Greater ease of access to information and technology created a new paradigm in the market that was further accentuated by the COVID-19 pandemic. The result has been a new balance of forces in the market, as seen in recent events. Whether this new paradigm will last, only time will tell… or the SEC.

Financial markets have long been associated with high-net-worth individuals and institutional investors. In fact, as of 2017, according to the National Bureau of Economic Research, the top 10% in the United States were in control of 84% of the total value of stocks, bonds, trusts and business equity. Much of this wealth is managed by institutional investors, such as hedge funds, commercial banks, or mutual funds – the so-called “smart money”. The dominance over the market by institutional investors meant that retail investors – individual investors often referred to as “dumb money”, due to the belief that these lacked the expertise, as well as the understanding of market forces – were undermined by hedge funds managers and investment banks for a long-time.

However, greater ease of access to information and technology created a new paradigm in the market that was further accentuated by the Covid pandemic. The result has been a new balance of forces in the market as seen in recent events. Whether this new paradigm will last, only time will tell…or the SEC.

The rise of retail investors

The coronavirus outbreak in the mid-quarter of 2020 triggered the growth of retail investors, which translated into a revolution in the stock market. With millions of people worldwide confined in their homes, their attention to the stock market increased, with more than 1 million new online brokerage accounts opened in the first three months of 2020. The new market participants were mainly young investors with little or no expertise who disregarded risks while pursuing new opportunities.

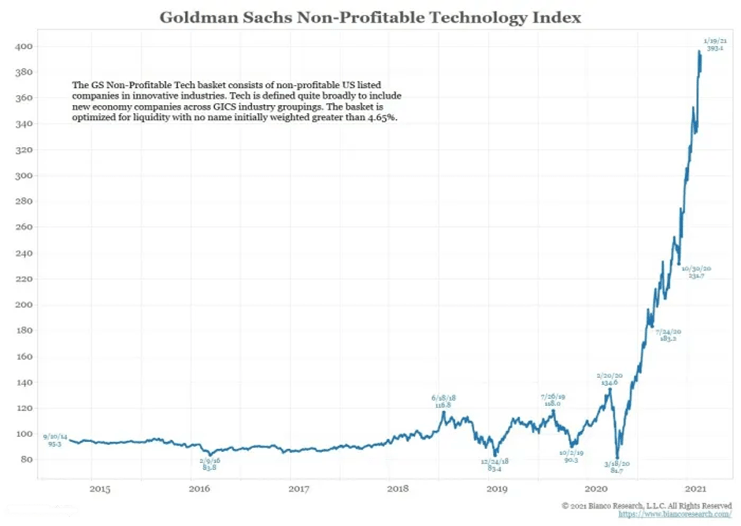

According to Deutsche Bank, “increased retail trading is ‘largely responsible’ for elevated stock prices and record-high options activity”, showing how these individual investors are driving the stock market. In addition, this increase in the number of call-options was mainly evident in small companies with low profitability. Retail investors are trading speculative stocks with low share prices, due to zero-commission investing apps and online brokerages. The New York Stock Exchange report demonstrated that, during several months in the Spring and Summer of 2020, more than 25% of the shares traded in the U.S. stock market were in companies with a share price below $5. To reinforce this tendency, Goldman Sachs, an investment bank, provided an index of non-profitable technology stocks, usually one of the main drivers of stock market valuations, which has raised nearly 400% since mid-March of 2020.

What lies behind that surge?

A global pandemic marked the year of 2020, as well as the stock market. While markets flopped and recovered in the first half of the year, retail investors sought an opportunity to try to take advantage of the circumstances to invest. The coronavirus pandemic led to an increase in retail investing. With the majority of people working remotely and having more free time to spare, many experimented the investment world. Nowadays, retail investors dispose not only of more financial information, but also of better investment education and trading tools. Furthermore, the $1200 COVID-19-relief check the US Government issued in April 2020 helped fund the trend, as shared by many redditors, users of the online social media platform Reddit where investors gathered in the R/WallStreetBets forum to discuss investments.

