The past weeks have been tense for the financial markets, with the stock market reacting negatively to the inversion of the Yield curve, one of the most preeminent indicators of recession in the past, which adds up to the failures registered in the last two years in making the economy dynamic again (via extremely low interest rates).

The truth is that the alarms are starting to ring in several fronts. Tensions between the US and China increased concerns among investors, and may deteriorate the whole economy, taking another step towards the recession. Investors have started to leave the common equities to take refuge in sovereign debt and gold, with the latter one being traded at around 1500 dollars (28.3% increase in the last 52 weeks according to Bloomberg), the highest since 2013.

Germany

Financial data about Germany, the strongest economy in the eurozone, also shows that an economic breakdown could be just around the corner with the country’s interests in sovereign debt negative in all the available periods (including the 30 years bonds) helping keeping the country slightly above the recession line.

The PMI (Purchasing Managers’ Index), a widely used economic activity indicator, stated a decrease in the country’s performance (43.5 in a scale from 0-100 where values below 50 indicate an expected retraction) and the industrial production registered the biggest fall of the last ten years (being affected by the US-China trade war in the exports field).

If we add up all this data to the fact that in the last year the country barely avoided a technical recession (GDP contraction for two consecutive quarters), it might be possible that the recession in the eurozone’s biggest economy is close to happening and with that its main traders will suffer repercussions.

To support this opinion, the reading of this year’s data about Germany’s economic performance is recommended, since this last quarter (April-June) the economy sank 0.1%. Next quarter prospects are not that good as well, but will depend on the markets’ reactions to the new quantitative easing programme (which will be launched in November).

Monetary Policy

Negative interest rates? Once seen as an anomaly, negative interest rates are becoming increasingly more common since the last financial crisis. Among the countries/monetary unions with «subzero» interest rates we have Denmark, Japan, Sweden (the first to adopt the strategy), Switzerland and the Eurozone.

Mainly used as an extension of the traditional monetary policy tools to avoid deflation, encourage lending and promote economic growth, these policies have lost their catalyst power, with the economy being “trapped” into an inefficient mechanism that contributes more to feed the Assets and Real Estate “bubble” than to give a temporary stimulus for a sustainable growth in the future. (Housing prices in the US are 8% higher than at the peak of the real estate bubble in 2006, and the CAPE ratio, Cyclically Adjusted Price to Earnings Ratio, that is generally applied to broad equity indices to assess whether the market is undervalued or overvalued, is also higher than in 1929 and 2008).

In fact, the bond market with negative yields already reached 17 trillions, roughly 30% of its entirety, which reveals the uncertainty amid the remaining market (not to be confused with the bond market, which is historically safe), with people willing to lose some money in order to avoid major losses.

It is also worth mentioning that these measures do not give signs of stopping, since Mario Draghi decided to restart ECB’s economic stimulus efforts with a quantitative easing programme of €2.6 tn, an act heavily contested by some of his peers in the Central Bank such as Klaas Knot, Dutch Central Bank governor, who said “this broad package of measures, in particular restarting the asset purchase programme, is disproportionate to the present economic conditions” and also “there are increasing signs of scarcity of low risk assets, distorted pricing in financial markets and excessive risk-seeking behaviour in the housing market”.

The Central Banks of Thailand, New Zealand and India have also started to cut heavily on the interest rates, more than investors were expecting, putting the monetary policy concerns into a globalised proportion.

Trade War

In the geopolitical arena, we have another big threat to the current weak balance of the worldwide economy: the worsening of the commercial tensions between the US and China, which has been speculated to degenerate into a currency war. This derives from China’s reaction to the implemented tariffs in every Chinese product applied by the US, that resulted in the devaluation of the Renminbi, with all the consequences that this measure means for the trade balance. Also regarding this topic, it is important to mention that China’s economy grew at its slowest pace in almost three decades in the second quarter of this year, as the trade war with the US took its toll on exports. Despite remaining with relatively good income and consumer spending growth rates, the year on year growth rate was “only” 6.2%, the lowest since 1992.

Maybe it is only one more episode in an endless novel, with both sides continuously failing to find a solution to their divergences, but as the time passes and the patience burns out, this might escalate into even more serious issues, with Bloomberg predicting a 0.6% decrease in global growth if the two countries expand their tariffs to all goods and services.

Yield Curve Inversion

Even more distressing is the inversion of the Yield curve of US Treasuries, that basically retracts the evolution of the 3 months interest rate versus the 10 years’ one (we can compare several periods within this range), meaning that the cost of borrowing long term is falling below that of borrowing short term, which is the opposite of what it should be. This phenomenon reflects investors’ collective uncertainty towards the current economic outlook and is thought to be the biggest warning to the markets since the 2007 recession, with investors turning to safer assets, such as the 10-year treasury bonds.

This is supported by the fact that the last 5 recessions were all preceded by one of these inversions (approximately between 12 to 18 months after). Despite this historical data, it is also important to bear in mind the economic environment we face today, since the extremely low interest rates in the eurozone and Japan and the mistrust of the investors are increasing the demand for US treasury bonds.

Naturally, and following Alfred Marshall’s law (Demand and Supply), the prices of the bonds are increasing and consequently the yields are decreasing in the same proportion, contributing for the inversion of this curve.

Counterarguments

Nonetheless, it is important to mention that there are also positive signs within the economy that might, at least for a while, dispel the recession. These signs include the fact that the low bond yields are widely explained by the aggressive monetary policy stimulus, that might distort a little bit the effectiveness of its predictions. Also, in the yield curve “field”, its small amplitude when compared with the likes of mid 70’s and early 80’s in terms of percentage, until a certain extent reduces the urgency of the warning.

The fact that the S&P 500 is just a few points below July all-time high,which signals goods expectations among the investors in what concerns corporate earnings.

Lastly, and perhaps one of the most important indicators, the fact that wages are growing strongly and the spectrum of deflation, characterized by a general decrease in the prices of goods and services with its implications in terms of wages, is for now a distant reality. This is of huge importance for the US, given that their economy is based 70% on consumption. (Wages grew 4.7 percent annualized in the second quarter of the year, US poverty rate has fallen to its lowest level since before the last financial crisis and Bloomberg Consumer Comfort index that assesses buying climate and personal finances reached an 18 year high, motivated by the good atmosphere that surrounds both the job and equity markets, with its value being fixed in 67.4 by 14th July.)

Conclusion

The past and the economic background that comes with it tell us that the inversion of the yield curve should be considered a serious foreshadowing of a recession, although the current economic atmosphere might have until some extent distorted the trustworthiness of this predictions. It is also important to state that a recession is not necessarily dreadful or horrific, it is indeed natural and takes part in all economic cycles.

However, alongside with continuous decreases in interest rates, trade wars, China’s growth deceleration, wealth and income inequality and others, a recession can be indeed “horrific” and “dreadful”, since it might trigger a more serious economic and political crisis, posing important challenges to government policies, that each day are getting more exposed with the decreasing power of one of its major mechanisms, the monetary policy.

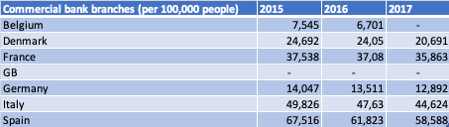

Number of commercial bank branches in Europe (per 100,000 people)

Number of commercial bank branches in Europe (per 100,000 people)