Once mistaken for the janitor by an employee’s parent, Alibaba Group’s CEO Daniel Zhang will be replacing Jack Ma as chairman of the company. What are the prospects?

In 1999, the biggest e-commerce and retail company in the world was created in an apartment in Hangzhou by a team of 18 individuals. One of the co-founders, Jack Ma (7.8% stake), then became the enterprise’s CEO and chairman and, consecutively, China’s wealthiest man, with a net worth of around US$42 billion. On September 2018, Mr. Ma publicly announced that he would be stepping down as Alibaba’s chairman and, one year after, on the 10th of the same month, the role of executive chair was passed on to Daniel Zhang. But what legacy did Jack Ma leave behind?

The Alibaba Group provides business-to-business – B2B – (Alibaba.com), business-to-consumer – B2C (Tmall) and consumer-to-consumer – C2C – (Taobao) sales services. It is considered the largest e-commerce company, with a gross merchandise value in 2018 of US$854 billion, outperforming Amazon3 and eBay4 combined. Furthermore, the company had the highest initial public offering (IPO) in history, with an astonishing value of US$228 billion when Alibaba raised more shares shortly after getting listed in the stock market5. As of 10th September 2019, when Jack Ma resigned from his position, the Alibaba Group had a market cap of US$455.6 billion.

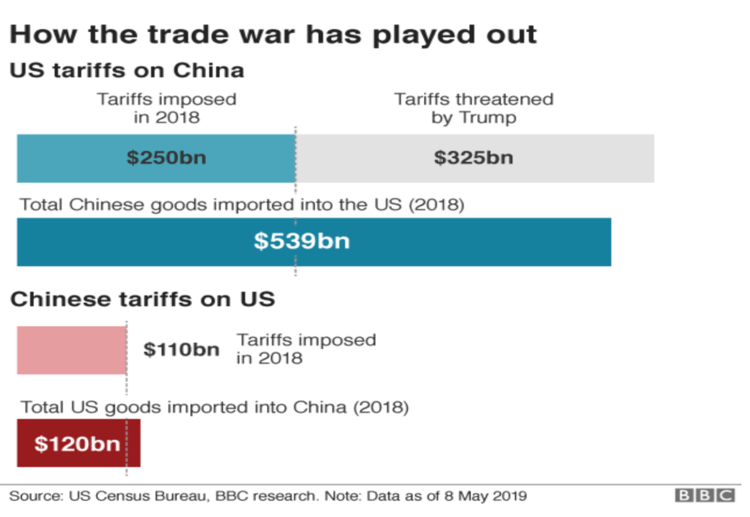

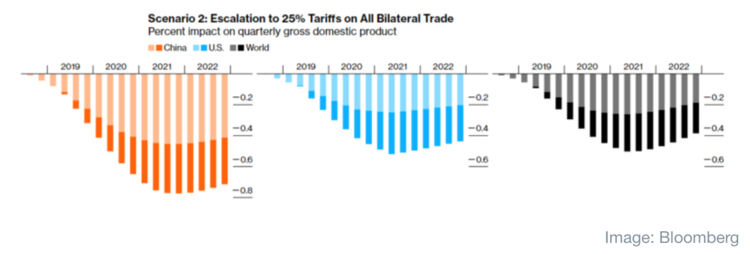

It looks as if Daniel Zhang has some really big shoes to fill, and the Chinese situation is very precarious at the moment, with its economic growth slowing down (6.2% yearly growth rate, the lowest since 1992), the trade war with the US and due to the protests in Hong Kong, that have already resulted in delay of a stock offering that could have raised US$20 billion for the company.

However, Mr. Zhang has proven so far to be extremely competent for this task. He joined the Alibaba Group in 2007 as CFO of Taobao (comparable to eBay) that, despite being the most visited website at the time, was suffering from severe losses and fraudulent sellers. In the following year, he was put in charge of the development of Tmall (comparable to Amazon) and, in order to attract brand names to this subsidiary of Alibaba, not only did he provide top merchants with relevant information regarding their buyers – who was buying what, area of residence, which ads were more effective – but he also installed a more complex security system concerning copycats and, as a result, sales rocketed. Daniel Zhang was also responsible for the creation of Singles’ Day, which is an annual deals-fest whose sales amounted to US$31 billion last year alone, outdoing the values of Black Friday in the USA.

