The Vatican, the world’s most powerful religious organization, has been known to spread its political influence across the globe throughout the centuries. As of recently, its involvement in several financial activities has been at the source of many fracturing scandals.

Their home in the Holy See is the Institute for the Works of Religion (IOR), commonly known as Vatican Bank. By involving many different church officials and mobilizing hefty amounts of money, its analysis has become of increasing difficulty and controversy, causing many clashes with the Italian press to arise.

For the past years, the press has been adamant on bringing the Catholic Church into the confessionary. Despite their well-known soft spot for conspiracy theories, it is undeniable that the Italian press has become a key player in the disclosure of many of the Vatican’s scams. Their involvement in the Mafia’s money laundry schemes, the misuse of funds and donations and the embezzlement of the IOR’s money are among the most relevant situations of financial misconduct.

More specifically, in 2012, the Vatican spent $200 million to convert a former Harrods warehouse into luxury apartments.

This bizarre investment came out as a substitute for another peculiar project – the injection of those same funds in an Angolan offshore oil rig, then classified as unsafe. Given that 75% of the investment was sourced from a loan from the Vatican Bank itself, its Supervisory Board ended up noticing it and launched an internal investigation to clarify the situation. Despite dating back to 2012, this irregularity was only discovered in mid-October of this year. Since then, many have been wondering what led the Vatican to explore a project which deviated immensely from its institutional purpose, questioning the IOR’s legitimacy to undertake profit-making activities.

This was one of the most striking financial scandals hitting the Holy See since the 1970s and 1980s, when the Archbishop Paul Marcinkus, as President of the Vatican Bank, engaged in perverse relationships with mobsters. Another bank, Banco Ambrosiano, was also involved in the scandal. Its mission statement claimed the goal of serving moral organizations, pious works and religious bodies set up for charitable aims. It’s main shareholder? The Vatican Bank.

Roberto Calvi, known by many as the “God’s Banker”, was chairman of the Banco Ambrosiano and had close ties with the Church. The Vatican, instrumentalizing its position as a sovereign state, was able to withhold transaction information from regulators and authorities.

This was deeply exploited by Calvi in the 1980s, who was responsible for moving the bank’s (and consequently, the Vatican’s) funds into offshore accounts, enabling Banco Ambrosiano and, therefore, the IOR to make a profit.

Ambrosiano ended up collapsing in 1982, after the authorities found a hole of around $3 billion in the bank’s finances. Roberto Calvi died hanging in London. Prosecutors believe this to have been a Mafia killing, linked to his money laundering activities via the bank.

In 2012, Father Ninni Treppiedi, priest in Alcamo, near Trapani, in the Mafia’s island stronghold of Sicily, was suspended after a series of questionable transactions of church funds and of vast sums of money passing through his personal bank accounts. Prosecutors highly suspected that this was the result of money laundering operations run by the Mafia Godfather, Matteo Messina Denaro. They investigated financial transactions that occurred between 2007 and 2009, amounting to around $1 million. Nevertheless, paperwork regarding the source of the money was said to be missing and the Vatican Bank did not want to release the records of the Father’s accounts. Ultimately, Treppiedi’s case was filed by the order of the Court of Trapani, but most people kept the suspicion about the connections with the Mafia.

The liaison between the Church and the mobsters remains until today, albeit the Vatican’s efforts to trail a path of cleaning and rebranding, focusing on increasing transparency.

Indeed, in the last decade, the Holy See has been trying to put an end to corruption in the management of the bank’s funds, through concrete reforms.

“These are scandals and they do harm.”

Thus, they need to be handled with. Accordingly, the first step towards more transparency was given with the establishment of the Financial Intelligence Authority (AIF) and with the implementation of the first anti-money laundering rules, in compliance with the European Union’s standards. These actions took place in 2009, during the Papacy of Pope Benedict XVI.

Despite some progress being made in the end of the last decade, the greatest improvements have been achieved under the control of Pope Francis, who took charge in 2013. In that same year, following a scandal of money laundering, in the value of $20 million, by Nunzio Scarano, referred to as “Monsignor Cinquecento”, the responsible for overviewing Vatican’s property holdings and investments, a Pontification Commission was established in order to review the activities of the bank. As a result, later in that year, more than 1000 customer accounts were closed.

