“China will strengthen green and low-carbon policies and regulations with a view to strictly control public investment flowing into projects with high pollution and carbon emissions both domestically and internationally”. These were the words of President Xi Jinping in 2014. Later on, in July 2019, China committed to “update” its climate target “in a manner representing a progression beyond the current one”. Furthermore, it also vowed to publish a long term decarbonization strategy by next year.

But can this nation live up to the promises?

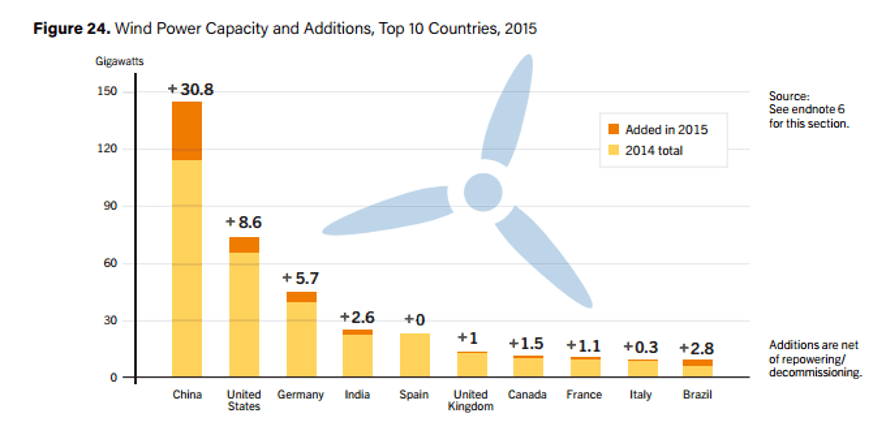

Indeed, China made an effort in promoting green development: in 2015, it increased its wind power capacity by over 30 gigawatts, becoming the number one leader in this parameter.

In that same year, China saw a huge growth in solar power production, moving into first place, surpassing the previous solar leader, Germany.

Image from REN21 Renewables 2016 Global Status report

Image from REN21 Renewables 2016 Global Status report

China has been the world’s leading country in electricity production for renewable energy sources, according to Global Commission on the Geopolitics of Energy Transformation, establishing itself as a global pacemaker in driving a domestic decarbonization agenda.

On the one hand, tension arises upon the fact that the country finances clean energy, representing 11% of its budget spent on electric power generation. On the other hand, investment in coal production amounts to a total of 36% of the Belt and Road Initiative. [1]

Conflicts of interest have emerged between the promise to reduce coal production and the fact that it has been one of the biggest contributors to the growth in the power sector. In fact, China is responsible for 51% of coal’s global demand as well as 46% of its global production – if the country continues to go down this path, its reliance on coal will not fall not even close to the promised value.

-

Demand-side: China’s coal consumption has been growing at a slower rate and not necessarily declining. It could indeed be said that Chinese coal demand has been relatively flat for a few years now, but it has not been falling in the absolute sense.

-

Supply-side: Coal power generation has been rising at 6% per year and China has reached 1.76 billion tonnes of this fossil fuel in the first half of 2019 – which represents a 2.6% increase from the same period last year.

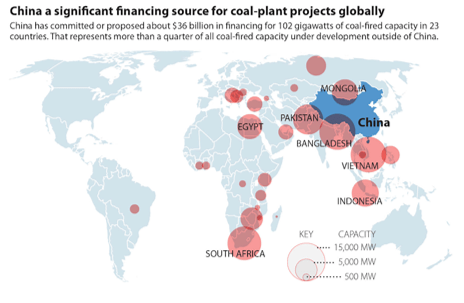

On top of that, China’s financial institutions are providing $36 billion in funding to build coal power plants outside the country.

A unit-by-unit analysis of all global coal plants under development, based in 2018, shows that Chinese investment has had a significant increasing role in supporting and funding new coal plants in international markets as shown in the image below:

Source: Global Coal Plant Tracker (July 2018) IEEF analysis

Moreover, Chinese financial institutions and corporations have agreed to fund over one-quarter of the 399 gigawatts (GW) of coal plants currently under development outside China. This comes at a time where many financial institutions such as the World Bank are shifting away from the coal industry.

According to research organization Climate Action Tracker (CAT) China’s actions and policies are highly insufficient to meet the challenge of holding global warming below even 2ºC, let alone the Paris Agreement limit of 1.5ºC.

As the world’s leading greenhouse gas emitter, CAT also predicts that China’s emissions will rise at least until 2030, at a point which is likely to be too late to curb the country’s impact on climate change.

Nonetheless, another question arises: will China be able to successfully decrease its coal production so fast as it pledges?

With Beijing’s push to reduce coal burning, nearly 13 million households in northern China have switched to electric or gas-heating since 2016.

In 2017, when northern China experienced the biggest ever campaign to replace coal with natural gas it was reported that, in Beijing alone, 140,000 households, across 336 villages bid farewell to coal.

In addition, the toughest restrictions ever on industry were also put in place, from mid-November to mid-March: 15 key cities had to cut steel manufacturing output by 50% which was a big improvement regarding environmental changes, since over 71% of the steel produced uses coal. Also, aluminium production was cut by 30 % as the energy for its digestion plant is derived from steam raised by using coal.

Despite the major decline in atmospheric pollution in those areas and the decrease in the national coal capacity, the rushed measures caused serious problems, since China’s infrastructures were not prepared for this significant change.

Since there was not enough time to install the gas pipes underground in Shijing, they were left above ground causing safety risks for civilians.

Furthermore, widespread reports from the winter of 2016 disclosed heating problems caused by failures to complete the switch to gas on schedule. As a result, some schools in rural zones had no heating, given that coal-fired boilers had been removed before natural gas pipes were installed. Similarly, in Linfen, a village located in Shanxi, had a 155 square kilometer “no coal zone” where residents had to remove coal stoves and they were not even allowed to keep coal at home – yet no alternative heating was provided, despite sub-zero temperatures.

Also, market-wise, as many firms and industries were highly dependent on coal, these restrictions placed them on the verge of shutting down. Eventually, gas heating increased, resulting in supply shortages and causing inadequate heating for many households.

All in all, the world’s success in bringing down global warming is dependent on China’s action, the world’s largest carbon emitter.

Yet, it appears that China’s interests are ebbing as its economy slows. Combined with an ongoing trade war with the United States as well as Trump Administration’s withdrawal from the Paris Agreement, this economic slowdown has reduced China’s enthusiasm to lead in this global battle. The aforementioned is no excuse for China to forgo a leading role in the fight against global warming. Indeed, embodying the “torchbearer” may be the country’s best bet for a sustainable transition to a stronger and low-carbon economy.

[1] The Belt and Road Initiative (BRI) development strategy aims to build connectivity and co-operation across six main economic corridors encompassing China and: Mongolia and Russia; Eurasian countries; Central and West Asia; Pakistan; other countries of the Indian sub-continent; and Indochina, quoted from OECD Business and Finance Outlook 2018

Sources: The World Economic Forum, The New York Times, Climate Change News, The Diplomat, Forbes, Institute for Energy Economics & Financial Analysis, Reuters, Chinadialogue, OECD