And it does not stop here: as a chairman, Daniel Zhang has revealed initiatives to place Alibaba in fields such as finance, healthcare, films and music. He has stated in an interview with Bloomberg:

“Every business has a life cycle. You have to be innovative and create new businesses with new technology, with a new model. Then that can make our entire business sustainable. We always say that we want to build a sustainable, long-term business. But most of it is not evergreen. I strongly believe that if we don’t kill our existing business, someone else will. So I’d rather see our new business kill our existing business.”

Of many projects that Zhang has been developing, however, there is one remarkably ambitious and innovative, Freshippo. This is a start-up of the Alibaba Group that would unite the concept of a grocery store, a restaurant and a delivery app all together, along with the aid of robotics and facial recognition. With 150 stores across 17 cities, Daniel Zhang states that Alibaba is determined to take 50% of the food delivery sector. Moreover, on the 25th of this month, the enterprise unveiled its first chip developed for artificial intelligence, becoming the most recent non-traditional chipmaker company to develop its own AI hardware.

The future, however, is uncertain, as many start-ups strive to compete for leadership of the food delivery market, and expansion has been challenging. Alibaba has already sunk US$4 billion in attempts at expanding to Southeast Asia and Donald Trump’s administration is considering the banning of Chinese companies listing in the US as a move in the trade war, which will greatly impact Alibaba’s shares, that have gone down by 4% since the news were released.

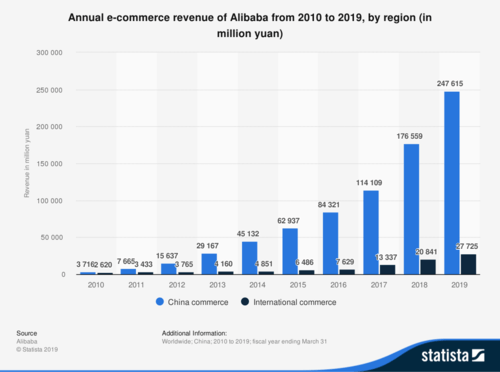

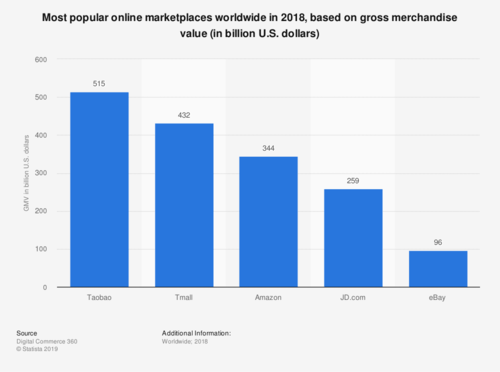

In order to analyse the outlook for Alibaba, it is important to consider its current presence in global markets while comparing it to China, its main source of revenue. One of Jack Ma’s long-term goals was to have half of the revenue coming from outside of China, but it is clear that the company is far from independent of the Chinese market provided that, in this year, its e-commerce revenues from international commerce only amounted to a mere 10% of Alibaba’s total revenues. However, both its subsidiaries Taobao and Tmall are clear leaders in the overall global markets when comparing gross merchandise value.

Annual e-commerce revenue of Alibaba

Annual e-commerce revenue of Alibaba Most popular marketplaces worldwide in 2018

Most popular marketplaces worldwide in 2018All things considered, although the leadership of Daniel Zhang has been looking promising for the company, there are many key factors that are weighing Alibaba Group down, so large global expansion opportunities might be jeopardized by several adversities. The question that lingers is: Will Daniel Zhang leave triumphant or was he at the right place at the wrong time?

Mariana Inglês

Mariana Inglês

Afonso Botelho

Afonso Botelho  Ana Mota

Ana Mota  Gonçalo Silva

Gonçalo Silva  Nuno Sampayo

Nuno Sampayo