Afterwards, in 2014, Pope Francis delivered a blunt message – the IOR would only be allowed to continue its operations as long as it committed to self-reform. In this regard, as the Holy See’s ministries, the discateries, were not controlled by the AIF (despite managing plenty of money) the Pope created the Secretariat for the Economy to keep an eye on their activity. Further policies included the transition from an internal auditing system to an external one and the requirement that the employees at the Vatican Bank worked exclusively for that institution, avoiding potentially harmful situations, such as the one involving Marcinkus in the 1970s and 1980s.

In terms of international assessment, Moneyval, a monitoring body of the Council of Europe that aims at countering money laundering practices, has praised the Vatican for its course of action in recent years in this regard.

All in all, the Holy See seems committed to carve out a new image for the Catholic Church, closer to its founding principles. Nonetheless, the Italian press argues that the increasing disclosure of scandals is instead a proof of the inefficiency of the adopted measures. Only time will tell which side the truth is on.

Sources:

-

Crux Now

-

European CEO

-

la Reppublica

-

Organized Crime and Corruption Report Project

-

Religion News Service

-

Reuters

-

The Economist

-

The Telegraph

-

U.S. Catholic

-

Wikipedia

Article Written By:

Ana Mota

Ana Mota  Gonçalo Silva

Gonçalo Silva

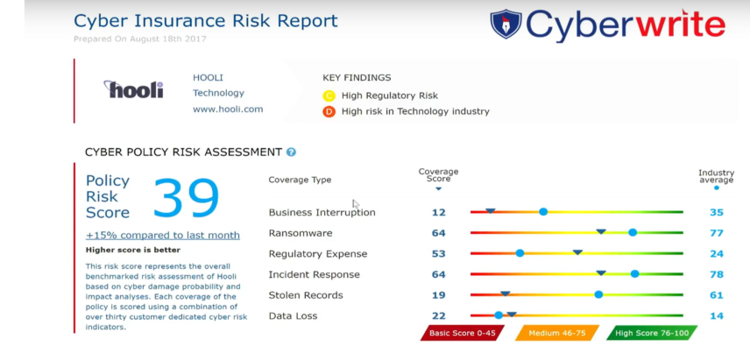

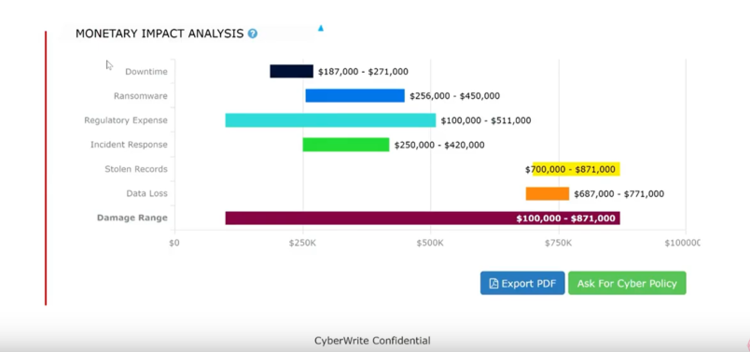

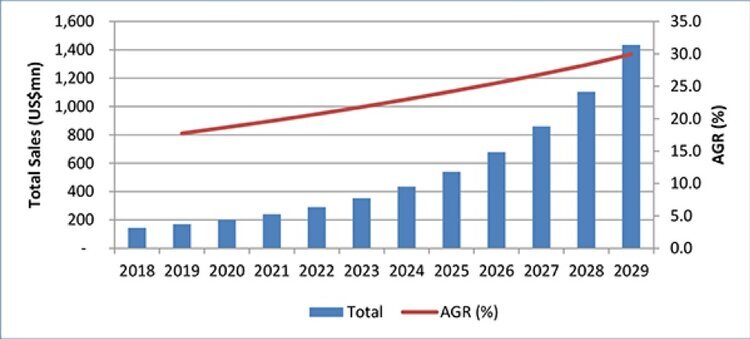

Forecast for sales of cyber insurance in South America. Taken from the cyber insurance market report 2019-2029

Forecast for sales of cyber insurance in South America. Taken from the cyber insurance market report 2019-2029