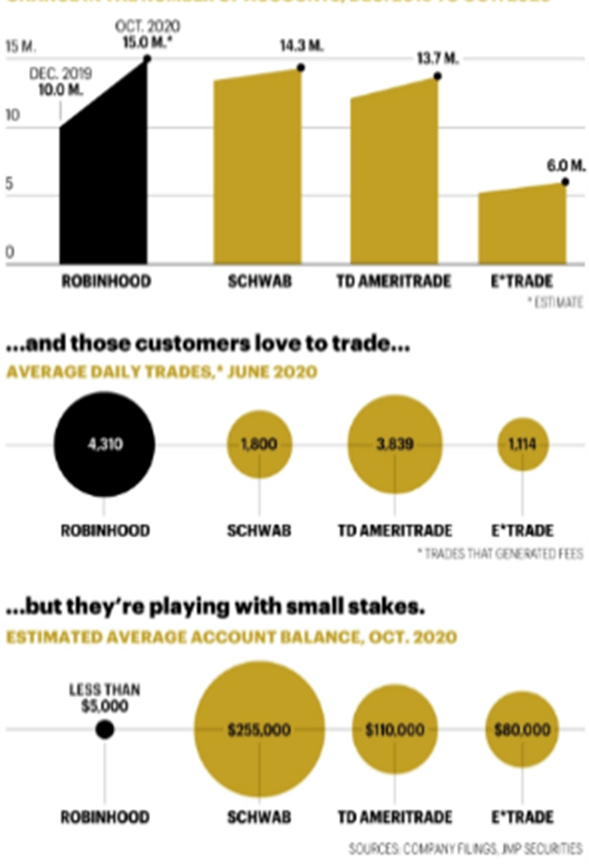

Another boosting factor that allowed the rapid growth of retail investment were online brokerages, enabled by the payment per order flow, which is the form of compensation for the firms charging zero-commissions to traders. These online intermediaries enabled investors to swiftly and easily sign up and try investing, this being far more accessible when compared to traditional intermediaries. At the end of 2019, most major online brokerages eliminated commissions for online stock trades. One example in which it is clear that this cut provoked a rise in retail investing is Robinhood. This investing app offers commission-free stocks, no minimum balance and permits the acquisition of fractional shares. From the beginning of 2020, Robinhood had reported 3 million new accounts, being half of them the first accounts of the investors.

The combination of these factors supports the idea of financial democratization that was accelerated in 2020 when millions of consumers where confined.

What does it mean for the stock market?

The impact of this increased predominance of retail investors is significant for all parties.

The first outcome would be the democratization of the markets in the sense that new trading platforms eliminate some barriers that restrict access to the market, namely commissions or capital requirements. As a result, financial gains from the stock market are more equally spread over the population. On the flip side, loss of capital is more harmful for retail investors, especially considering the frequency of bet-like investing behaviour among zero-commission trading apps through high leveraging and options that some do not fully understand.

This has been a major critic from hedge funds, which argue that the lack of expertise may affect basic market assumptions, such as the efficient allocation of resources, besides overinflating prices. For instance, despite the fact that retail investors provide liquidity when institutional investors pull back, that increased activity from herd behaviour creates volatility, which may ultimately affect the liquidity of that “hot” stock, as well as lead to panic selling. Therefore, retail investors end up underestimating their own market power.

For that reason, there have been calls for the SEC to implement more regulation on trading apps, and, consequently, on retail investors. The way these apps work is also under scrutiny, owing to the gambling experience they provide, by rewarding and incentivizing purchases rather than serving as simple intermediaries, which blurs the line between investment and entertainment.

One way of reducing the negative aspects of a broader market access is through financial literacy. If the process is accompanied by proper education on financial markets, new investors will be equipped with the tools they need to make rational investments, instead of gambling on stocks. This would not only benefit them, but also institutional investors, by solving the most prevalent argument invoked by the latter.

How does GameStop fit into all this? GameStop was one of the “meme stocks” the new wave of investors, armed with new trading technologies and funded by savings and stimulus checks, laid their eyes on. The army of traders working together in a short squeeze exerted enough strength to force a bailout on a number of hedge funds betting against the company. Without going into detail on the structural problems of payment per order flow or the technical terms behind the short squeeze, the case of GameStop shows individual investors are a force to reckon with.

There is, however, one important aspect to consider. Retail investors have flooded the market before whenever barriers to the market decreased. The phenomenon first occurred in the 70s, through discount brokers, and then in the 90s, as a result of online trading. The newest trading platforms have eliminated almost all barriers. Consequently, trading volumes are now twice as much as in 2010, whether this trend will continue is contingent on action from regulators. The scandal over the brokerage app Robinhood will likely lead to action either from Congress or the SEC, which, in turn, may affect how these apps function and access to market.

Sources: ABC News, Business Insider, Financial Times, Market Watch, Medium, Nasdaq, National Bureau of Economic Research, Statista, University of Chicago, Wall Street Journal

Tiago Rebelo

Raquel Novo

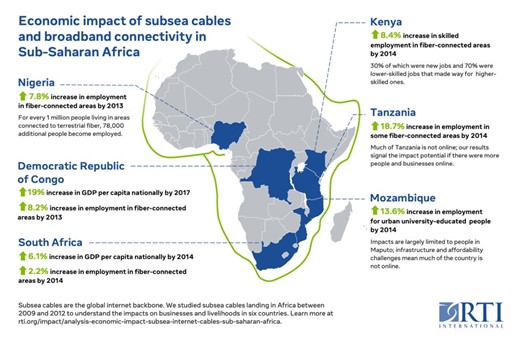

The number of connections between Africa and the world.

The number of connections between Africa and the world.