risk of potential widespread default.

In Sri Lanka, citizens have regularly clashed with police over a new industrial zone surrounding Hambantota Port. Many argue that Chinese financing has led to a debt trap in Sri Lanka where the Hambantota Port project performed poorly once it was operationalised, operating at a loss. Consequently, on December 2017, the Sri Lanka Ports Authority renegotiated a deal with China Merchant Port Holdings (CM Ports), where CM Ports injected $1.1 billion for an 85% stake and a 99-year lease.

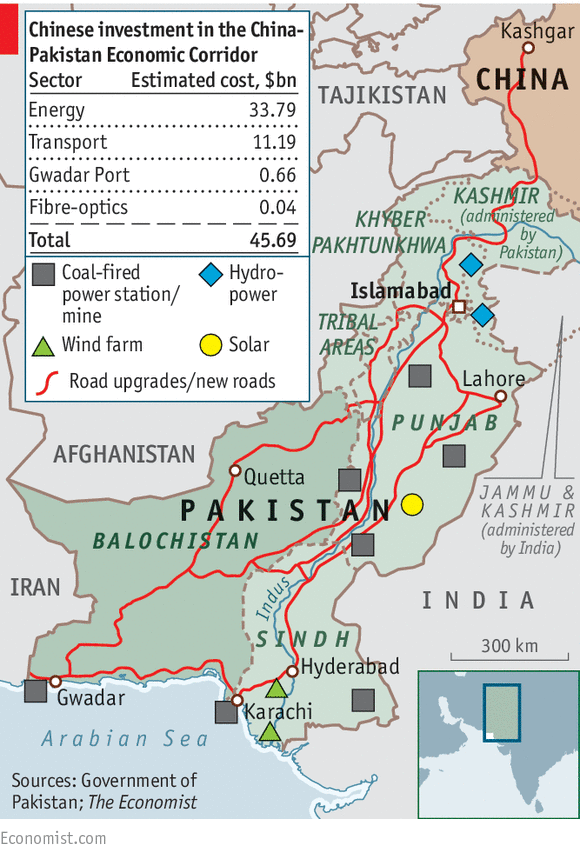

In Pakistan, Chinese officials openly appealed to opposition politicians to embrace the construction of the China-Pakistan Economic Corridor (CPEC), which is BRI’s ‘flagship project’ to bolster ties between Beijing and Islamabad.

The CPEC is the only corridor that links China to one single country – Pakistan, comprising an important trade route to China, particularly because of the country’s location between China and its energy suppliers in Africa and the Middle East, enforcing China’s huge energy appetite.

Pakistan may have taken more than what it was expecting when it took China’s loans. The country’s Prime Minister is fighting to keep the economy afloat and some are worried that Pakistan’s debt to China may ultimately hurt those efforts. The total value of CPEC projects is currently estimated at $62 billion.

The Belt and Road Initiative is President’s Xi’s most ambitious foreign and economic policy initiative. Much of the recent discussion has concerned the geopolitical aspects of the initiative. There is little doubt that the overarching objective of the project is to help China’s neighbouring countries become more closely tied to Beijing. However, there are many concrete and economic objectives behind BRI that should not be obscured by a focus on strategy.

Additionally, the lack of political trust between China and some BRI countries, as well as instability and security threats in others, are considered obstacles which have to be taken deeply into account when designing an action plan.

Finally, despite ad hoc approaches to the treatment of debt problems, there are some signs that Chinese officials are moving toward greater policy coherence and discipline when it comes to avoiding unsustainable debt.